WESCO International's Operational Moat and Navigating Recent Earnings Challenges

Examining WESCO's scale, leadership shifts, and financial health amid mixed earnings responses reveals its resilience and risks.

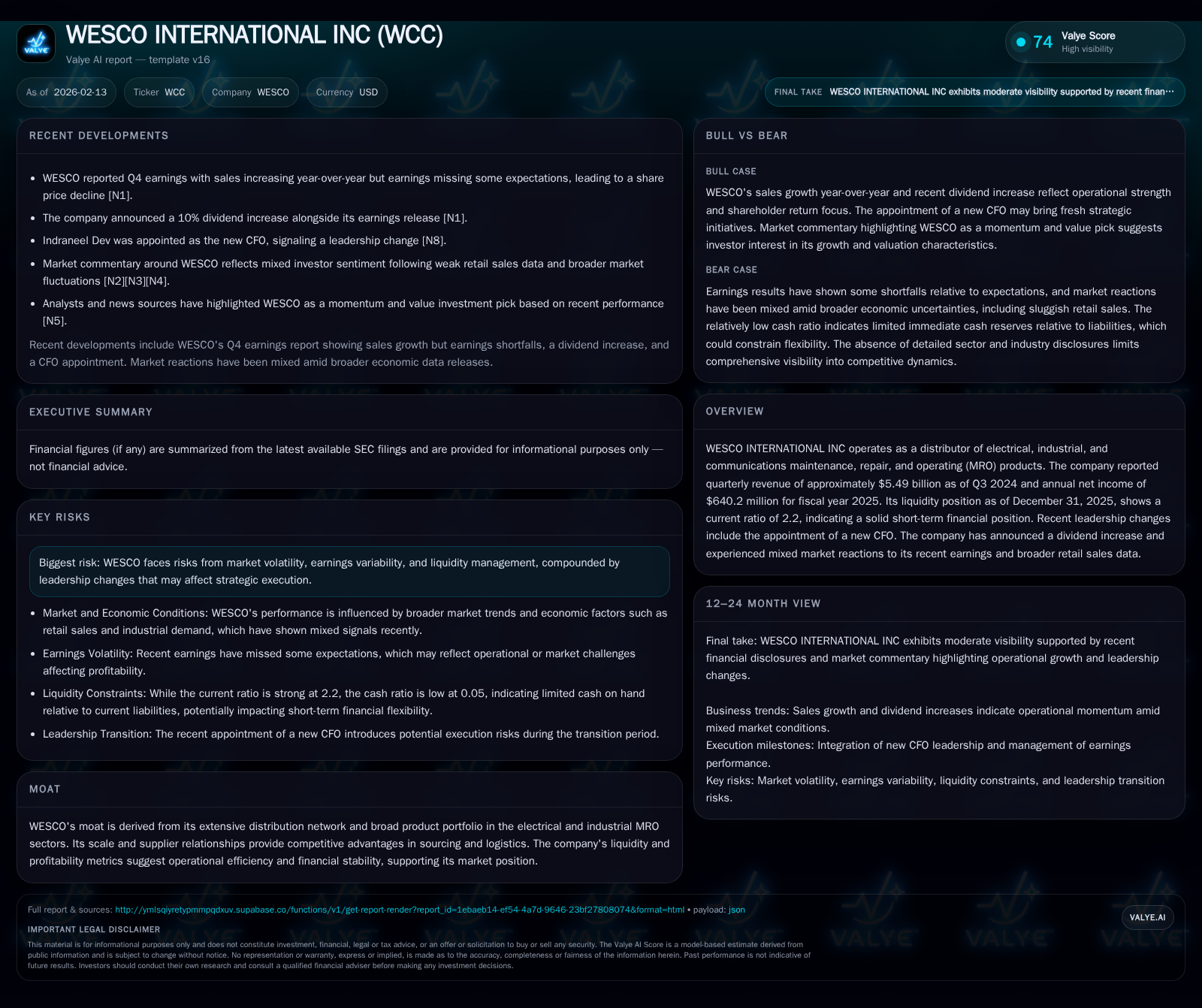

WESCO International remains a formidable player in electrical and industrial MRO distribution owing to its extensive network and supplier relationships. Despite reporting solid revenue growth in Q4 2025, the company’s earnings missed market expectations, triggering a share price decline. Leadership changes, especially the appointment of a new CFO, coupled with conservative guidance and a dividend increase, underline both strategic recalibration and confidence in liquidity. Broader market volatility and sluggish retail data compound short-term pressures but WESCO's balance sheet strength provides stability for near-term navigation.

WESCO’s Moat: Strength in Scale and Distribution

WESCO International firmly anchors its competitive position through an expansive distribution network spanning electrical, industrial, and communications MRO products. As of Q3 2024, the company generated approximately $5.49 billion in quarterly revenues[ F1 ], underscoring significant scale that facilitates advantageous supplier negotiations and optimized logistics. Its comprehensive product palette caters to diverse end markets, reinforcing customer retention and breadth of service.

This size is not merely about top-line magnitude but translates into operational efficiencies reflected in sound profitability metrics — with net income reported at $640.2 million for fiscal year 2025[ F1 ]. Moreover, WESCO maintains a healthy current ratio of 2.2 as of December 31, 2025[ F1 ], signifying that current assets comfortably exceed liabilities and supporting day-to-day operations without undue liquidity strain. Such financial sturdiness underpins the company's moat by sustaining investment capacity and resilient supply chain management.

The firm's longstanding supplier relationships enable stable sourcing while leveraging volume discounts—a cornerstone advantage in a sector characterized by tight margins. While distributorships face commoditization risks broadly within industrial supply chains (analysis), WESCO's integrated approach combining scale with depth remains a durable barrier against fragmented competition.

Decoding Q4 Earnings: Growth versus Expectations

The earnings release for Q4 2025 presented a nuanced picture. Revenues increased year-over-year, affirming underlying demand momentum within the MRO landscape[ N1 ][ N4 ]. However, despite the top-line gain, reported earnings missed analyst consensus estimates[ N1 ][ N3 ], highlighting pressure on profitability that investors often react to sharply.

Contrasting these dynamics is the paradoxical rise in absolute profit dollars alongside falling share prices post-announcement[ N14 ]. This disconnect suggests that market participants prioritized margin compression or margin quality concerns over headline net income figures. Investors appeared sensitive to the trajectory of costs or possibly particular one-time items discussed on the earnings call transcript that may have clouded near-term outlooks[ N2 ].

The mixed reception underscores how even companies with positive sales growth can face headwinds when costs or execution nuances unsettle earnings expectations. WESCO’s ability to manage these margins going forward will be critical in restoring investor confidence.

Leadership Evolution: New CFO and Strategic Implications

Amid this earnings complexity, WESCO appointed Indraneel Dev as new Chief Financial Officer – a pivotal leadership change at the helm of financial stewardship[ N7 ][ valye_report_excerpt ]. The timing amplifies scrutiny on corporate strategy execution during a period marked by earnings unpredictability.

CFO transitions can herald shifts in capital allocation priorities, cost structure oversight, or reporting transparency – all areas particularly relevant given recent financial outcomes. While executive turnover introduces inherent uncertainty (analysis), it also opens avenues for fresh strategic approaches that could enhance operational resilience or unlock efficiencies.

How Mr. Dev aligns financial management with broader company goals will likely influence investor perceptions as FY26 unfolds.

Liquidity and Financial Health Anchors Stability

WESCO's liquidity profile emerges as a pillar of stability amid operational fluctuations. The company reported $9.46 billion in current assets against $4.30 billion in current liabilities at year-end 2025 — translating to a current ratio of approximately 2.2[ F1 ]. This buffer indicates sufficient short-term resources to cover obligations without refinancing stress.

Strong liquidity is crucial for distributors who must balance inventory holdings against working capital constraints especially during periods of macroeconomic uncertainty or uneven demand cycles (analysis). WESCO’s cash position thus serves as a financial shock absorber enabling continued investment in inventory breadth and infrastructure despite episodic market volatility.

This financial footing arguably provides the company with maneuvering space absent for smaller players more vulnerable to capital market disruptions or tightening credit conditions.

Dividend Increase: Signal or Counterbalance?

In February 2026, WESCO announced a dividend increase of approximately 10%, signaling confidence in generating steady cash flows even as it simultaneously guided FY26 sales below analyst estimates[ N13 ][ valye_report_excerpt ]. This dual communication illustrates a nuanced narrative: rewarding shareholders while managing expectations conservatively.

From one angle, the dividend boost can be interpreted as a reaffirmation of ongoing operational strength and commitment to shareholder returns – potentially appealing to income-focused investors.[ analysis ] Alternatively, increasing dividends amid lowered guidance may be viewed as compensatory to offset disappointment on growth forecasts or an effort to stabilize investor sentiment amid shorter-term uncertainties.[ N13 ]

Market reaction was tepid-to-negative with shares edging down approximately 5% following the guidance update reflecting skepticism about near-term growth prospects despite dividend generosity.

External Factors: Market Volatility and Retail Data Impact

WESCO's pricing and operational environment does not exist in isolation from broader macroeconomic trends impacting industrial distributors worldwide. Recent episodes of stock market declines preceding U.S. jobs reports as well as weak retail sales statistics have sown jitters amongst investors broadly[ N8 ][ N10 ][ N11 ].

Sluggish consumer retail spending indirectly pressures industrial MRO companies by tempering construction activity or manufacturing output needed for demand.[ analysis ] These external headwinds exacerbate internal concerns over earnings variability leading to heightened volatility in share price movements despite underlying business scale.

Such contextual factors remind analysts that trading performance often reflects complex interplay between micro fundamentals and wider economic sentiment rather than company-specific issues alone.

Risks and Challenges on the Horizon

While no material changes arose to risk disclosures per latest filings[ S2 ][ valye_report_excerpt ], persistent challenges include exposure to cyclical swings inherent in MRO demand cycles combined with heightened sensitivity due to leadership transitions affecting strategic continuity.

Liquidity management remains a watchpoint especially if revenue growth falls short while inventory requirements stay elevated—any misalignment might stress working capital beyond forecasts (analysis). Earnings consistency is another concern given recent misses; variability could impact investor trust if not addressed through disciplined cost control or margin improvements.

These enduring risks require vigilant management focus as well as clear communication strategies amid an unpredictable external backdrop.

Strategic Outlook: Navigating Below-Estimate Guidance

Guidance issued for fiscal year 2026 indicated sales expectations below consensus forecasts driving cautious forward-looking stances from analysts[ N13 ][ N6 ]. The management narrative acknowledged ongoing macro uncertainties coupled with competitive dynamics challenging growth acceleration efforts.

Yet continued investment in capabilities alongside leveraging established distribution infrastructure suggests long-run resilience even if short-term momentum moderates.[ analysis ] Leadership appears intent on balancing prudent fiscal discipline against tactical investments tailored to differentiated customer offerings.

Such calibrated navigation may help sustain WESCO's moat while addressing emerging competitor challenges within evolving MRO landscapes.

Peer Comparison: Contextualizing Performance in Industry

Placing WESCO alongside peers offers perspective on relative positioning. Arrow Electronics recently surpassed Q4 earnings and revenue expectations presenting contrast where some competitors outperform consensus notably amidst similar macro conditions[ N5 ].

This comparison highlights both areas where WESCO’s execution could catch up—particularly around margin expansion—as well as its entrenched advantages like liquidity strength not universally shared across competitors.[ analysis ]

Such benchmarking underlines that while pockets of risk exist internally or at sector level, WESCO retains competitive durability if it addresses emerging gaps promptly.

Investment Thesis: Balancing Momentum with Caution

Synthesizing available data reveals a company straddling powerful operational foundations against headline-level challenges from recent earnings results and leadership turnover.[ N9 ][ N12 ][ valye_report_excerpt ]

Momentum advocates point to sizable distribution network scale combined with profitability improvements fueling positive medium-term outlooks.[ N9 ] Meanwhile cautious voices highlight episodic profit misses alongside macroeconomic volatility warranting measured appraisal.[ N12 ]

Ultimately, WESCO’s scenario demands both appreciation for fundamental strength and awareness of transitional risks shaping near-term outcomes — crafting an intricate investment landscape rather than straightforward narratives.

This report aims solely to provide an analytic perspective on WESCO International Inc., synthesizing publicly available information without issuing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments