Agree Realty Corp: Navigating Dividend Stability and Insider Confidence Amid Real Estate Sector Challenges

Agree Realty Corp balances a resilient dividend profile with strategic insider buying as it confronts sector cyclicality and macroeconomic pressures.

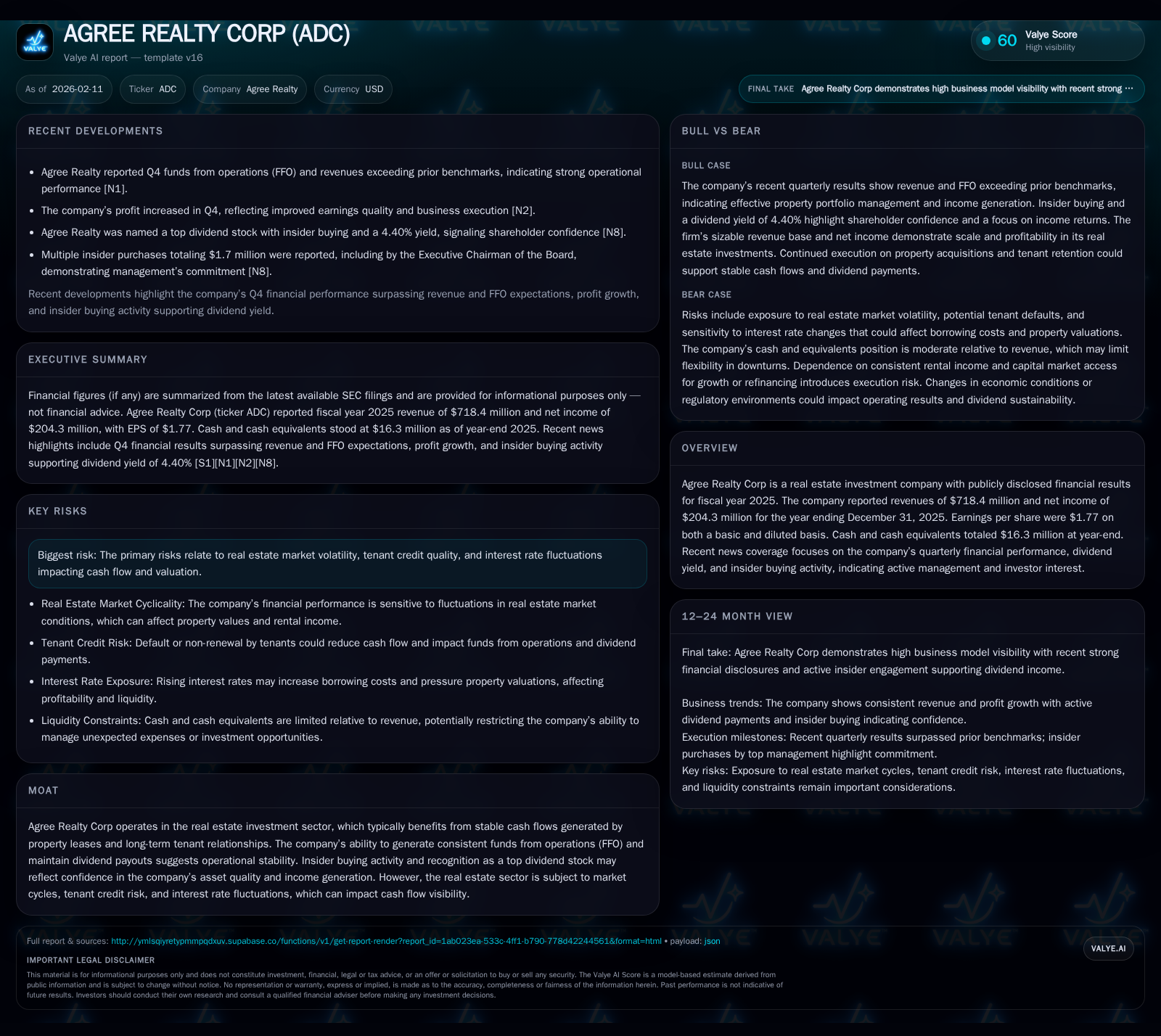

Agree Realty Corp (ADC) stands out as a dividend-focused real estate investment trust with $718 million revenue and $204 million net income reported for fiscal 2025. The company's consistent earnings and 4.4% dividend yield have attracted notable insider buying, signaling confidence from its leadership. However, underlying real estate market cyclicality, tenant credit risk, and interest rate volatility present ongoing challenges that require prudent management tactics to preserve dividend sustainability and growth prospects.

A Dividend Darling in a Cyclical Sector: Agree Realty's Income Appeal

Agree Realty Corp has carved out a distinct niche as a reliable dividend payer in the often-volatile real estate investment trust (REIT) universe. Its reputation as a top dividend stock has been bolstered recently by reports emphasizing a 4.40% yield coupled with significant insider buying activities. According to Nasdaq coverage from early 2026, investors eye ADC not only for its payout consistency but also for the clear signal insiders send by increasing their stakes during uncertain market conditions [N10]. This dual dynamic—stable income backed by management conviction—engages income-focused investors seeking resilient sources of cash flow.

This allure is noteworthy in an asset class traditionally susceptible to economic cycles, where rental income can be pressured by tenant defaults or vacancies. Agree Realty’s operational model leans heavily on long-term tenant leases across retail properties, underpinning predictable funds from operations (FFO), which are critical for sustaining dividends. The balance here is between rewarding shareholders regularly while managing the inherent risks of leasing commercial real estate.

Parsing the Numbers: 2025 Financial Snapshot and Trends

The company’s financial results for fiscal year 2025 affirm its operating stability amidst a complex macro environment. Agree Realty posted revenues of approximately $718.4 million alongside net income north of $204 million for the year ended December 31, 2025 [F1]. These figures translate into earnings per share of $1.77 on both basic and diluted bases—a metric that informs on profitability available to common shareholders.

Quarterly updates reveal that ADC has been able to outperform analyst expectations in key areas such as Q4 funds from operations (FFO) and revenues [N3]. Such performance is complemented by liquidity evidenced in $16.3 million of cash and equivalents at year-end [F1], providing operational flexibility amid potential market shifts.

Moreover, recent profit climbs observed in quarterly reports reflect controlled cost structures alongside healthy lease renewals or expansions [N4]. These trends underpin a narrative of disciplined growth rather than speculative asset accumulation.

Insider Confidence: Decoding Significant Insider Purchases

A particularly compelling angle on ADC’s outlook is derived from the scale and timing of insider buying activity. In January 2026 alone, board members committed roughly $1.7 million towards stock acquisitions—a move highlighted as exceptional in industry reporting [N11]. This buying spree included purchases by the Executive Chairman of the Board himself [N13], signaling top-tier leadership endorsement of the company’s valuation and future trajectory.

Insider transactions of this magnitude amidst sector uncertainty serve as implicit endorsements often overlooked by a wider investor base sifting through headline volatility [N12]. They suggest that management’s assessment of current share price undervaluation or long-term company fundamentals remains optimistic.

This form of endorsement complements other positive operational signals while providing a layer of reassurance on governance integrity concerning capital deployment decisions.

Real Estate Moat Analysis: Operating Strengths and Structural Risks

Agree Realty’s moat lies squarely in its ability to generate consistent lease-based revenue streams supported by long-duration contracts with solid tenants. Such agreements foster predictability in funds from operations—a non-GAAP measure closely watched within REIT circles given its representation of recurring earnings excluding depreciation or one-off items.

The company benefits from diversification across multiple retail properties geographically spread to mitigate localized economic impacts [valye_report_excerpt]. Additionally, tenant longevity tends to reduce credit risk exposure although it cannot eliminate it entirely; tenant financial stress or bankruptcy presents downside risks impacting rent receipts and thus cash flows.

Further sector-wide vulnerabilities include sensitivity to market cycles affecting property valuations plus fluctuations in borrowing costs due to interest rate shifts—which bear directly on debt servicing capabilities [S1]. Notably, Agree Realty’s operating segment structure centers on leased retail sites with current compliance metrics reflecting healthy occupancy rates albeit subject to periodic renegotiations or turnover.

Dividend Sustainability Amid Interest Rate Challenges

The strategic imperative for ADC revolves around maintaining dividend reliability despite headwinds presented by rising interest rates that elevate borrowing expenses and pressure asset prices. The company demonstrates awareness by managing payout ratios prudently relative to its FFO generation capacity.

Recent news notes ex-dividend reminders alongside discussions around payout adjustments aligned with cash flow realities [N7]. This cautious yet steady approach caters well to investors prioritizing yield yet wary of distribution cuts common in cyclical downturns.

Interest rate sensitivity also links back to the corporation’s debt profile; floating-rate obligations or refinancing needs could amplify cost burdens if rates continue ascending [valye_report_excerpt]. Therefore, Dividend sustainability underscores not just profitability but also effective capital allocation planning amid evolving financial conditions.

Competitive Landscape: Positioning Against Peers like Realty Income and Phillips Edison

Contextualizing Agree Realty within its peer group reveals nuanced distinctions impacting investor perceptions. Realty Income (ticker: O), often held up as the quintessential monthly dividend REIT, enjoyed share gains recently driven by strong portfolio growth reports [N6], suggesting aggressive expansion strategies.

Phillips Edison & Company (PECO) matched Q4 FFO estimates mirroring sector-wide steadiness but without standout surprises [N5]. Compared against these peers, ADC maintains comparably competitive dividend yields while exhibiting slightly more conservative growth pacing—potentially appealing to risk-conscious investors valuing steadiness over accelerated expansion [N8].

Operational metrics such as occupancy rates, tenant credit quality assessments, and lease term lengths further differentiate player profiles though aggregate stability remains a shared quality among these blue-chip REITs.

Strategic Forward Outlook: Management’s Tactical Moves and Market Positioning

Looking ahead, management signals through recent operational results and insider buys suggest ongoing tactical prudence focused on capital discipline rather than rapid acquisition sprees [N3]. The deliberate stance favors sustainable earnings growth anchored in high-quality assets assuring predictable rents over opportunistic portfolio inflation.

Capital allocation decisions appear designed to weather macro uncertainties while maintaining sufficient liquidity buffers evident at year-end balances [F1]. By aligning executive incentives with shareholder interests—demonstrated via personal stock investments—management projects confidence which may forestall speculative market concerns regarding governance or strategic direction.

Such resilience is critical as sector headwinds persist on inflationary pressures affecting operating expenses alongside external influences like regulatory changes impacting real estate taxation or zoning.

Risk Assessment: Market Cyclicality, Tenant Credit Risks, and Capital Structure

Assessing Agree Realty's risks requires attention to long-standing commercial real estate vulnerabilities coupled with contemporary financial complexities documented in SEC filings [S1],[S2]. Market cyclicality poses pronounced threats whereby economic slowdowns diminish consumer spending impacting retail tenants’ ability to meet lease obligations.

Tenant credit risk remains elevated due to potential bankruptcies or rent renegotiations adversely affecting cash inflows vital for distributions. While diversification mitigates some concentration exposure, no portfolio is immune wholly from systemic shocks.

Interest rate fluctuations complicate debt management strategies; ADC holds unsecured long-term loans tied partially to variable benchmarks such as SOFR (Secured Overnight Financing Rate) increasing exposure if interest rates rise unexpectedly beyond forecasts [S2]. Leverage levels are carefully disclosed but represent ongoing sensitivities influencing corporate flexibility under stress scenarios.

Capital structure robustness including liquidity reserves acts as an important buffer against downside scenarios but continuous vigilance is necessary given inherent sector volatility.

Valuation Insights: Balancing Yield Against Market Expectations

From a valuation standpoint, Agree Realty occupies an intriguing position balancing stable dividend payouts with latent risks imbedded in commercial real estate markets during rising rate environments. While its approximately 4.40% dividend yield remains attractive versus broader fixed-income alternatives, investors must weigh this against potential fluctuations in property values and funding costs that could compress future distributable earnings.

Recent quarters’ earnings beats affirm quality yet caution tempers exuberance given lingering macroeconomic uncertainties including inflationary trends impacting tenant viability plus geopolitical tensions influencing broader business sentiment [valye_report_excerpt],[N3]. Thus ADC's valuation appears reflective of both its durable income stream merits alongside disciplined growth strategy tempered by experienced recognition of sectoral cyclicality effects.

In synthesis, Agree Realty stands as a solid candidate within the income-generating REIT space characterized by thoughtful management guided by insider conviction; however it remains prudent for stakeholders to continually monitor evolving risk factors accompanying cyclical industries reliant on external economic variables beyond direct control.

This analysis is intended solely for informational purposes without any recommendation regarding securities buying or selling.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments