AZZ Inc. Boosts Financial Strength Through Strategic JV Gains and Operational Expansion

AZZ’s robust annual results driven by equity gains from the AVAIL joint venture and steady demand in metal coatings underline a solid base for growth amid cyclical headwinds.

AZZ Inc.’s fiscal 2026 performance was markedly strengthened by significant equity earnings from its 40% stake in the AVAIL Infrastructure Solutions joint venture, which realized gains from divestitures of electrical and welding services businesses. The company’s core Metal Coatings and Precoat Metals segments maintained stable demand aligned with typical seasonality in construction and industrial markets. Operational cash flow surged, supporting capital returns through dividends and share repurchases while liquidity remained strong. Despite volatility risks in input costs and cyclical seasonality tied to North American infrastructure spending, AZZ’s leading market positions and JV partnerships provide differentiated growth levers to monitor.

Recent Operational Highlights from Latest 8-K Filing

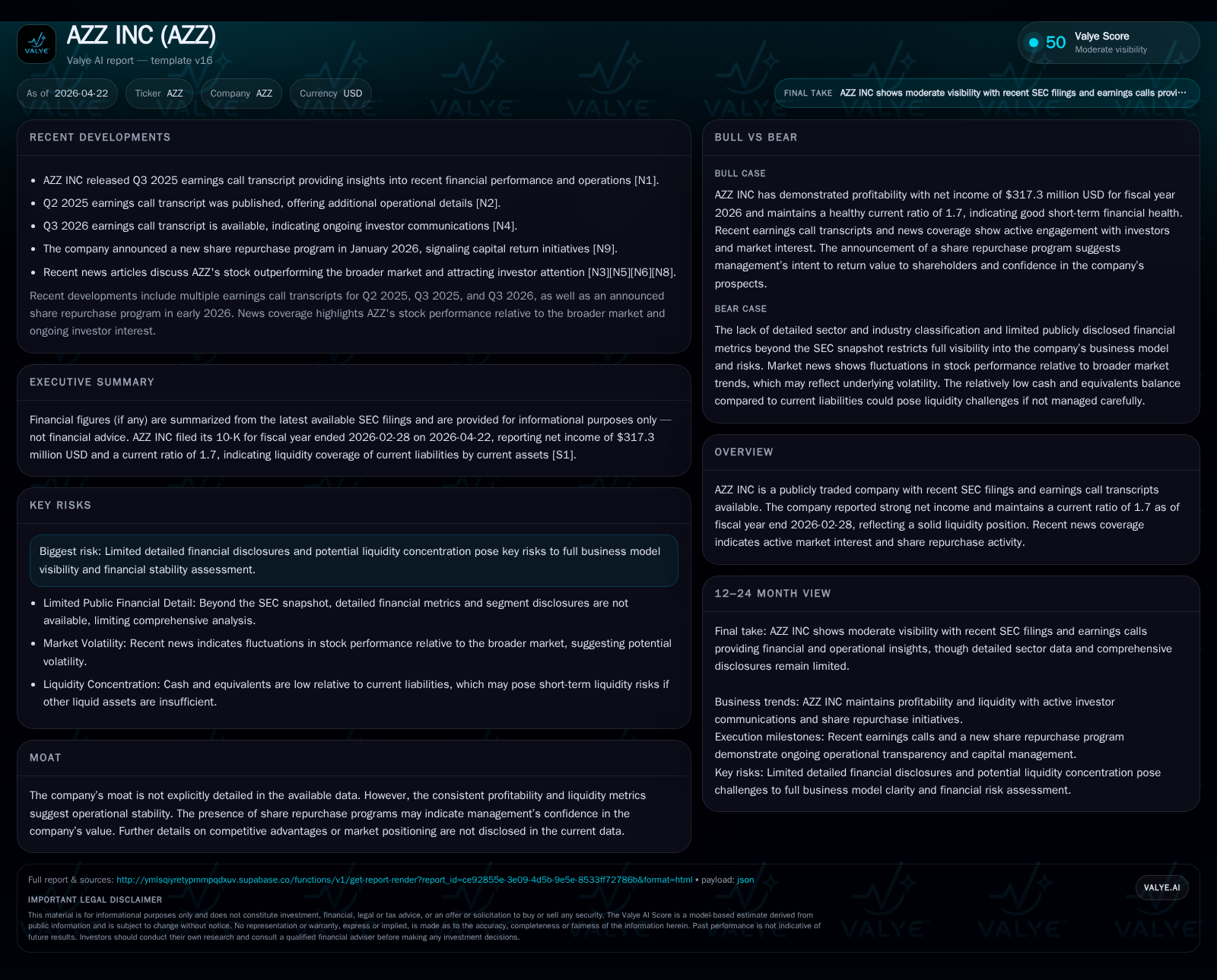

On April 22, 2026, AZZ Inc. reported its fiscal year ended February 28, 2026 results emphasizing a substantial surge in net income to $317.3 million. This improvement largely reflects a sharp increase in equity earnings from its non-controlling 40% interest in the AVAIL Infrastructure Solutions joint venture, which posted $209.7 million in equity earnings — up significantly compared to prior periods — bolstered by gains on disposal of the Electrical Products Group and Welding Services Business [S3][S1]. No quarterly filing intervened between FY2025 and FY2026 results; thus, this annual release marks a material near-term update highlighting operational expansion through strategic JV asset monetizations.

Cash generation from operations reached an impressive $525.4 million for the period, reinforcing AZZ's liquidity position (current ratio ~1.7) and facilitating shareholder returns through dividends and share repurchases [F1][S1]. While no detailed guidance beyond first quarter FY2027 sales price expectations was provided, management underscored seasonally normal volumes supporting demand continuity in core segments.

Multi-Segment Business Model: Hot-Dip Galvanizing, Coil Coating, and JV Infrastructure Solutions

AZZ organizes its operations into three distinct operating segments:

AZZ Metal Coatings: This segment leads North America as an independent provider of hot-dip galvanizing and related metal coating services essential for corrosion protection across steel fabrication industries. Its metallurgical process involves molten zinc reacting with steel substrates to extend product lifecycles by several decades. AZZ operated 42 galvanizing plants plus additional surface technology facilities as of FY2026 [S1]. The breadth of site footprint underpins capacity advantages enabling localized service and logistics benefits essential for industrial fabricators.

AZZ Precoat Metals: Focused on coil coating solutions using customer-owned bare metal substrate (steel/aluminum), this segment provides both corrosion protection and aesthetic finishes tailored primarily for construction, HVAC, appliance, container packaging, transportation, and other diversified end-markets. While paint prices have increased recently, the associated costs are largely passed through to customers mitigating margin risk [S1]. Availability of substrate inputs remains stable.

AZZ Infrastructure Solutions: Represented by a 40% ownership stake in AVAIL JV (AIS Investment Holdings LLC), this segment develops infrastructure transmission power products and automated weld overlay systems that enhance corrosion/erosion resistance vital to critical infrastructure globally [S1]. Recent asset sales within the JV materially contributed to elevated equity earnings reported in FY2026 [S3].

The multi-pronged business model combines steady manufacturing/service operations with a strategic minority investment structure that allows capture of high-value infrastructure project economics without full operational burden.

Competitive Positioning within North American Metal Coatings Industry

Within hot-dip galvanizing services—a technically specialized yet commoditized metallurgical process—AZZ maintains scale leadership with extensive plant assets concentrated across North America [S1]. This positioning supports customer retention via proximity advantages amidst regional complexity of transporting heavy coated steel products.

Supply-side factors emphasize raw substrate availability as critical; however, currently no substrate shortages have been noted impacting coil coating volume [S1]. Paint materials are another key input but are fully passed on to customers reducing risk exposure.

Natural gas usage is a principal raw material powering continuous coil coating lines; however, pricing can be volatile creating potential cost pressure variability [S1]. Additionally, competitive pricing tension persists around selling prices influenced by product mix fluctuations inherent to the construction-driven client base.

Costs associated with operating multiple surface treatment technologies including powder coating and anodizing further differentiate service capabilities vis-à-vis smaller competitors lacking scale or integrated offerings.

Growth Levers: Infrastructure JV Divestitures, Demand in Core End Markets, and Pricing Outlook

AZZ’s compound growth drivers rest on several pillars:

- The significant increase in equity income from AVAIL JV following divestitures enables capital redeployment flexibility while generating recurring free cash flow streams tied to global infrastructure investments [S3][S1].

- Ongoing demand for corrosion protection solutions in electrical utilities, construction frameworks, and industrial equipment sustains volume baselines across Metal Coatings segment despite typical seasonality [S1][N1].

- Precoat Metals pricing shows upside potential as inflationary pressures allow incremental pass-through increases on raw materials alongside value-additional pricing adjustments reflecting mix changes [S1].

- Stable seasonal volume patterns are expected heading into fiscal 2027 providing visibility into operational cadence.

- Shareholder capital return programs including dividends (~$23 million paid) plus active share buybacks ($20 million repurchased) underline management’s confidence in cash flow durability [F1][S10].

Overall pricing power appears moderate yet defensible due to product differentiation supporting extended lifecycle benefits critical to customers’ long-term asset planning.

Challenges: Cyclical Seasonality, Input Cost Volatility, and Market Price Pressures

Despite stable medium-term prospects, AZZ faces ongoing challenges:

- Its business exhibits inherent cyclicality linked closely to North American construction sector seasonality—with higher activity during warmer months—resulting in lumpy volume realization adversely affected during winter quarters or severe weather episodes [S1].

- Natural gas price fluctuations exert cost volatility on coil coating operations which cannot be entirely mitigated despite pass-through protections on paint costs [S1].

- Pricing pressure exists from competitive fragmentation and commoditized input materials requiring continuous operational efficiency improvements; recent restructuring charges related to closure of two surface technology plants aim at cost optimization reflecting these imperatives [S1].

Such factors cap margin expansion potential absent supportive macro trends or technological innovation breakthroughs that could change capacity utilization dynamics or enable premium offerings.

Upcoming Catalysts and Monitoring Points

Key areas warranting close attention include:

- First quarter fiscal 2027 financial updates detailing actual sales price execution across Metal Coatings and Precoat Metals segments vis-à-vis inflation pass-through strategies.

- Potential further divestiture or restructuring initiatives within AVAIL JV that could impact equity income contribution cadence or corporate liquidity.

- Execution progress on operational streamlining efforts particularly given recent resizing of surface technology facilities that may alter fixed cost structure.

- Capital allocation decisions signaling board confidence such as incremental buybacks or dividend maintenance amid shifting sectoral investment landscapes.

- Macroeconomic conditions including regulatory developments influencing infrastructure spending patterns where the infrastructure solutions JV participates globally.

Tracking these milestones will provide directional clarity on whether current profitability trajectory sustains against industry cyclicality backdrop.

Financial Profile and Capital Allocation: Earnings, Cash Flow, and Share Repurchases

Supporting these strategic facets is a robust financial profile characterized by strong operating metrics detailed below:

Historical performance (annual)

| FY | Net ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2026 | 317 | 265 | 81 | +146.3% |

| 2025 | 129 | 236 | 116 | +26.8% |

| 2024 | 102 | 222 | 95 | +291.8% |

| 2023 | -53 | 174 | 57 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2026 | 23 | 20 | 23.7 |

| 2025 | 23 | 12.3 | |

| 2024 | 31 | 0 | 14.5 |

| 2023 | 23 | 0 | -6.2 |

Source: SEC companyfacts cache [F1].

Net income jumped roughly +146% YoY boosted mainly by the AVAIL JV equity earnings leap (+$193 million increase), while operating income grew +12% supported by segment profit stability augmented by restructuring-driven cost improvements [F1][S1][S3]. Operating cash flows also soared over fivefold versus prior comparable periods reflecting improved working capital management paired with high-quality earnings conversion.

Capital expenditures declined ~30%, aiding free cash flow generation estimated at approximately $445 million after capex deductions [F1], facilitating balanced capital returns executed via dividends sustained at prior levels alongside new share repurchase activity totaling $20 million during FY2026 [F1][S9][S10]. Liquidity remains well managed with current ratio approximated at 1.7 reflecting ample short-term asset coverage over liabilities [F1].

This financial strength affords AZZ flexibility amid typical sector cyclicality while underpining investor-aligned cash deployment priorities.

This analysis synthesizes company disclosures without investment advice or recommendation. It thoroughly anchors current developments embedded within AZZ’s longer-term operational framework critical for informed stakeholder assessments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments