Westamerica Bancorporation’s Shift from Strong Growth to Cautious Stability in California Small-Business Banking

After years of rapid growth and strategic acquisitions, Westamerica Bancorporation has moved towards measured earnings and disciplined capital management focused on its regional small business niche.

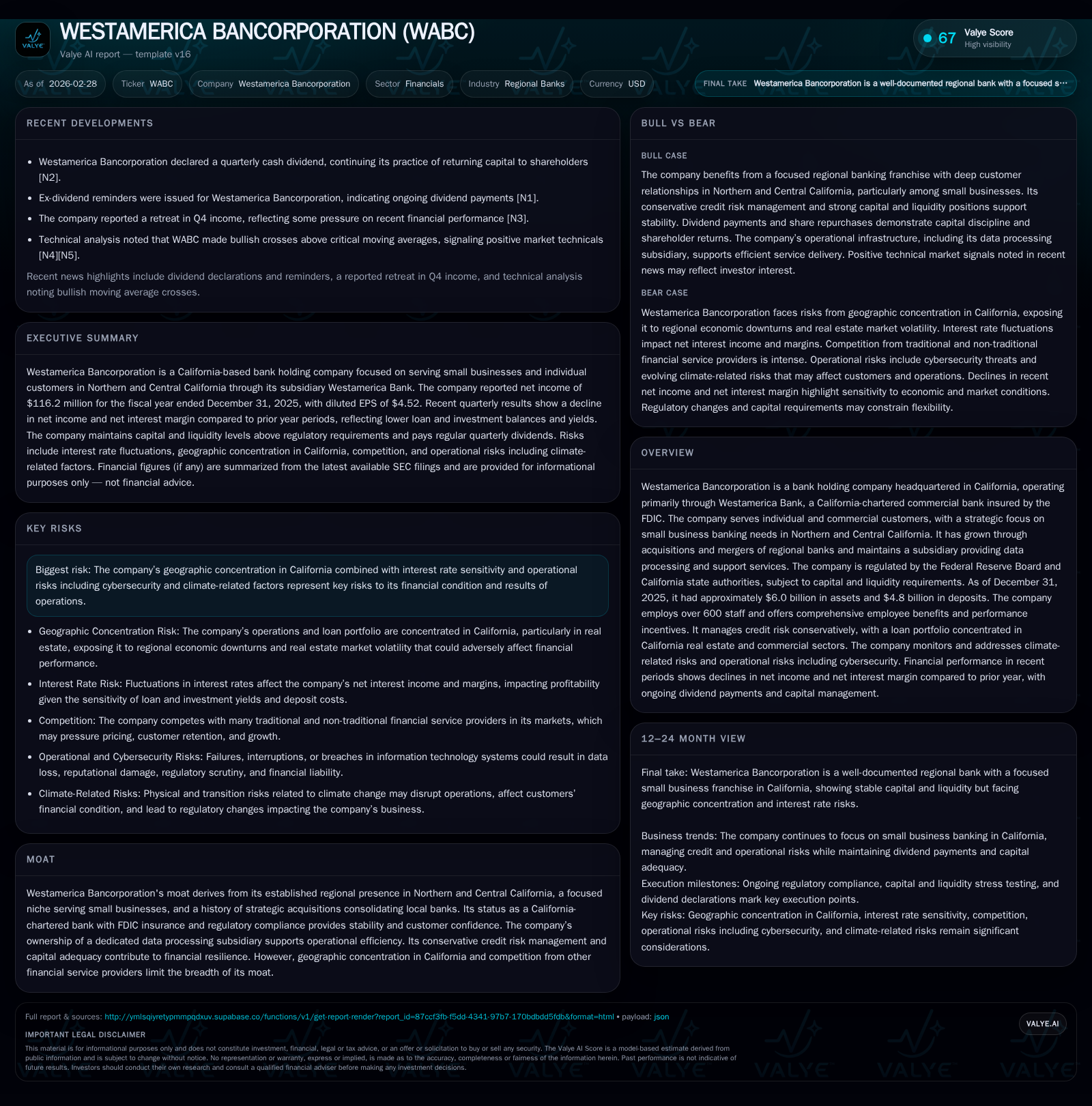

Westamerica Bancorporation (WABC) experienced outstanding net income growth fueled by acquisitions and organic expansion through FY2024 but saw a notable income decline in FY2025 amid margin pressures and heightened competitive dynamics. The company remains strongly capitalized, with a conservative credit posture and continued dividend payments paired with increasing share repurchases. Its concentration in Northern and Central California's small business banking market provides a defensible niche, though geographic and rate sensitivity risks persist. Going forward, the firm’s ability to navigate evolving interest rate environments, loan demand trends, and regulatory expectations will be critical.

Historical Growth Trajectory and Acquisition-Driven Expansion

Westamerica Bancorporation's trajectory over recent years showcases an impressive ascent powered by targeted acquisitions across Northern and Central California markets complemented by organic growth focused on small business banking. According to the company history detailed in the 2026 10-K [S1], Westamerica consolidated multiple regional banks during the 1990s and early 2000s — including notable deals such as ValliCorp Holdings in 1997 — building scale while reinforcing customer relationships within a defined geographic footprint.

This acquisition-driven expansion underpinned net income growth from approximately $39.3 million in FY2022 to $138.6 million by FY2024, representing an extraordinary compound annual growth rate over this period [F1]. Such scale gains also brought operational leverage and stronger deposit bases critical for lending capacity.

However, after peaking in FY2024, net income contracted by roughly 16.2% in FY2025 to $116.2 million [F1], marking a shift from rapid growth to cautious earnings stability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 116 | 122 | 2 | -16.2% |

| 2024 | 139 | 142 | 2 | +251.3% |

| 2023 | 39 | 158 | 1 | +0.3% |

| 2022 | 39 | 114 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 47 | 104 | 120 |

| 2024 | 47 | 0 | 140 |

| 2023 | 46 | 14 | 157 |

| 2022 | 45 | 0 | 113 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary (FY2022-FY2025) drawn from [F1]

Dynamics Behind Recent Income Contraction and Margin Pressures

The net income contraction observed in FY2025 alongside roughly a 13.9% decline in operating cash flow highlights tightened operational conditions for WABC [F1,S2,N3]. Q4 commentary from Nasdaq noted net interest margin (NIM) compression as a primary driver due to competitive pressures on deposit pricing as the bank sought to retain and grow its deposit base amid fluctuating Federal Reserve policies [N3].

While the provision for credit losses remained flat or slightly reversed (-$550k reported for certain periods), signaling stable asset quality through conservative underwriting practices including robust portfolio monitoring overseen by the Loan Review Department ([S2],[S9]), revenue pressures were significant enough to offset these mitigating factors.

Interest-rate sensitive lending means increased funding costs from more attractively priced deposits squeezed spread income temporarily despite asset-sensitive positioning ([S14]). Additionally, noninterest incomes declined marginally, exacerbating pressure on overall earnings before taxes.

Strategic Positioning within California’s Small Business Banking Ecosystem

WABC's moat is principally rooted in its focus on relationship-driven banking services tailored specifically for small businesses across a concentrated set of Northern and Central Californian counties spanning Mendocino to Kern Counties ([S1]). This geographical coherence fosters localized customer intimacy not easily replicated by larger national players.

The loan portfolio emphasizes commercial loans reflective of this SME customer base where collateralization is carefully scrutinized along with borrowers’ operational performance ([S6]). Deposits are similarly relationship-centric with strong reliance on non-interest bearing demand deposits and money market checking accounts that offer stable low-cost funding advantages but also require focused ongoing client engagement given heightened regional competition ([S4],[S22]).

Despite this niche positioning providing differentiation benefits, concentration risk remains an inherent limitation arising from dependence on California’s economic cycles including exposure to climate-related physical risks such as wildfire impacts noted by management ([S9],[S21]).

Capital Allocation Approach: Dividends, Buybacks, and Prudence

Capital discipline characterizes WABC’s shareholder return policy balancing steady dividends with opportunistic share repurchases that escalated sharply starting FY2023 through FY2025 ([F1],[N1],[S13]). Annual dividends held stable around $47 million with payout ratios approximating one-third to two-fifths of net income demonstrating prudent constraint maintaining capital buffers.

Contemporaneously, buybacks rose dramatically from nominal historical levels ($218k in FY2022) to $103.7 million by end-FY2025—a deliberate repositioning to enhance capital efficiency alongside constrained organic growth prospects ([F1],[S16]). This move presumably reflects management confidence in valuation levels paired with ongoing earnings capacity enabling sustainable buyback execution without threatening liquidity.

The resultant approximate return on equity figure of about 12.4% for FY2025 suggests effective profit generation relative to equity base (~$934 million end-‘25) while preserving robust capitalization fundamentals ([F1],[S16],[S7]).

Risk Profile: Geographic Concentration and Interest Rate Exposure

Operating predominantly within California confines WABC significantly exposes it to local economic cyclicality along with sector-specific risks such as agriculture loan concentrations susceptible to drought or commodity price volatility ([S9],[S21]). Environmental considerations are proactively integrated into lending policies requiring flood insurance on certain collateralized real estate loans while monitoring water resource access among agricultural borrowers mitigates but does not eliminate these vulnerabilities.

Interest rate risk is another salient factor where WABC maintains an asset-sensitive balance sheet deliberately structured using third-party models conforming with Federal Reserve supervisory guidance ([S14]). This configuration typically amplifies earnings positively when rates rise but conversely could compress margins if rates flatten or unexpectedly fall given competitive deposit obligations.

Regulatory compliance around capital adequacy remains rigorous with WABC comfortably exceeding 'well-capitalized' thresholds including Common Equity Tier 1 ratios above 22% at year-end 2025 while undergoing periodic stress testing under multiple scenarios reaffirming resilience ([S7],[S12],[S26]).

Key Financial Ratios Spotlight - ROE, Liquidity, and Credit Quality Trends

Aside from ROE hovering near a solid ~12.4%, liquidity management continues focusing heavily on maintaining ample high-quality liquid assets encompassing cash reserves plus investment-grade securities valued over $4 billion mostly classified as held-to-maturity or available-for-sale ensuring quick access if requisite ([S15],[F1]).

Allowance for credit losses remains adequate though modest reflecting conservative underwriting standards augmented by dedicated internal loan review capabilities reporting directly to the audit committee ([S6],[S25]). No significant provisions were required even amid macroeconomic uncertainties.

Operating efficiency is further enhanced through strategic ownership of Community Banker Services Corporation, delivering centralized data processing and back-office efficiencies thus controlling operating expenses better than peers reliant on outsourced technology services ([S1]).

What To Watch Next: Earnings Milestones, Regulatory Changes, and Loan Demand

Investors should monitor forthcoming quarterly earnings results for signs of stabilization or recovery within net interest margin amid evolving Federal Reserve policy trajectories post-2025,[N3],[S2] especially considering re-pricing dynamics for both assets and liabilities.

Competitive intensity around deposit gathering among regional banks will also shape funding cost curves affecting overall profitability potential.[S22] Additionally, any shifts in commercial loan demand driven by California's economy notably among small businesses will materially impact future revenue streams.[S11]

Regulatory developments related to community bank leverage ratio frameworks or heightened climate-related disclosures could alter capital planning approaches though no immediate elections have been declared.[S7]

Operational Support through Subsidiary Services Enhancing Efficiency

A distinctive feature underpinning Westamerica Bancorporation's operational model is its wholly owned subsidiary Community Banker Services Corporation (CBSC), which offers dedicated back-office functions including data processing crucial for streamlined operations invisible often within bank financial disclosures but vital for managing complexity across merged entities spanning multiple counties ([S1]).

This vertically integrated approach reduces reliance on third-party processors common among smaller banks thereby improving cost structure adaptability especially important given tight margin environments faced since mid-2024 onward.

This analysis leverages factual disclosures extracted primarily from Westamerica Bancorporation’s SEC filings through February 27, 2026 combined with validated financial data series up to fiscal year-end December 31, 2025 presented via XBRL datasets [F1] without speculative extrapolation. There are no recommendations or forecasts provided herein; readers should consult official filings directly for formal guidance statements. The company's clear transition from high-growth acquisition phases into measured capital return balances coupled with robust credit management defines its present strategic character within the Californian community banking space. Future performance will critically depend on external macroeconomic shifts plus internal execution amid localized market challenges.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments