Adaptive Biotechnologies Advances Immune Medicine Diagnostics Amid Continued Losses and Regulatory Challenges

Adaptive Biotechnologies leverages its adaptive immune system platform and clonoSEQ assay to innovate diagnostics while managing ongoing financial losses and complex regulatory environments.

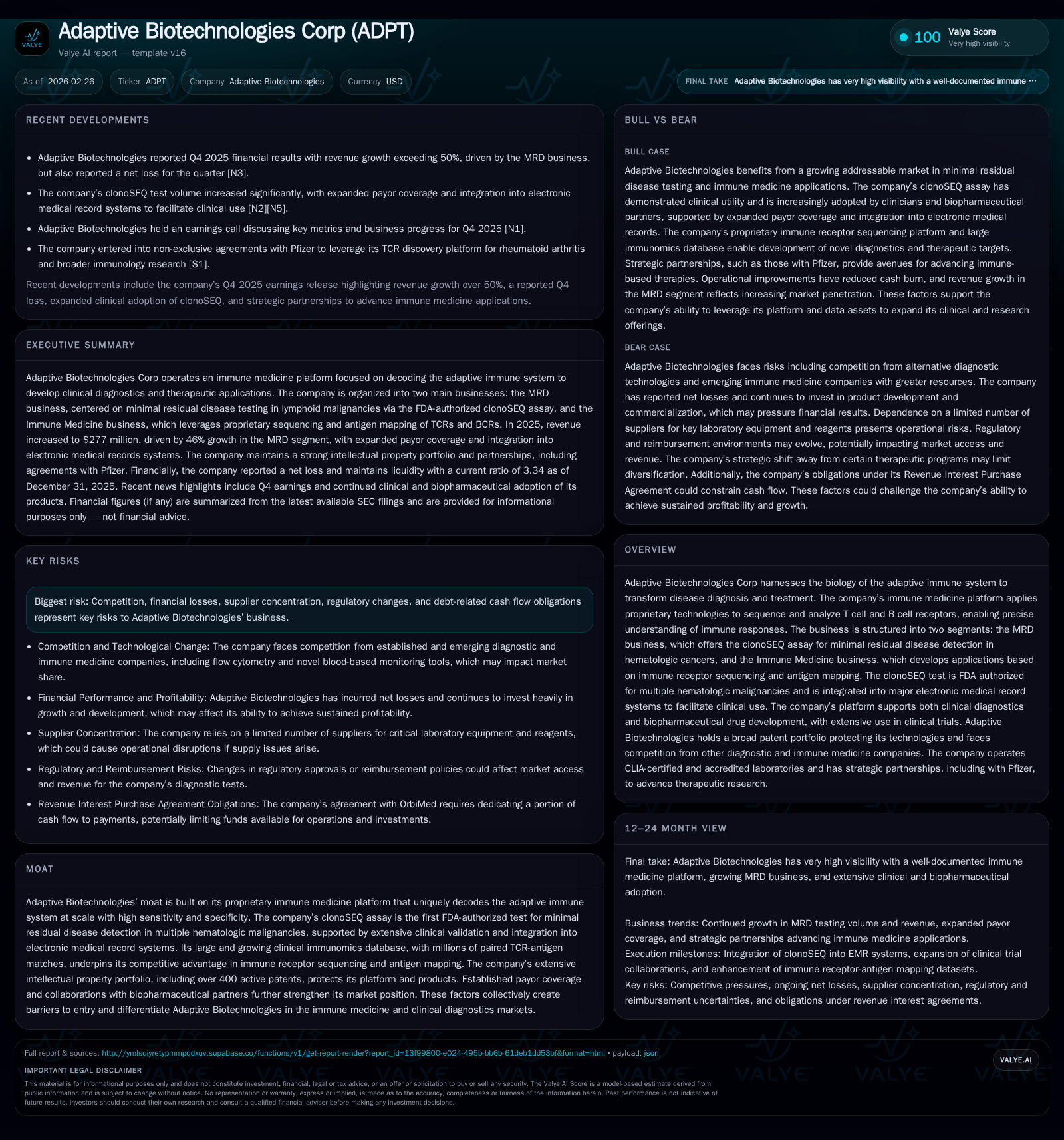

Adaptive Biotechnologies Corp develops diagnostic and therapeutic products based on decoding the adaptive immune system, with its FDA-authorized clonoSEQ assay central to minimal residual disease (MRD) detection in hematologic cancers. The company reported a net loss of $59.5 million in 2025, an improvement from prior years, supported by better operating efficiencies though cash flow remains negative. Growth opportunities are driven by expanding clinical adoption of MRD testing and Immune Medicine applications, while risks include reimbursement uncertainties, regulatory compliance, and intellectual property challenges. Monitoring revenue trends and reimbursement developments will be key to evaluating progress.

Company Overview

Adaptive Biotechnologies Corp is a pioneer in immune medicine that applies next-generation sequencing technologies to decode the adaptive immune system’s genetic code. Its flagship product, the clonoSEQ assay, is FDA-authorized for detecting minimal residual disease (MRD) in hematologic malignancies including multiple myeloma, chronic lymphocytic leukemia, and B-cell acute lymphoblastic leukemia. Beyond clinical diagnostics, the company's Immune Medicine segment leverages a proprietary immunomics database containing millions of paired T-cell receptor (TCR) antigen matches to develop novel diagnostic insights and therapeutic targets.

Historical Financial Performance

Adaptive Biotechnologies has historically reported significant net losses driven by substantial investments in research, development, and commercial expansion. For fiscal year 2025, the company recorded a net loss of $59.5 million, marking a notable improvement from the $159.5 million loss reported in 2024—a roughly 62.7% year-over-year reduction indicative of improved operational efficiency [F1]. Operating income followed a similar trend with a loss of $57.1 million in 2025 compared to $162.5 million in the prior year.

Operating cash flow improved but remained negative at $45.9 million for FY2025 versus negative $95.2 million in FY2024. Capital expenditures declined nearly 20% year-over-year to just under $3 million as management prioritized optimizing existing infrastructure over expansion [F1]. The company maintains solid liquidity with a current ratio of approximately 3.34 at year-end 2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -59 | -46 | -57 | 3 | +62.7% |

| 2024 | -159 | -95 | -163 | 4 | +29.2% |

| 2023 | -225 | -156 | -227 | 11 | -12.5% |

| 2022 | -200 | -184 | -200 | 16 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -49 | -27.2 |

| 2024 | -99 | -78.7 |

| 2023 | -167 | -73.0 |

| 2022 | -200 | -43.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not disclosed; YoY changes reflect available data.

Business Segments

Adaptive operates two principal business segments:

MRD Business: Focused on the clonoSEQ assay used for sensitive detection of minimal residual disease post-treatment across multiple hematologic cancers. The addressable market for this segment is estimated around $6.2 billion globally with approximately $5.3 billion attributable to clinical testing alone.

Immune Medicine (IM): Utilizes large-scale sequencing data combined with machine learning models linking TCRs to antigens to create novel diagnostic tools and therapeutic targets primarily focused on immuno-oncology and autoimmune disorders.

Growth Prospects

The company's growth strategy centers on expanding clinical adoption of clonoSEQ as physicians increasingly use MRD monitoring to guide personalized treatment decisions. Additionally, Adaptive seeks to broaden indications for clonoSEQ alongside launching new products within its Immune Medicine segment.

Its competitive advantage is supported by more than 400 active patents protecting its proprietary sequencing technologies and algorithms as well as an extensive immunomics database comprising millions of TCR-antigen pairs—providing valuable insights for diagnostics refinement and biopharmaceutical collaborations.

Challenges include reimbursement delays affecting test utilization rates; ongoing requirements for clinical validation; evolving regulatory landscapes impacting Medicare coverage; and competitive pressures from emerging diagnostic technologies [N1][N2].

Regulatory Environment & Risks

Adaptive operates under rigorous FDA oversight governing its diagnostic tests alongside complex healthcare fraud and abuse laws such as the Anti-Kickback Statute (AKS), False Claims Act risks related to billing practices, HIPAA regulations governing patient data privacy and security, state laboratory licensure requirements, and international data protection standards including GDPR.

Reimbursement uncertainties persist especially regarding government programs like Medicare where future payment rates remain subject to policy changes amid broader cost containment efforts . Compliance efforts require substantial resources given overlapping regulations.

The firm also faces patent litigation risks common across biotechnology sectors where infringement claims could impose costly legal proceedings potentially delaying commercialization or necessitating royalty payments [S17][S20][S24].

Returns & Capital Allocation

Despite improvements in operating results since peak losses recorded in prior years, Adaptive continues generating substantial operating losses (-$57 million in FY2025) accompanied by negative free cash flow estimated at approximately -$49 million after accounting for capital expenditures [F1]. Shareholders’ equity stabilized at approximately $219 million at the end of 2025.

No dividends or share repurchases have been declared or indicated given continued prioritization of reinvestment into R&D and commercial initiatives amid unprofitability.

Return on equity remains negative near -27% for FY2025 reflecting ongoing net losses despite progress toward narrowing operational deficits.

Outlook & Key Considerations

While explicit forward guidance is not detailed,[N3] key factors to monitor include:

- Quarterly revenue trends following recent earnings misses,

- Developments in reimbursement policies especially Medicare’s coverage decisions,

- Success extending clonoSEQ indications or launching new Immune Medicine products,

- Management’s ability to control operating expenses amidst growth initiatives,

- Potential patent disputes or regulatory investigations that could impact operations.

Conclusion

Adaptive Biotechnologies occupies a distinctive position through its innovative immune medicine platform decoding adaptive immunity at scale alongside FDA-cleared MRD diagnostics integrated into clinical workflows. The company benefits from robust intellectual property protection and collaborative partnerships but continues facing significant losses driven by investments necessary for market penetration amid uncertain reimbursement landscapes.

Persistent regulatory complexity adds operational risks while competitive dynamics require sustained innovation investments. Investors should closely observe execution on expanding clinical adoption of clonoSEQ alongside developments within Immune Medicine offerings as these underpin any pathway toward sustained profitability.

This analysis is intended solely for informational purposes without constituting investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments