Armada Acquisition Corp. II: Navigating the SPAC Frontier with Capital Discipline and Unfolding Merger Prospects

An in-depth analysis of Armada Acquisition Corp. II's financial foundation, governance, and strategic outlook amid its pivotal pre-business combination phase.

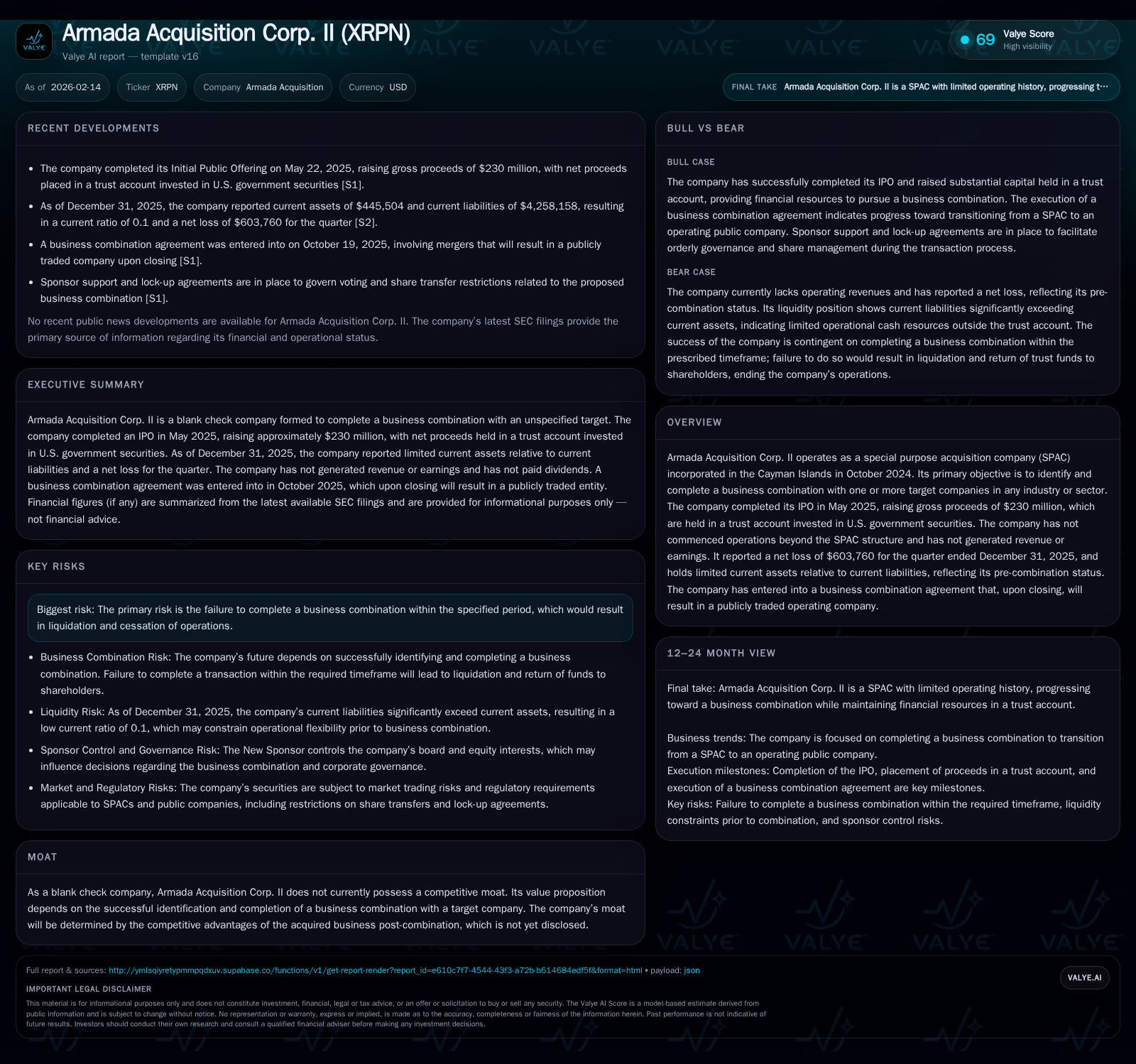

Armada Acquisition Corp. II, a Cayman Islands-incorporated SPAC formed in late 2024, raised $230 million through its May 2025 IPO to pursue a currently undisclosed business combination. Its financial disclosures reflect the typical pre-combination profile characterized by minimal operating activity and reliance on trust account capital invested conservatively in U.S. government securities. Governed under a structure where sponsors fund operations without reimbursement, Armada faces the inherent risk of liquidation should it fail to consummate a merger by the deadline. Market engagement remains limited, with highly concentrated shareholdings observed. Going forward, the company’s value and competitive moat remain contingent solely upon the success of its forthcoming acquisition.

Spotlight on Armada Acquisition Corp. II: Purpose and Structure

Armada Acquisition Corp. II emerged onto public markets in October 2024 as a Cayman Islands-registered special purpose acquisition company (SPAC). By design, its existence is focused narrowly on identifying one or more private companies suitable for combining into a publicly traded entity through the SPAC shell. This structure inherently offers no operating history or revenue-generating activity; Armada currently functions solely as an investment vehicle awaiting its transformative merger event [S1][S2][F1].

Legally domiciled offshore, this setup grants certain operational flexibilities often leveraged by SPACs concerning governance, tax structuring, and cross-jurisdictional deal-making preferences. However, it also imposes investor scrutiny regarding transparency and governance controls during the latent phase preceding any de-SPAC transaction.

IPO Proceeds and Trust Account: Navigating Capital with Discipline

In May 2025, Armada successfully raised gross proceeds amounting to $230 million through its IPO issuance of 23 million units priced at $10 each. The underwriting syndicate led by Cohen and Northland commanded substantial fees tallying approximately $14.4 million split between immediate cash payments and deferred amounts payable upon business combination consummation [S1][F1].

Post-expense net proceeds have been securely placed in a trustee-controlled account invested conservatively in U.S. government securities to preserve principal and provide liquidity necessary for future acquisition funding [S1]. This fiscal discipline exemplifies standard SPAC trust practices designed to mitigate downside risk for investors by shielding funds from operational creditors' claims prior to merger execution.

Financial Snapshot: Reading Between the Lines of Pre-Combination Numbers

The quarter ended December 31, 2025 reveals results typical of pre-combination SPACs—Armada produced no revenues but reported a net loss of $603,760 driven primarily by general administrative expenses incurred during corporate maintenance activities [S2][F1].

Its balance sheet shows current assets totaling roughly $445 thousand dwarfed by current liabilities exceeding $4.25 million, resulting in an extremely low current ratio around 0.1 [F1]. Such figures reflect obligations unrelated to operating debt but possibly accrued costs such as management fees or deferred underwriting obligations pending completion of business combination.

This stark liquidity imbalance highlights the reality that while investor capital remains protected within the trust account separately from these liabilities, the operating entity itself holds minimal working capital—an expected but critical nuance for shareholders assessing short-term solvency independent from trust protections.

Governance and Sponsor Incentives: Who's Steering the Ship?

Armada maintains principal executive offices in Miami, Florida—the cost of which is borne directly by its sponsor without reimbursement [S1]. This arrangement signals aligned interests insofar as sponsors invest their own resources ahead of generating returns from any prospective transactions.

To date, no equity-based incentive plans have been adopted for officers or directors, reflecting an early-stage governance posture typical among newly formed SPACs awaiting definitive mergers [S1]. Such conditions may foster streamlined decision-making but simultaneously raise questions about long-term incentive alignment pending completion of the initial business combination.

Risk Landscape: Countdown to the Business Combination Deadline

A defining risk faced by Armada is its finite window to complete an initial business combination as mandated by its IPO terms—failure necessitates liquidation wherein all funds held in trust are returned to public shareholders and the entity ceases operation [S1].

This binary outcome creates acute time sensitivity impacting strategic outreach efforts and heightens uncertainty given no targeted sectors or candidate companies have yet been disclosed publicly.

Moreover, although non-disclosure until later deal stages is consistent with SPAC market norms, this veil inherently complicates investor evaluations who must rely primarily on sponsor credibility and potential pipeline rather than tangible portfolio assets at this juncture.

The Elusive Moat: Dependency on Unknown Future Acquisitions

Currently devoid of any operational business lines or intellectual property assets, Armada’s intrinsic value proposition rests entirely on successfully consummating a merger with an unidentified company that ideally possesses sustainable competitive advantages [Valye excerpt].

Until such transaction closes, Armada lacks any definable moat or leverageable differentiation; post-combination prospects hinge on how effectively the acquired entity can capitalize on market opportunities relative to competitors. This dynamic underscores that Armada’s fate and competitive positioning are inseparably linked to unknown future partners.

Market Positioning and Investor Sentiment in the Nasdaq Listings

Since IPO launch symbols ACCIU (units), AACI (Class A shares), and AACIW (warrants) have transitioned effective October 30, 2025 to XRPNU (units), XRPN (Class A common shares), and XRPNW (warrants), marking administrative progressions toward eventual de-SPAC status [S1].

Notably, shareholdings exhibit pronounced concentration with only one holder recorded respectively for Class A and Class B shares as of December 1, 2025 [S1]. Such narrow ownership profiles frequently translate into limited trading liquidity and elevated volatility potential when market interest intensifies around merger announcements.

Investor participation so far appears minimal outside insiders or affiliated parties which may influence aftermarket behavior leading up to any transaction confirmation.

Outlook: What to Watch as Armada Approaches Its Defining Move

Looking ahead, critical milestones include finalizing definitive agreements detailing terms of the eventual business combination alongside requisite shareholder approvals and regulatory clearances [Valye excerpt][S2]. Timelines imposed under SPAC charters pressure management teams toward accelerated deal execution or risk liquidation scenarios.

Despite non-disclosure of candidate industry sectors or targets thus far, monitoring Armada’s communications for clues on strategic focus areas is essential given prevailing macroeconomic and sector-specific trends that might dictate acquisition appetites.

Execution success will profoundly influence post-merger valuation prospects along with governance transformations needed to transition from blank check status toward operational sustainability.

This analysis relies exclusively on publicly available regulatory filings as of February 2026 without extrapolation beyond documented disclosures. It aims to contextualize Armada Acquisition Corp. II’s position within evolving SPAC market dynamics without offering investment advice or predictive judgments about future performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments