Adicet Bio’s Financial Strain Reflects High-Risk Early-Stage Cell Therapy Development

Adicet Bio’s early clinical-stage allogeneic gamma delta T cell platform faces scaling and regulatory challenges amid sustained operational losses.

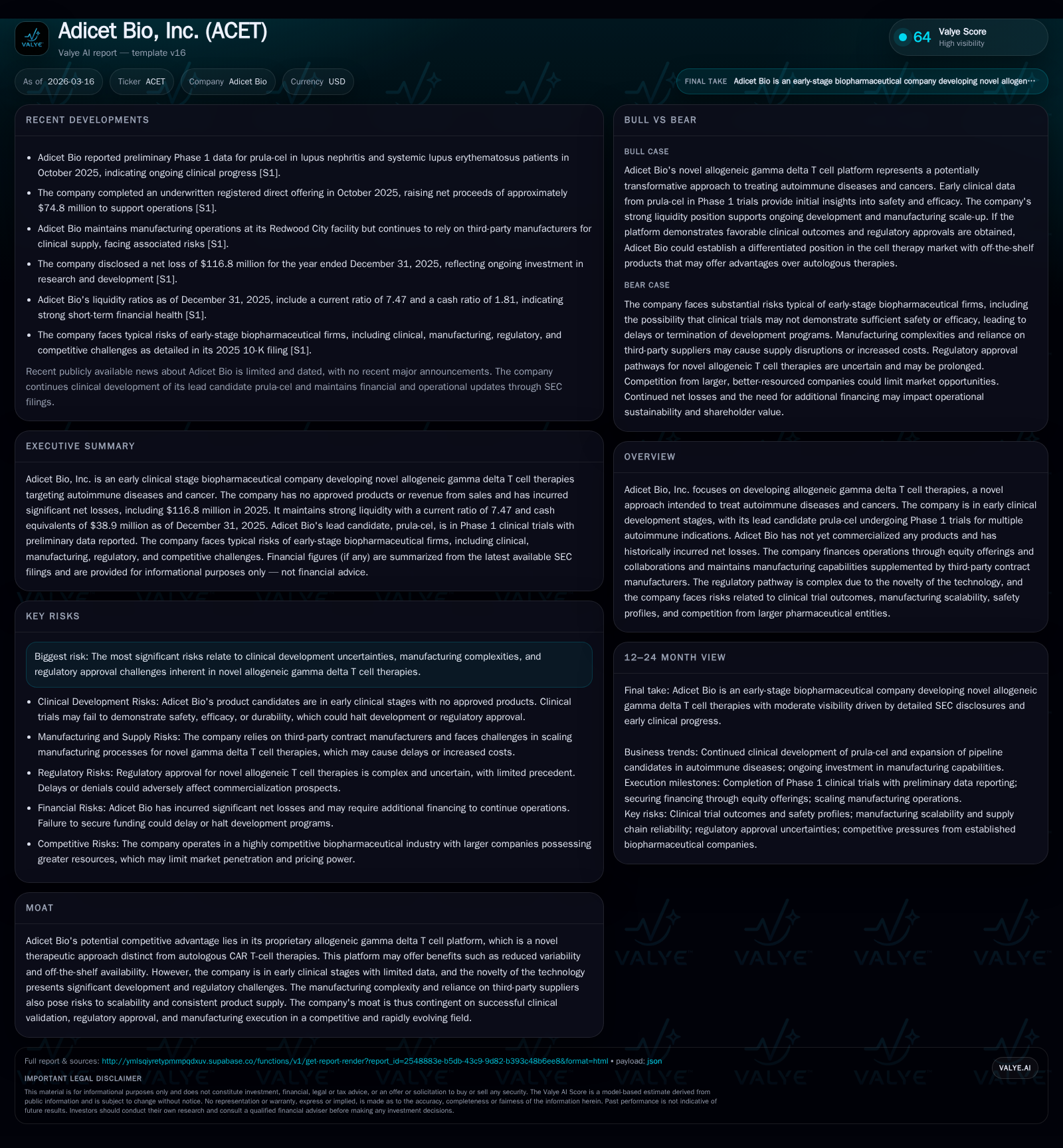

Adicet Bio operates in the nascent field of allogeneic gamma delta T cell therapies, targeting autoimmune diseases and cancers. Despite a proprietary platform with potential off-the-shelf advantages over autologous CAR T therapies, the company remains pre-commercial with no approved products or revenue. Persistent net losses exceeding $100 million annually highlight significant investment in R&D and an uncertain path to regulatory approval. Manufacturing complexities and competitive pressures from larger pharma players further constrain near-term growth prospects. Key performance metrics reveal minimal improvement in operating results, with heavy reliance on capital raises to sustain operations.

Company Overview and Technology

Adicet Bio, Inc. is pioneering an innovative approach in immunotherapy focused on allogeneic gamma delta T cell therapies for treating cancer and autoimmune diseases. Unlike autologous CAR T-cell therapies that use a patient's own cells, Adicet's platform aims to develop 'off-the-shelf' cellular treatments derived from healthy donors, potentially reducing variability and complexity related to patient-specific manufacturing.

The company's lead product candidate prula-cel is currently undergoing Phase 1 clinical trials targeting multiple autoimmune indications. Additional candidates such as ADI-212 are under early-stage development [S1]. However, the enterprise remains pre-commercial with no approved products or revenue streams.

Historical Financial Performance

Since its founding in November 2014, Adicet has consistently invested heavily in R&D as it builds out capabilities for its novel platform technology, resulting in sustained operating and net losses over multiple years without commercial income.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -117 | -95 | -122 | 2 | +0.3% |

| 2024 | -117 | -92 | -128 | 1 | +17.9% |

| 2023 | -143 | -94 | -152 | 4 | -104.4% |

| 2022 | -70 | -45 | -73 | 17 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -97 | -73.4 |

| 2024 | -93 | -62.8 |

| 2023 | -98 | -83.8 |

| 2022 | -62 | -23.9 |

Source: SEC companyfacts cache [F1].

Negative figures indicate losses or cash outflows; all figures sourced from latest SEC filings [F1]

Net income reflects deepening losses through FY2023 followed by modest stabilization in FY2024–25. Operating income exhibits a similar trend with gradual improvement but remains deeply negative.

Cash flow from operations has hovered near negative $95 million annually since FY2023 despite reductions in capital expenditures relative to FY2022 levels.

At fiscal year-end 2025, Adicet held approximately $38.9 million in cash and equivalents against current liabilities of $21.5 million — yielding a current ratio of approximately 7.47x. This suggests adequate short-term liquidity but highlights limited runway absent additional financing [F1].

Growth Prospects and Strategic Catalysts

Future expansion fundamentally hinges on successful clinical validation of Adicet’s allogeneic gamma delta T cell platform candidates. Positive safety and efficacy results for prula-cel would represent critical milestones capable of transforming the company’s trajectory.

Key potential drivers include:

- Advancement through later clinical trial phases (Phases 2/3) establishing robust efficacy data.

- Navigating regulatory approval pathways despite limited precedent for this novel therapy class [S17][S13].

- Scaling manufacturing infrastructure balancing internal capabilities with third-party contract manufacturers.

- Expanding pipeline leveraging platform versatility across oncology indications.

Growth may be constrained by:

- Uncertain clinical outcomes given the early developmental stage.

- Prolonged or complex regulatory approvals due to the novel therapeutic modality.

- Challenges ensuring reproducible large-scale manufacturing meeting cGMP quality standards.

- Competition from established pharmaceutical companies developing alternative immunotherapies.

- Pricing pressures and reimbursement uncertainties influenced by evolving healthcare reforms [S7][S15].

Regulatory Environment and Risks

The FDA's regulatory framework for cellular therapies like those pursued by Adicet remains fluid and evolving. The agency's limited prior experience with allogeneic gamma delta T cells suggests possible prolonged review periods including advisory committee consultations [S17][S13]. Post-market requirements such as Risk Evaluation and Mitigation Strategies (REMS) may impose ongoing compliance burdens.

Similar considerations apply internationally where advanced therapy medicinal product (ATMP) designations impose rigorous assessment criteria affecting market entry timing.

Failure to navigate these approvals or unexpected adverse trial results could severely disrupt timelines or commercialization feasibility.

Intellectual Property Considerations

Intellectual property protection forms a cornerstone of Adicet’s competitive position but faces inherent uncertainties characteristic of biotechnology patent landscapes [S8][S18][S26]. The company must maintain patents around proprietary constructs and manufacturing processes while defending against infringement claims that could stall development or result in costly litigation.

International patent enforcement challenges exist due to jurisdictional variations potentially allowing competitors more latitude outside the U.S., thereby diluting exclusivity benefits globally.

Capital Allocation and Financial Returns

Given its pre-revenue status and intensive R&D focus, Adicet reported a negative return on equity estimated at approximately -73.4% for FY2025 based on net loss relative to equity base [F1].

Cash flows remain firmly negative reflecting ongoing funding needs; approximate free cash flow was near -$97 million primarily driven by operating cash burns vastly exceeding minimal capital expenditures [F1].

No dividends or share repurchases have been implemented given the absence of profits.

Operations have been historically funded through equity offerings; recent capital raises include approximately $19 million via ATM sales in January 2024 plus public offerings totaling over $160 million between early 2024 and late 2025 [S1], underpinning development programs but diluting existing shareholders.

Manufacturing Capacity Challenges

Adicet maintains internal manufacturing capabilities supplemented by third-party contract manufacturers—a common model balancing cost efficiency against risks related to control over supply chain quality [S1].

Scaling production consistently while adhering to cGMP standards represents a key operational challenge; manufacturing failures or supply interruptions could delay clinical activities or commercialization adversely impacting prospects.

External Market Factors and Competitive Positioning

While Adicet’s proprietary platform offers theoretical advantages in reduced variability and ready availability versus autologous treatments, larger incumbents possess broader pipelines and established manufacturing platforms enabling greater resilience against setbacks.

Reimbursement uncertainty looms as insurers increasingly scrutinize pricing particularly for high-cost biologics requiring long-term follow-up care—pressures intensified by recent legislative initiatives addressing drug pricing growth mechanics [S7][S15].

Expanding competitive immunotherapy options—from CAR-T innovations through bispecific antibodies—further crowd the market landscape challenging differentiated uptake scenarios.

Summary Outlook: What to Watch Next (Analysis)

- Progression milestones from Phase 1 trials of prula-cel including interim safety/efficacy readouts signaling viability beyond proof-of-concept stages.

- Regulatory filings such as IND clearances for additional indications or new pipeline candidates broadening opportunity sets [S14].

- Updates on manufacturing scale capacity expansion or third-party agreements ensuring reliable supply chains necessary for commercialization readiness.

- Capital raising announcements critical given cash burn trends indicating limited runway without fresh resources into late-stage trials.

- Competitive developments including peer clinical successes/failures recalibrating investor perceptions around therapy class viability.

- Changes in healthcare policies affecting reimbursement frameworks materially influencing commercial feasibility post-launch.

Disclaimer

This report is intended solely for informational purposes reflecting publicly available data as of early 2026 and does not constitute investment advice or recommendations. Financial figures are sourced exclusively from SEC filings noted herein; no forecasts or speculative estimates have been made beyond documented guidance or company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments