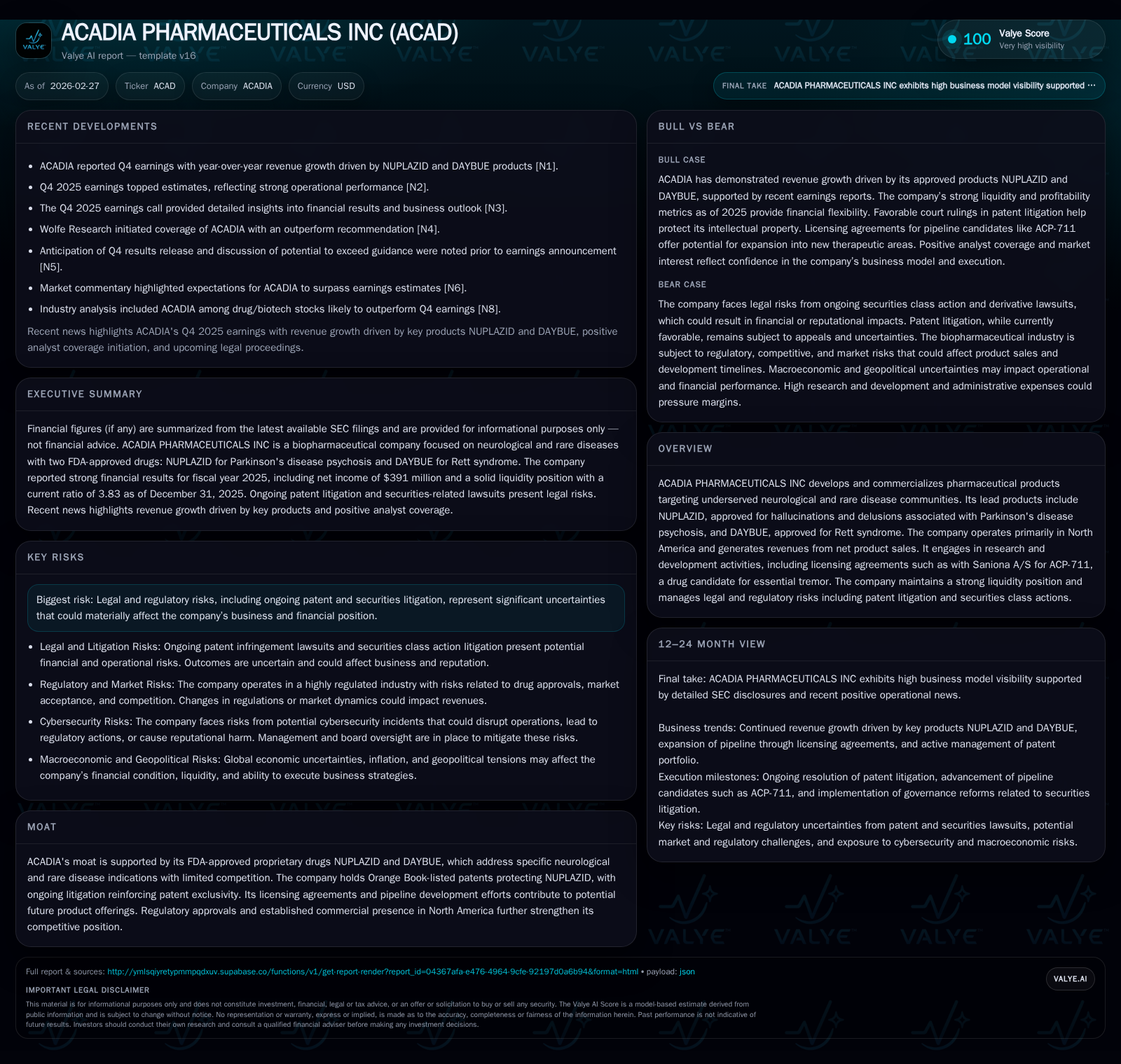

ACADIA PHARMACEUTICALS Solidifies Neurological Franchise with Nuplazid and Daybue Amid Patent Litigation

ACADIA reported strong operational cash flow and net income growth in 2025, driven by its lead neurological drugs, while ongoing patent disputes present material risk.

ACADIA Pharmaceuticals has strengthened its position in the niche neurological pharmaceutical space through its FDA-approved products Nuplazid and Daybue, which address Parkinson’s disease psychosis and Rett syndrome respectively. After years of volatile financial performance affected by patent litigation and development setbacks, 2025 marked a return to profitability with operating income reaching $105 million and net income surging to $391 million [F1]. The company also boasts a robust liquidity profile with a current ratio above 3.8, supporting continued R&D investment and commercial expansion. However, patent infringement lawsuits against generic manufacturers remain unresolved, including upcoming trials that could affect exclusivity duration [S4][S5]. Future growth hinges on pipeline advancement such as ACP-711 for essential tremor under a licensed partnership with Saniona. Watch for updates on clinical milestones and regulatory approvals to assess trajectory [N1][N3][S28][S11].

Historical Performance

ACADIA Pharmaceuticals has experienced a financial roller-coaster over recent years, reflective of the challenges inherent in neuropharmaceutical commercialization amidst patent defense pressures. Revenue rose substantially from $136 million in 2022 to $231 million by 2023, driven by increased traction for its flagship drug Nuplazid, approved for hallucinations and delusions associated with Parkinson's disease psychosis, as well as early contributions from Daybue for Rett syndrome [F1].[N1] However, historical volatility is notable — revenues had previously peaked at approximately $442 million in 2020 before declining during market adjustments and competitive pressures.

Operating income followed a pattern of recovery: from steep losses of over $223 million in 2022 fading to negative $73 million in 2023, ACADIA turned profitable by fiscal year-end 2025 at roughly $105 million—a marked improvement reflecting scaling sales efficiencies and controlled operating expenses [F1].[N2]

This operational turnaround translated into net income growth from a modest $46 million in 2023 to a robust $391 million in 2025, showcasing effective margins expansion despite substantial ongoing R&D and legal costs. Working capital management is conservative, with current assets exceeding current liabilities by almost fourfold ($1.06 billion vs. $277 million), bolstering liquidity during litigation uncertainties [F1].[S12][S19]

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 391 | 110 | 105 | +72.7% | ||

| 2024 | 226 | 158 | 231 | +394.5% | ||

| 2023 | 231 | 46 | 17 | -73 | +69.3% | +209.8% |

| 2022 | 136 | -42 | -114 | -224 | +4.4% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 105 | 31.9 |

| 2024 | 157 | 30.9 |

| 2023 | 17 | 10.6 |

| 2022 | -114 | -10.4 |

Source: SEC companyfacts cache [F1].

Figures above sourced primarily from latest SEC filings and company disclosures [F1], unless otherwise noted.

Future Growth Prospects

The core foundation underpinning ACADIA’s future lies with two FDA-approved therapies: Nuplazid (pimavanserin) which commands a niche with limited competition due to its unique mechanism targeting Parkinson's disease psychosis symptoms; and Daybue for the orphan indication of Rett syndrome offering access into rare pediatric neurodevelopmental disorders [S1].[N1]

While commercial execution has catalyzed top-line gains, continuation depends heavily on maintaining exclusivity protections around Nuplazid’s patented formulations enforced through active litigation against several generic entrants including MSN Laboratories and Aurobindo Pharma [S5][S7][S9]. Court decisions thus far have favored ACADIA but appeals remain pending with key trials scheduled into late 2026—creating considerable uncertainty that could cap revenue upside if generic launches accelerate.

In pipeline development, ACADIA’s license agreement with Saniona A/S for ACP-711 represents a deliberate expansion into treating essential tremor—a prevalent neurological condition lacking fully satisfactory pharmacological interventions today [S13].[N3] Initial upfront payments of $28 million were expensed into R&D reflecting absence of alternative uses, with potential milestone obligations exceeding $500 million contingent on successful development progress and commercial thresholds.

Regulatory challenges persist internationally; notably a projected negative opinion from the European CHMP on Daybue’s Rett syndrome application adds complexity around geographic expansion strategies outside North America where sales currently concentrate exclusively [N12].

Forecasts and Milestones to Watch

Though explicit formal guidance was not extended for future periods in disclosed filings as of early 2026, investors should monitor several pivotal indicators extracted from both corporate communications and SEC updates:

- Outcomes of pending patent infringement appeals expected within the next year will be critical to forecast duration of revenue protection for Nuplazid.

- Clinical development progress and Phase II trial readouts relating to ACP-711 could reshape medium-term revenue trajectories if positive efficacy/safety signals emerge.

- Regulatory feedback — particularly regarding Daybue beyond U.S. markets—will influence international market access timelines.

- Legal settlements or escalations on securities class action claims premised on data disclosure issues may impact financial statements or governance transparency outlooks [S6][S10].

Close attention should be paid to quarterly earnings releases as they provide updated sales figures for core products along with commentary around litigation status and pipeline timing assumptions post each reporting period [N3].[N9]

Returns and Capital Allocation Profile

Capital allocation decisions at ACADIA lean heavily toward reinvestment in R&D as the company seeks sustained innovation fodder beyond marketed products. With reported operating cash flow standing strong at approximately $110 million in FY2025 against relatively low capital expenditures near $4.7 million, free cash flow generation is positive at over $105 million—offering capacity flexibility for strategic initiatives including milestone payments or potential acquisitions [F1].[S28]

No dividends or share repurchase programs have been documented recently; instead retained earnings are channeled toward advancing the research pipeline and defending intellectual property rights lawfully challenged by generics.

The approximate return on equity calculated using net income over average equity stands near an impressive ~32%, underscoring efficient capital employment given commercial scale achieved so far amid sector-wide risks [F1]. However, this figure reflects non-operational elements including favorable litigation outcomes influencing net results.

Litigation and Regulatory Risks Remain Material

Patent enforcement forms a core strategic battleground; ACADIA initiated lawsuits against multiple generic pharmaceutical companies since mid-2020 alleging infringement on Orange Book-listed patents associated with Nuplazid formulations [S5][S7]. Despite some settlements granting generics permission dates beyond mid-to-late-2030s, the remaining defendants’ suits proceed including scheduled Delaware District Court trials in November 2026.

Additionally, securities class action litigation alleges inadequate disclosure related primarily to statistical issues around dementia-related psychosis indications implicated in FDA submissions; these actions involve ongoing discovery stages with pretrial hearings slated throughout early-to-mid 2026 [S6][S15]. Governance reforms are underway following derivative suit settlements linked to these claims.

Cybersecurity has emerged as a key operational risk area; after onboarding a Chief Information Security Officer (CIDO) in mid-2025 with deep industry experience, ACADIA enhanced governance protocols overseen by its audit committee aiming to reduce exposure to potential data breaches that could disrupt clinical or commercial operations [S1][S8].

Industry Context Analysis

The neuropharmaceutical subsector is characterized by high barriers to entry due to stringent FDA approval pathways requiring rigorous demonstration of safety/efficacy alongside substantial patent portfolios protecting proprietary molecules—factors ACADIA leverages successfully today. Competition remains limited but innovation cycles demand continuous investment.

Furthermore, payer dynamics increasingly favor treatments demonstrating clear patient benefit especially when addressing underserved populations like Parkinson's psychosis or rare diseases such as Rett syndrome—areas aligned with ACADIA’s core focus though pricing pressure persists generally across biopharma.

Licensing deals such as that executed with Saniona typify industry practice where modular acquisition of promising assets provides pipeline diversity without overstretching internal R&D bandwidth prematurely.

Conclusion

ACADIA Pharmaceuticals stands at an inflection point balancing renewed financial strength buttressed by increased revenues and profitability against persistent legal uncertainties pertaining primarily to patent protection enforcement for its cornerstone drug Nuplazid.[F1][S4] The launch of Daybue deepens its foothold within rare neurological diseases but international regulatory headwinds temper global expansion enthusiasm.[N12] Simultaneously advancing early-stage candidates like ACP-711 via partnerships underscores intent to transition toward broader therapeutic coverage while managing capital efficiently supported by healthy free cash flow generation.[F1]

Stakeholders must closely monitor legal developments that hold the key to duration of exclusivity protections vital for preserving lucrative market positions alongside clinical trial milestones that dictate growth runway sustainability past the medium term.[N3][S7]

This report is intended solely for informational purposes based on publicly available data as of February 27, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments