Vanda Pharmaceuticals: Regulatory Wins Clash with Persistent Losses and Emerging Risks

Exploring Vanda's financial and operational paradoxes against its recent FDA success and unresolved profitability challenges.

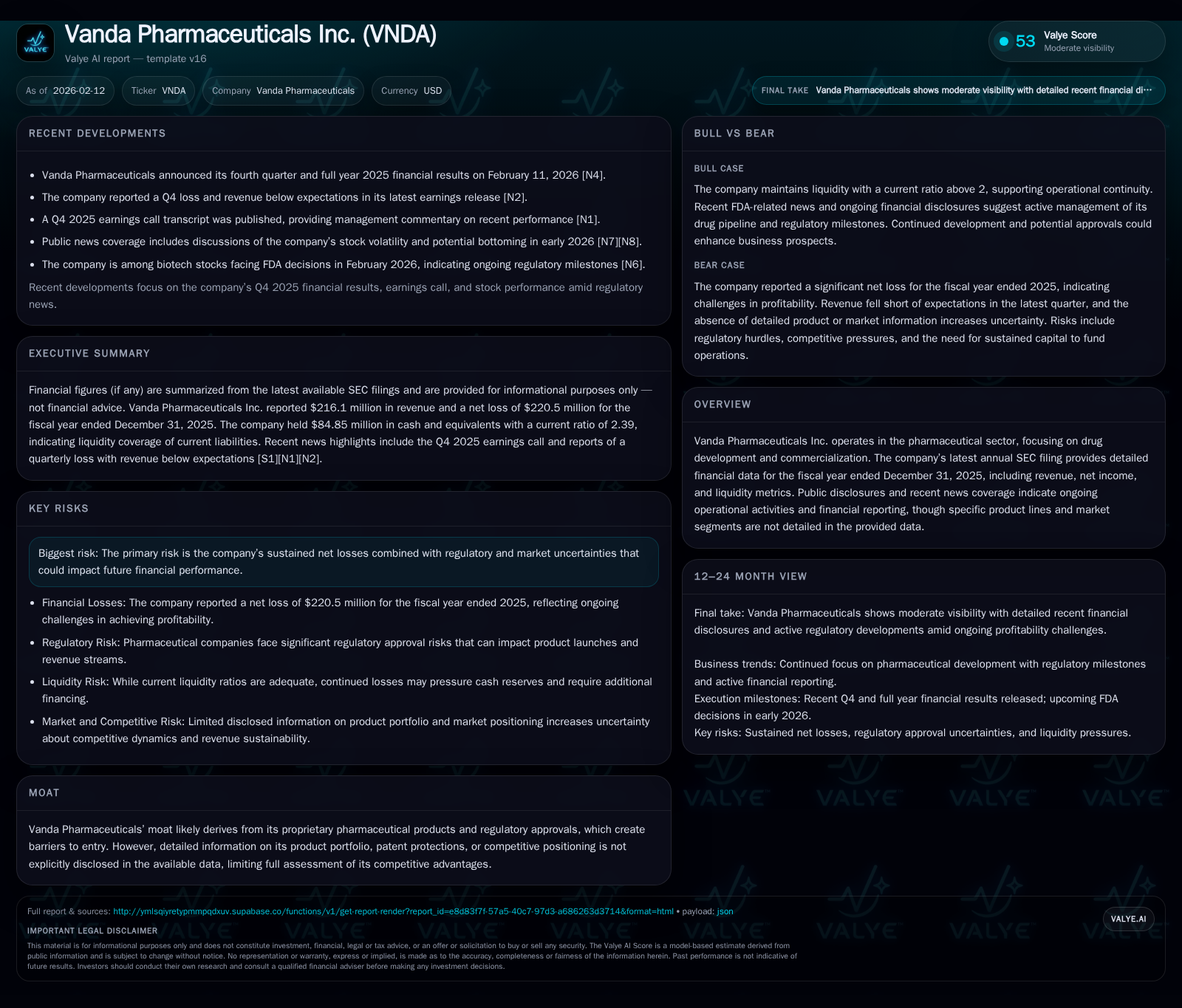

Vanda Pharmaceuticals experienced a significant stock rally late in 2025 following FDA approval of a novel motion sickness drug, underscoring successful regulatory execution. Nonetheless, the company reported a steep $220.5 million net loss on $216.1 million revenue for the full year, signalling ongoing challenges in translating approvals into profitability. With limited public data on its product portfolio and patent strength, Vanda's moat remains opaque but likely tied to proprietary drugs and regulatory barriers. Near-term liquidity appears adequate but warrants scrutiny given current losses and liabilities. Investor sentiment has oscillated sharply with news flow, while sector-wide uncertainties compound operational risks heading into 2026.

From Regulatory Triumphs to Financial Headwinds: Setting The Stage

Vanda Pharmaceuticals crafted a compelling narrative late in 2025 when its stock surged nearly 29% following FDA clearance of a motion sickness drug — a regulatory win that investors initially embraced enthusiastically [N14]. This uplift spotlighted Vanda’s ability to successfully navigate the labyrinthine approval process pivotal in pharma innovation cycles. Yet beneath this celebration lies an uneasy paradox: the same quarter in which these triumphs were publicized also revealed persistent financial distress marked by deeper net losses and revenues that failed to meet market expectations [N2,N1]. The juxtaposition lays bare the complex balancing act facing Vanda — executing on high-stakes regulatory milestones while grappling with structural challenges in financial performance.

This tension between external validation via approvals and internal operational realities became stark during the Q4 2025 earnings release. Despite market excitement fueled by pipeline successes, reported figures underscored the uphill battle to transform regulatory accolades into profitable growth—a narrative that would temper investor enthusiasm as the quarter closed.

Unpacking Vanda’s Revenue Streams and Financial Health in 2025

A granular look at Vanda's fiscal year 2025 performance offers critical insight. The company registered revenues totaling approximately $216.1 million — a noteworthy top line figure indicating substantive sales activity likely linked to existing marketed products or royalties [S1,F1]. Yet this revenue was heavily overshadowed by a net loss soaring to about $220.5 million, highlighting persistent cost pressures far exceeding income generation capacity [F1]. Such losses underscore fundamental challenges in scaling operations profitably amidst intensive R&D spends or marketing efforts.

Examining liquidity paints a cautious but somewhat resilient picture: current assets of $347.3 million versus current liabilities of $145.2 million yield a current ratio near 2.39, suggesting that short-term obligations remain serviceable under present conditions [F1]. Cash and equivalents stood at approximately $84.9 million by year-end — a moderate war chest but one that necessitates close monitoring given ongoing negative earnings trends could accelerate cash depletion absent new inflows or financing [S1].

Together, these figures sketch a company navigating steady if not expanding revenue alongside profound difficulty containing operating expenses—a double-edged sword reflective of early-stage or mid-sized pharmaceutical firms advancing product pipelines yet not fully leveraged commercially.

The Moat Mystery: Assessing Vanda’s Competitive Defenses Amid Sparse Public Detail

Determining Vanda’s sustainable competitive advantage proves challenging due to limited public granularity on its drug portfolio, intellectual property holdings, or explicit market positioning [valye_report_excerpt.moat]. However, industry conventions suggest that proprietary pharmaceuticals granted FDA approvals inherently provide barriers — including patent protections and regulatory exclusivity periods restricting generic competition.

Given Vanda’s demonstrated ability to secure such approvals recently, it's plausible that its moat is constructed around these regulatory shields coupled with specialized formulations addressing niche therapeutic areas (such as motion sickness). Nevertheless, without detailed disclosure on patent life spans or pipeline breadth, assessing durability or differentiation relative to peers remains speculative.

This opacity forces reliance on indirect inference: in biotech sectors where commercial success often hinges on protected innovation funnels, approval achievements imply at least temporary competitive defenses though long-term moat strength depends on replenishing breakthroughs and market adoption trajectories.

Navigating the Losses: What Drives Vanda’s Continued Red Ink?

Delving beyond headline results reveals multiple factors contributing to sustained losses in 2025. Earnings call transcripts emphasize aggressive investment in research & development activities aimed at expanding the clinical pipeline or enhancing existing therapies [N1]. Concurrently, marketing expenditures necessary for drug launches or physician awareness also weigh heavily.

Moreover, commercial ramp-up dynamics may be less than optimal; new products typically require extensive time to penetrate markets deeply enough to offset upfront costs fully. Such lags impact profitability especially if earlier-stage candidate failures punctuate progress cycles.

In aggregate, these elements portray a company functioning largely within growth mode parameters common among mid-tier pharma firms—burning cash today with hopes pinned on future revenue expansions yet without guaranteed timelines for breakeven.

Liquidity Matters: Cash Position and Balance Sheet Robustness Under Scrutiny

From a financial stability standpoint, Vanda’s end-of-2025 cash balance of roughly $84.9 million stands modest relative to its current liabilities tallying about $145.2 million [F1]. While the overall current ratio near 2.39 signals adequate coverage of short-term debts by liquid assets plus receivables/inventories, the concentrated cash component suggests tightened maneuverability if operating losses continue unchecked.

Pharmaceutical companies facing prolonged negative earnings must carefully manage burn rates or consider capital raises/licensing deals to sustain runway; any significant delays or missed milestones could pressure liquidity further.

Hence monitoring subsequent quarterly reports for cash flow trends is critical because solvency risks may escalate absent corrective business performance or financing strategies.

Market Sentiment and Stock Performance: Investor Reactions Post-FDA Approval

The ebbs and flows of investor appetite toward Vanda reflect natural market psychology blending hope with caution. After the December FDA nod led to an immediate 29% jump in share price — fueled by anticipation around new revenue streams from approved indications — sentiment gradually cooled amid emerging details signaling broader operational struggles [N14].

By early January, pre-market sell-offs hinted at skepticism regarding sustainability amid revenue shortfalls reported later for Q4 and broader market headwinds affecting biotech stocks [N9,N8,N2]. This volatility underscores how biotech equities can rapidly oscillate based on incremental data points from regulatory events through earnings results.

Mapping this trajectory unveils an investor base attuned both to promising milestones yet wary of underlying fundamentals prompting more tempered medium-term expectations.

Risks in Focus: Regulatory Uncertainties And Market Pressures Ahead

Beyond internal financial metrics lies an array of exogenous risks confronting Vanda as it navigates forward. The Valye report underscores persistent net loss risk compounded by sector-level regulatory unpredictability such as potential shifts in FDA review frameworks or competitor approvals impacting market access [valye_report_excerpt.risks].

Biotech stocks broadly face heightened volatility around upcoming FDA decisions slated for early 2026 which could indirectly affect funding environments or investor confidence impacting companies like Vanda [N7]. Furthermore, macroeconomic factors including interest rate trends that influence healthcare valuations add complexity independent of operational outcomes.

Consequently, these layered pressures accentuate Vanda’s path dependency on successful product development executions complemented by prudent risk management strategies amid fluctuating external landscapes.

Peer Glance: Comparing Vanda To Industry Revenue and Profitability Benchmarks

Placing Vanda within peer context reveals differentiated momentum gaps reflective of their respective business scales and commercial maturity levels. For instance, Gilead Sciences reported surpassing Q4 earnings estimates with stronger revenue growth illustrating established blockbuster franchises driving stable profits versus nascent players like Vanda still incurring heavy investment-led losses [N3].

Similarly, Intellia Therapeutics exhibited notable stock appreciation fueled by gene-editing breakthroughs signaling investor enthusiasm for disruptive technologies able to translate innovation into eventual commercialization success [N6].

These comparisons illustrate how peers benefit from either diversified portfolios or breakthrough modalities generating positive market feedback loops while Vanda wrestles with narrower late-stage successes counterbalanced by continued cash burn.

What Lies Ahead? Catalysts And Challenges Through 2026

Looking into the near horizon, several potential catalysts may shape Vanda’s trajectory: announcements related to pipeline trial readouts could provide fresh investor interest if positive; expansion into new therapeutic indications following recent approvals might boost revenue prospects; licensing partnerships could improve cash flows.

However, these opportunities coexist with notable headwinds — relentless loss trends constrain reinvestment capacity; regulatory shifts might impose longer review times; mounting competition could erode pricing leverage over time.

Navigating this landscape demands strategic clarity balancing growth ambitions against fiscal discipline while relentlessly advancing product innovation to reinforce potential competitive moats illuminated intermittently through recent successes.

This analysis synthesizes publicly available data including SEC filings and recent news coverage without recommending specific investment actions. Readers are advised to conduct independent research considering evolving information dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments