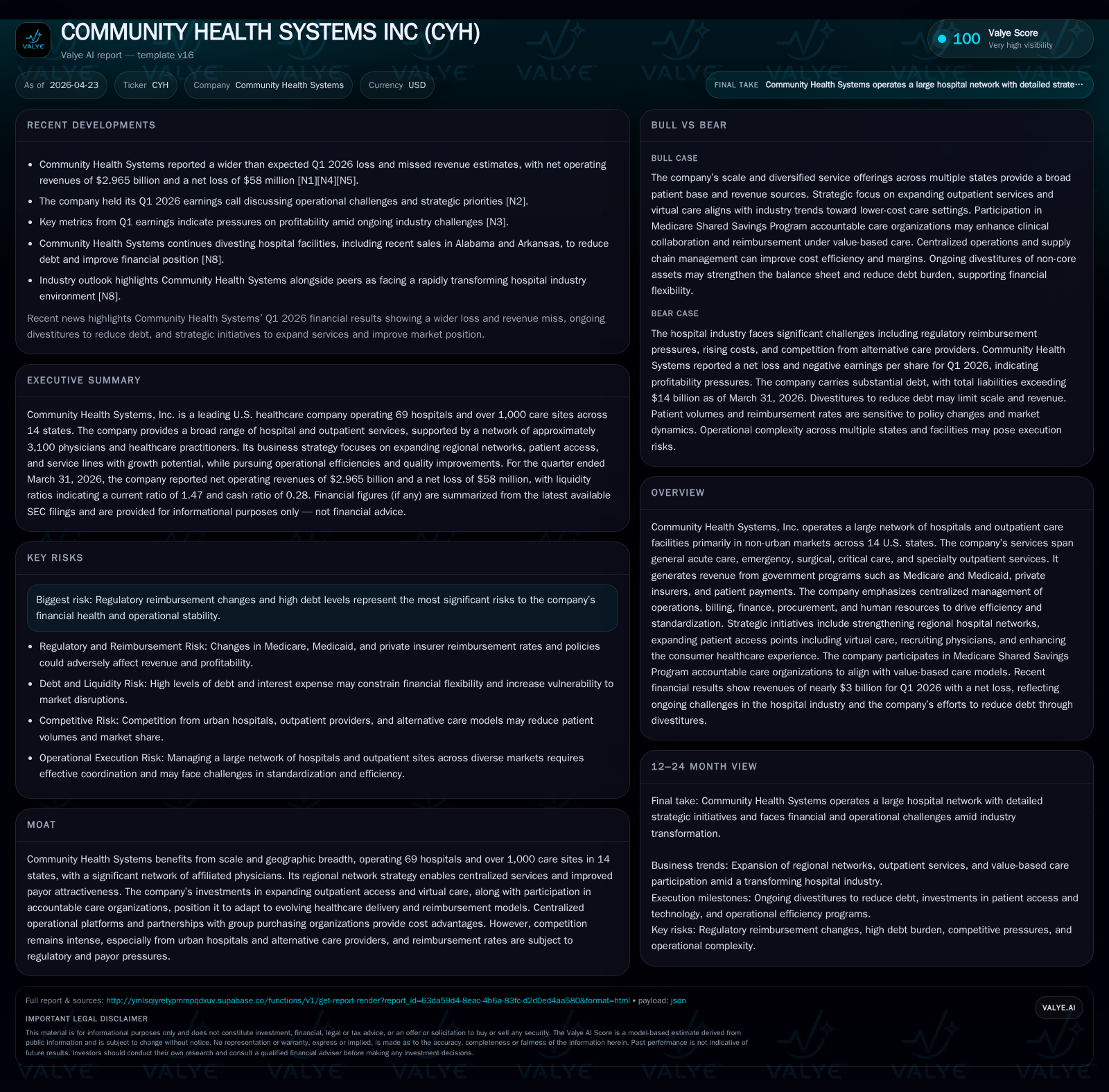

Community Health Systems Eyes Stabilization as Quarterly Results Reveal Operating Pressures

Q1 2026 filings spotlight charity care impact and Medicaid reimbursement challenges amid CHS’s strategic outpatient expansion and heavy leverage.

Community Health Systems’ latest 10-Q filing reveals continuing operational headwinds from charity care exclusions and uncertain Medicaid supplemental reimbursements, affecting near-term revenues. The company’s extensive non-urban hospital network, supporting diverse acute and outpatient services primarily reimbursed by government programs, faces competitive pressures from urban providers and evolving payor models. Growth is driven by outpatient access expansion and value-based care participation, but regulatory reimbursement shifts and substantial debt weigh on financial flexibility. Key upcoming CMS decisions on Medicaid programs and execution in physician recruitment and outpatient rollout will be critical to watch.

Quarterly Operational Update Sharpens Focus on Charity Care and Reimbursement Nuances

Community Health Systems’ Q1 2026 10-Q filing [S2] foregrounds ongoing challenges in managing charity care alongside Medicaid supplemental reimbursement programs. The company continues to provide uncompensated care to financially indigent patients without pursuing collections; such amounts are excluded from net operating revenue under federal guidelines. This charity care practice reflects patient household income relative to federal poverty levels. To partially offset these costs, CHS relies on state Medicaid supplemental programs that allocate payments not tied directly to individual patient care but intended to compensate providers for treating Medicaid and indigent populations. These programs blend state and federal funds, sometimes funded via provider-assessed fees or taxes.

Importantly, these repayment frameworks require periodic Centers for Medicare & Medicaid Services (CMS) authorization for continuation. Delays or non-renewal of CMS approvals introduce timing risks to revenue recognition from these programs. Market responses post-earnings have underscored concerns about the sustainability of this reimbursement stream amidst a shifting policy environment [N1][N3]. This situates near-term results under pressure as unreimbursed care persists at material levels.

An April 21 event filing [S3] provides complementary updates reinforcing these operational realities without signaling immediate change but underscoring the fraught regulatory backdrop.

Core Business Model: Network Scale, Service Suite, and Revenue Mix

CHS operates an extensive healthcare network consisting of 69 hospitals aggregated across largely non-urban markets within 14 states along with more than 1,000 other sites including physician practices, urgent care centers, ambulatory surgery centers, imaging centers, cancer centers, among others [S1][S11]. These assets collectively serve over 10,000 beds with approximately 1,700 employed physicians plus an additional 1,400 licensed healthcare practitioners supporting a wide clinical footprint.

Revenue streams derive principally from governmental payors—Medicare and Medicaid—as well as private insurance carriers and direct patient payments. The company emphasizes centralized management of finance operations such as billing and collections; procurement partnerships notably through HealthTrust buying group (in which CHS holds an ~11.7% stake) enable cost savings on medical supplies [S8][S26].

The service mix encompasses general acute care alongside emergency services, specialized surgery suites (orthopedics, cardiovascular), critical care units, behavioral health offerings, diagnostic facilities and outpatient services including virtual health visits [S11][S26]. Centralized platforms facilitate standardized processes across geographically dispersed operations while also enabling local tailoring via regional networks to enhance efficiency.

This diversified portfolio serves as a hedge against some payer or segment-specific downturns but also introduces complexity in managing diverse payor contracts and shifting demand patterns—particularly the structural pivot toward outpatient modalities.

Competitive Dynamics in Non-Urban Hospital Networks

CHS’s primary service areas are often smaller or mid-sized urban clusters where it may be the sole or dominant general acute provider [S8]. However, competition arises from municipal or nonprofit hospitals enjoying favorable tax treatment which enables them to finance specialized service capacity beyond CHS’s scope [S5][S15]. Such competitors also benefit from philanthropic funding allowing subsidization not available to for-profit CHS.

Physician alignment is another critical competitive factor since admitting doctors influence patient flows strongly. CHS seeks differentiation through recruitment efforts of primary care physicians and specialists plus fostering collaborative relationships within its affiliated physician network [S19]. However, competing integrated health systems increasingly embed physicians directly or operate via accountable care organizations (ACOs), heightening market competitiveness especially in outpatient arena.

Emerging competition originates from ambulatory surgery centers or specialized outpatient providers incentivized by payor policies favoring cost-effective treatment outside inpatient settings, pressuring traditional hospital inpatient admissions [S5][S23]. This trend reiterates the importance of expanding outpatient capabilities and service integration to maintain market share.

Growth Catalysts: Expansion of Outpatient Access and Accountable Care Participation

Strategic priorities emphasize scaling outpatient access points encompassing freestanding urgent cares, ambulatory surgical centers, imaging facilities alongside broad deployment of telehealth offerings for both hospital-based services and direct-to-consumer modalities [S26][N1]. These expansions respond strategically to shrinking inpatient volumes driven by payor preference for lower-cost settings.

CHS currently participates in eleven Medicare Shared Savings Program ACOs comprising roughly 2,900 physicians—both employed and independent—facilitating risk-sharing arrangements aimed at cost containment while improving quality outcomes [S19]. These initiatives align reimbursement incentives more closely with value-based care paradigms expected to dominate future healthcare economics [S14][S28].

Patient experience enhancements ranging from centralized scheduling systems to digital engagement campaigns further underpin retention strategies by easing navigation across episodes of care [S19]. Expanding virtual platforms unlock convenience factors increasingly valued by consumers thereby strengthening CHS’s competitive positioning in an evolving delivery landscape.

Headwinds: Regulatory Pressure, Medicaid Reimbursement Uncertainty, and Financial Leverage

Regulatory risks loom large as CMS contemplates policy tweaks impacting Medicare/Medicaid payment methodologies inclusive of reduction or modification of supplemental state programs crucial for indigent care funding [S4][S7][S10]. Recent legal challenges against certain Medicaid waiver expansions add uncertainty.

Additionally, the company faces scrutiny risks pertaining to compliance demands under laws such as the False Claims Act (FCA), Anti-Kickback Statute and Stark Law which govern billing integrity and relationships with referral sources [S12][S27]. Continuous auditing activity including RAC program claims review may induce payment recoveries creating cash flow variability.[S1]

From a balance sheet perspective CHS bears a sizable debt load totaling approximately $10.1 billion in long-term obligations at quarter-end [S6][S29]. Although recent proactive redemption of $223 million senior notes at a slight premium signals active liability management efforts reducing weighted average cost or extending maturities; free cash flow generation remains relatively modest constraining optionality versus interest expense burden [F1].[N13]

Seasonal demand fluctuations compound uncertainty; episodic spikes from illness outbreaks further temper volume visibility.[S7]

Key Upcoming Milestones and Market Signals to Monitor

Looking ahead investors should track CMS decisions regarding renewals or restructuring of key supplemental Medicaid reimbursement programs due within coming quarters as these materially affect net revenue realizations under current accounting conventions.[S2]

Execution markers include expansion pace of new outpatient sites (tracking openings vs targets), absorption rates in telehealth utilization growth curves as well as recruitment successes in key physician specialty areas pivotal for service line breadth extension.[N1][N2]

Debt maturity calendars warrant attention particularly surrounding forthcoming refinancing windows that could strain liquidity if capital markets conditions deteriorate unexpectedly.[S6]

Quarterly earnings commentary will offer insight into margin trajectories reflecting mix shifts toward higher-margin outpatient services against fixed cost absorption thresholds.[N3]

Supporting Financial Analysis: Cash Flow, Debt Profile, and Profitability Trends

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.5 | 509 | 543 | 1488 | -1.2% | +198.6% |

| 2024 | 12.6 | -516 | 480 | 542 | +1.2% | -288.0% |

| 2023 | 12.5 | -133 | 210 | 957 | +2.3% | -389.1% |

| 2022 | 12.2 | 46 | 300 | 821 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 208 | -36.5 |

| 2024 | 120 | 27.0 |

| 2023 | -257 | 9.6 |

| 2022 | -115 | -3.4 |

Source: SEC companyfacts cache [F1].

The company’s fiscal year ending December 31, 2025 showed revenues at approximately $12.485 billion with operating income rebounding robustly to about $1.488 billion (+174% YoY) after a challenging prior period [F1]. Net income swung into positive territory at $509 million compared to prior losses indicating improved profitability though absolute margin levels remain pressured.

Operating cash flow expanded moderately (+13% YoY) reaching $543 million while capital expenditures declined slightly to $335 million suggesting conservative reinvestment posture commensurate with focus on efficiency gains rather than aggressive capacity build-outs.[F1]

Liquidity measurements reflect current assets covering liabilities at a ratio near 1.47x providing reasonable short-term cushion amid working capital cycles.[F1] Despite this the negative equity position (~ -$1.39 billion) underscores historically leveraged capital structure constraints requiring vigilant debt servicing discipline.[F1]

Recent amendments to credit agreements including note redemptions convey management’s intent to mitigate interest costs yet overall leverage ratios remain elevated cautioning against operational softness translating into financial distress.[F1][S6][S29]

In sum financials exhibit signs of stabilization supported by scale economies inherent in CHS’s network alongside centralized corporate functions but remain sensitive to reimbursement climate shifts combined with the systemic transition towards outpatient healthcare delivery modalities.

This report presents an analytical overview based exclusively on publicly available SEC filings plus corroborated news transcripts through April 2026 without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments