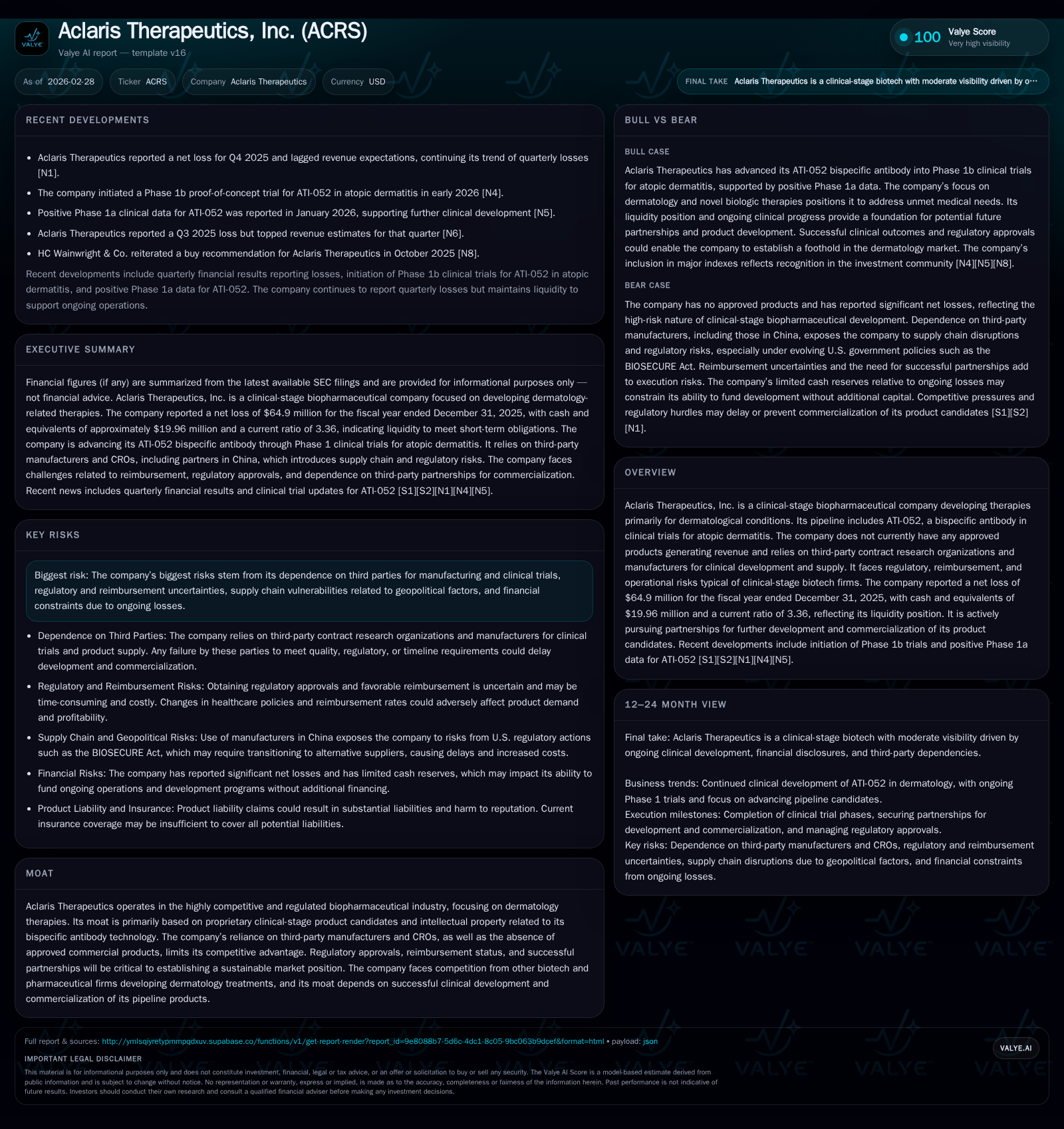

Aclaris Therapeutics’ Transition from Clinical Trials to Commercialization: Financial and Developmental Milestones in 2025

The company marked significant clinical progress in its dermatology pipeline while narrowing losses, underscoring a pivotal year balancing scientific advancement with financial discipline.

Aclaris Therapeutics, Inc. continued its evolution in 2025 with meaningful progress in clinical-stage drug development, notably advancing its ATI-052 bispecific antibody for atopic dermatitis into Phase 1b trials. Despite no product revenue, the company improved operating results, cutting its net loss nearly by half versus 2024. Operating cash flow deficits reflect ongoing investments in R&D amid modest capital expenditures. The firm’s capacity to secure reimbursement, navigate regulatory approvals, and forge strategic partnerships will critically shape its path toward commercialization. Elevated risks around third-party dependencies, regulatory compliance, and supply chain exposures remain material as Aclaris pursues clinical milestones and financial stabilization.

Fiscal 2025 Financial Performance: Gains Amid Continued Losses

Aclaris Therapeutics, Inc.'s fiscal year 2025 demonstrated meaningful financial improvement against the backdrop of its wholly clinical-stage profile. The company reported a net loss of $64.9 million for FY 2025 compared to a significantly larger loss of $132.1 million recorded in FY 2024 — an improvement of approximately 50.8% year-over-year [F1]. Operating income losses likewise contracted substantially by about 46.2%, reaching a deficit of $76.4 million in 2025 versus $141.9 million previously [F1]. This pattern reflects tighter expense management alongside continued investment in clinical development efforts, although product revenues remained nonexistent.

Notably, Aclaris has operated without any approved commercial products generating top-line revenue since its inception into clinical testing phases [S1]. This dynamic aligns with typical developmental cadence observed in biopharmaceutical firms where upfront R&D outlays precede revenue generation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -65 | -47 | -76 | 111000 | +50.8% |

| 2024 | -132 | -20 | -142 | 121000 | -49.3% |

| 2023 | -88 | -78 | -97 | 1309000 | -1.8% |

| 2022 | -87 | -68 | -90 | 605000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -47 | -63.0 |

| 2024 | -20 | -84.9 |

| 2023 | -80 | -56.3 |

| 2022 | -68 | -44.0 |

Source: SEC companyfacts cache [F1].

Drivers of Historical Operating Improvements and Cash Flow Dynamics

The contraction in operating losses signals enhanced operational efficiencies or controlled spending on supporting activities such as general administration or licensing costs [S3]. However, this improvement contrasts with a stark deterioration in net cash used by operating activities (CFO), which plunged from roughly negative $20 million in FY 2024 to over negative $47 million in FY 2025 [F1]. This divergence suggests an intensification of actual cash burn related principally to research programs and third-party contract engagements — a common pattern for companies reliant on CROs for pivotal trial conduct and CMOs for drug substance production without internal manufacturing infrastructure.

Capital expenditures remained immaterial and stable at just over $111k for FY25 compared to prior periods [F1], consistent with Aclaris’ strategy emphasizing outsourced services instead of heavy asset ownership.

Taken together these metrics underscore the dual challenge for a clinical-stage biotech: driving forward costly innovation while managing capital under continuing losses.

Pipeline Advances: Clinical Milestones and Bispecific Antibody Developments

Aclaris spotlighted substantial pipeline progress during the period as its ATI-052 bispecific antibody entered Phase 1b clinical trials targeting atopic dermatitis [N1][S1]. This represents a critical milestone demonstrating advancement beyond early safety assessments into more rigorous exploratory efficacy evaluations—helping to validate both technical feasibility and pharmacologic potential.

This trial initiation is integral to Aclaris’ value proposition predicated on proprietary molecular immunotherapies designed to address inflammatory dermatological disorders—a competitive therapeutic domain requiring compelling differentiation on efficacy endpoints such as symptom mitigation and durable disease control [S1]. Such advancements build substantive clinical candidate visibility even absent marketed drugs.

Commercialization Prospects: Regulatory Approval Pathways and Reimbursement Challenges

Looking ahead toward eventual commercialization if product candidates prove successful clinically and obtain marketing approval faces multilayered complexity [S1]. Regulatory approval pathways remain exacting—demanding comprehensive data submissions covering safety profiles verified under FDA scrutiny alongside global health authorities where distribution might occur.

Securing sufficient reimbursement emerges as another pivotal hurdle given sector-fragmented payer landscapes encompassing private insurers and government programs like Medicare/Medicaid with intricate formulary access processes [S1][S27]. Payers typically weigh cost-effectiveness relative to existing therapies alongside real-world patient outcomes data before endorsing pricing tiers permitting profitable sales.

Management articulates an active pursuit of partnership arrangements aimed at co-development or commercial distribution support—though acknowledges the competitive landscape among biotech vendors striving for suitable collaborators possessing requisite regulatory expertise and sales networks [S21]. Such alliances help offset resource burdens mitigating sole commercialization risks.

Financial Health and Capital Allocation Priorities

Despite persistent losses reflected through a negative net income position (-$64.9 million) against equity standing near $103 million at end-2025 [F1], Aclaris displayed prudent liquidity management with cash and equivalents totaling approximately $19.96 million entering the new fiscal year along with a current ratio healthy at about 3.36 [F1].

Return on equity remains deeply negative around -63%, illustrating eroding shareholder value typical among pre-revenue biopharmaceutical developers absorbing R&D-heavy investments without commercial inflows yet [F1]. No dividends or share repurchases occurred consistent with corporate priorities concentrating available funds on advancing pipeline assets rather than capital returns [S3].

Capital allocation clearly skewed toward funding costly trial expenditures plus external research partnerships rather than infrastructure expansion—characteristic of outsourced clinical models limiting fixed capital deployment.

Key Risks: Third-Party Dependencies and Regulatory Compliance Complexity

Aclaris confronts a spectrum of material risks primarily centered around reliance on third-party contract research organizations (CROs) responsible for key components of trial execution alongside contract manufacturing organizations (CMOs) handling drug substance production [S4][S6]. This layered vendor dependency exposes the company to potential disruptions linked to counterparty performance or geopolitical issues affecting supply chains.

Regulatory risks span not only marketing approval challenges but also ongoing compliance obligations including rigorous pharmacovigilance reporting post-launch plus cybersecurity risk governance overseen directly by CFO-level management as disclosed within internal controls frameworks [S1][S14]. These aspects reinforce complex operational risk layers that could adversely impact timelines or invoke penalties if not tightly managed.

Furthermore,Aclaris operates under evolving legal regimes targeting pharmaceutical fraud prevention (anti-kickback statutes), data privacy safeguards across jurisdictions—including HIPAA compliance—and emerging AI governance mandates potentially complicating technological applications within drug discovery or patient data handling [S12][S13].

Monitoring Points: Upcoming Data Readouts and Cash Runway Assessment

Market attention should center on imminent clinical data readouts expected from Phase 1b ATI-052 studies serving as crucial inflection points validating therapeutic hypotheses potentially unlocking further developmental investment or partnership uptake [N1][S3]. Meanwhile liquidity trends necessitate vigilance given ongoing operating cash flow deficits that may require supplementary financing measures absent near-term revenue generation [F1][S3].

Additional catalytic developments would include formal announcement of strategic partnerships furnishing collaborative resources essential to scaling late-stage trials or commercialization preparations—events likely influencing perceptions regarding valuation inflection prospects.

This report synthesizes publicly available SEC filings and company disclosures up to February 28th, 2026 to provide an integrated view focused on operational execution patterns and industry-specific considerations shaping Aclaris Therapeutics' trajectory as a developing dermatology-centric biopharma entity. It avoids speculative forecasts or valuation judgements while emphasizing measurable financial and developmental milestones relevant to analyst diligence processes within biopharma investment contexts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments