Zoom Communications Accelerates AI-Driven Growth with Strong Operating Leverage Despite Macroeconomic Pressure

Zoom reported 4.4% revenue growth in FY2026, boosted by enterprise expansion and AI integration, while operating income surged 38%.

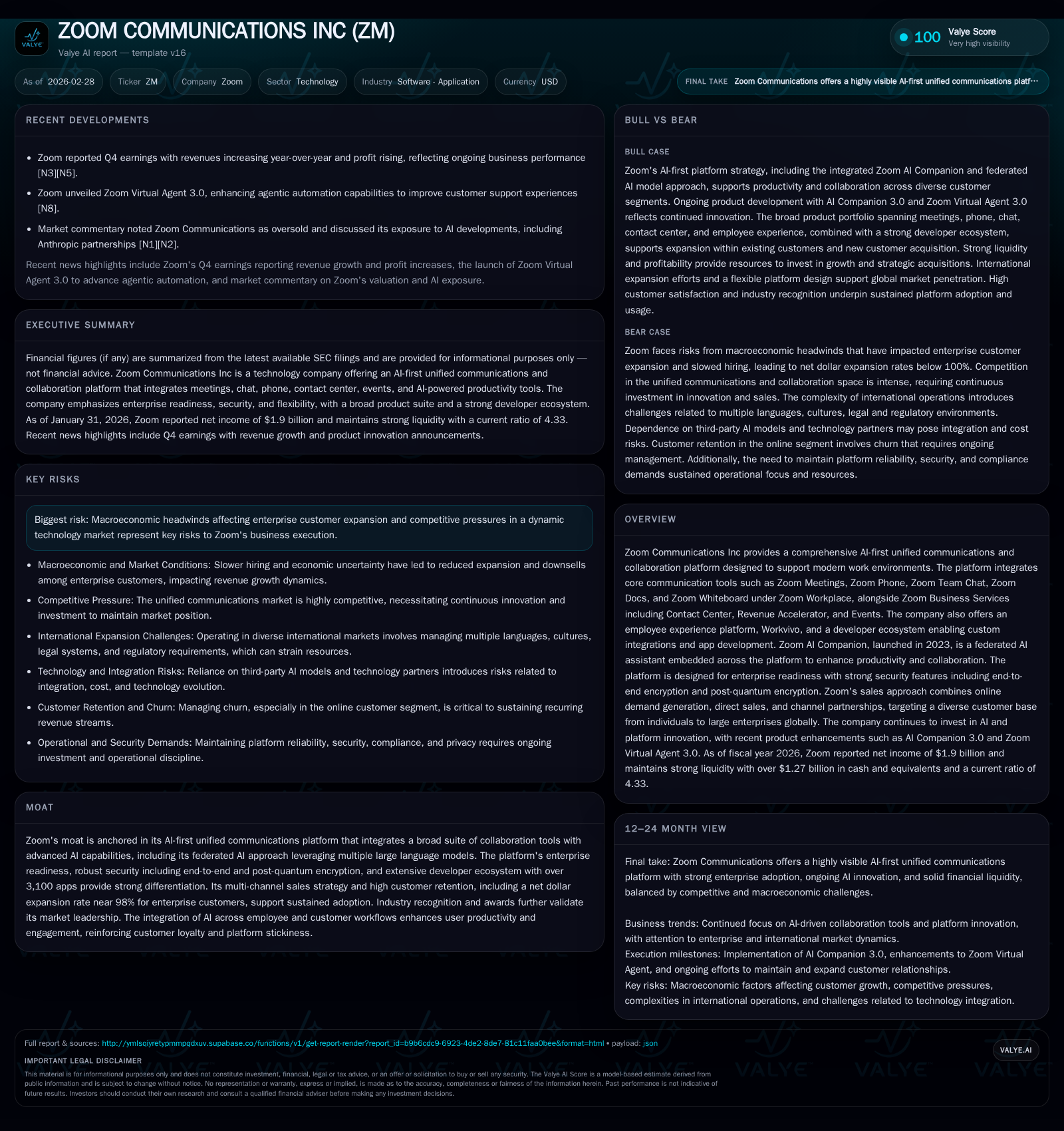

In fiscal year 2026, Zoom Communications Inc continued its transformation into an AI-first unified communications platform, growing revenue by 4.4% driven mainly by expansion within existing enterprise customers and introduction of advanced AI features like Zoom AI Companion. Robust operating margin expansion supported a sharp 88% rise in net income and strong free cash flow generation. While macroeconomic headwinds have tempered customer seat growth, Zoom’s strategic investments in AI innovation, platform broadening via Zoom Workplace, Business Services, and developer ecosystem underpin longer-term growth opportunities. The company maintains a solid liquidity position and an active share repurchase program reflecting disciplined capital allocation. Key risks remain in the form of competitive market dynamics and ongoing regulatory scrutiny.

Historical Performance Overview

Zoom Communications has evolved from its core video conferencing roots into a comprehensive AI-first unified communications platform encompassing Zoom Workplace (Meetings, Phone, Team Chat, Docs, Whiteboard) and Zoom Business Services (Contact Center, Revenue Accelerator, Events), complemented by Workvivo for employee experience and an extensive developer ecosystem.

Over the past four fiscal years leading to January 31, 2026, the company posted steady revenue growth despite economic challenges:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 1900 | 1989 | 1124 | 65 | +88.1% |

| 2025 | 1010 | 1945 | 813 | 137 | +58.5% |

| 2024 | 637 | 1599 | 525 | 127 | +514.7% |

| 2023 | 104 | 1290 | 245 | 104 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 1621 | 1924 | 19.4 |

| 2025 | 1094 | 1809 | 11.3 |

| 2024 | 0 | 1472 | 7.9 |

| 2023 | 1000 | 1186 | 1.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue series for FY23/24 not explicitly provided; growth implied from earnings progression.

The latest fiscal year saw a broad-based push in enterprise subscription services which increased 6.5%, helping elevate total revenues by $203 million or 4.4% year over year [F1][S1]. Large enterprise customers contributing over $100K annually accounted for approximately 33% of revenue as of January 31, 2026, up from roughly 29% three years prior, evidencing deepening penetration into large organizations [S1][S19]. The enterprise net dollar expansion rate has been slightly below one hundred percent due to macroeconomic impacts but remains a critical focus area backed by product innovation including AI capabilities [S1][S14].

Cost efficiencies also played a role: gross margin improved to 77% versus prior-year levels driven largely by decreased stock-based compensation expenses—a significant factor across all operating expense categories [S15][S16][F1]. These savings partially offset ongoing investments in research & development focused on AI-platform advancements.

Future Growth Prospects

Zoom positions itself as an "AI-first" work platform aiming to transform collaboration workflows with seamless integration of AI-powered tools across internal communication and customer engagement scenarios [S9][S17]. Launched in September 2023, the Zoom AI Companion uses a federated approach combining proprietary SLMs/LLMs with third-party models to deliver intelligent assistance like meeting summarization, task automation, contextual catch-up features in video meetings, chat summarization, real-time call assistance on Zoom Phone, and intelligent virtual agents within Contact Center products [S21][S26].

This AI-driven differentiation is expected to enable both land-and-expand within existing enterprise accounts as well as new customer acquisition by offering enhanced productivity benefits that are difficult to replicate by competitors [N8][S9]. Additionally, the expanding developer ecosystem—with more than 3,100 apps—supports integrations that embed Zoom deeper into customers’ workflows [S17][S26].

Geographically, while the Americas remain the dominant revenue base (~72%), international markets (APAC & EMEA) contribute close to 28%, signifying meaningful global demand coupled with localized sales efforts through strategic partners [S24][S19]. Continued international expansion is viewed as a multi-year opportunity.

Strategic acquisitions such as BrightHire are pursued selectively to augment recruiting capabilities within the employee experience vertical (Workvivo), complementing organic product development [S24].

However, macroeconomic headwinds—especially slower hiring trends affecting seat growth—and pricing pressures remain key constraints on monthly recurring revenue scalability alongside intensifying market competition from established unified communication players [S1][S14][N7]. Ongoing regulatory investigations related to privacy and data security present potential risks though recent SEC inquiries concluded without enforcement action [S11][S25].

Forecasts and Milestones

While explicit formal guidance was not detailed in recent filings or earnings news releases [N1][N3], management emphasizes focusing on:

- Growing large enterprise customers who contribute more than $100K in trailing revenue.

- Expanding product adoption breadth within existing accounts through AI-enabled feature rollouts.

- Advancing platform innovations showcased at annual user conferences such as Zoomtopia.

- Supporting international market penetration via direct sales and channel partnerships.

- Maintaining platform reliability and security standards appropriate for enterprise adoption.

Investors should monitor updates on net dollar expansion rates among enterprises post-macroeconomic recovery phases and any progress on newly deployed AI features or acquisitions that may materially impact growth trajectories [N4][N6].

Returns and Capital Allocation

Zoom demonstrates high-quality profitability metrics supported by improved margins and strong cash flow dynamics:

| FY | CFO ($B) | Capex ($M) | FCF ($B) | Buybacks ($B) | Current Ratio |

|---|---|---|---|---|---|

| 2023 | 1.29 | 104 | ~1.19 | 1.00 | - |

| 2024 | 1.60 | 127 | ~1.47 | - | - |

| 2025 | 1.95 | 137 | ~1.81 | 1.09 | - |

| 2026 | 1.99 | 65 | ~1.92 | 1.62 | >4 (4.33)[F1] |

Free cash flow approximates operating cash flow minus capital expenditures; FY26 capex declined by over half compared to FY25 primarily due to lower infrastructure spend [F1][S28]. This FCF strength underpins aggressive share repurchases totaling $1.62 billion executed during FY26 with an additional $1 billion authorization remaining as of January end [S23][F1]. Dividend payments were not specified.

Return on equity expanded robustly to approximately 19.4%, fueled by near doubling of net income against steadily growing shareholders' equity [F1]. The balance sheet remains conservatively structured with ample liquidity ($1.27 billion cash & equivalents) covering short-term obligations more than fourfold—the current ratio stands at a healthy ~4.33x [F1][S18].

Sector Contextual Analysis

Zoom operates in a highly competitive Unified Communications as a Service (UCaaS) market where differentiation increasingly hinges on platform extensibility via APIs/SDKs plus embedded intelligence layers powered by generative AI models—an area where Zoom’s federated strategy offers potential cost-efficient performance benefits vs pure proprietary or single-UML providers.

Security remains paramount given heightened organizational standards; Zoom’s deployment of end-to-end encryption combined with emerging post-quantum cryptographic methods sets it apart relative to many peers still navigating early quantum readiness . Adoption trends now skew toward holistic platforms integrating video conferencing with cloud-based telephony, event hosting scalable into millions of viewers, contact center automation with virtual agents—all supported by seamless data governance frameworks favoring platforms demonstrating credible compliance frameworks.

To sustain competitive advantages amid cyclical IT budget environments influenced by macroeconomics requires continuous innovation aligned closely with evolving customer workflows—as reflected by Zoom's investment priorities highlighted above.

Risks Summary

Key risks identified include:

- Persistent macroeconomic pressures constraining seat count growth among larger enterprises causing sub-100% net dollar expansion rates recently [S14][S19].

- Intensified competition from entrenched tech giants expanding their UC offerings bundled within broader productivity suites.

- Regulatory investigations related to privacy/data security could result in penalties or distraction though some inquiries have resolved favorably so far [S11][S25].

- High reliance on continued investment in technology innovation and talent retention needed to maintain forward momentum amid rapid market evolution [S2][S17].

Monitoring these factors alongside execution on product roadmap milestones will be critical going forward.

This analysis is based solely on publicly available information including SEC filings up to February 27, 2026 ([F1],[S#]) and recent news reports ([N#]). It aims to provide institutional-quality insights without making any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments