How Addus HomeCare’s Capital Allocation Shapes Its Growth Trajectory

Addus HomeCare demonstrates robust financial momentum underpinned by strategic capital deployment amid evolving regulatory landscapes.

Addus HomeCare Corp posted significant operating and net income growth in fiscal 2025, supported by efficient service delivery and favorable reimbursement trends. The company balances this growth with disciplined capital allocation, including moderate capex investments and selective share repurchases, while maintaining a strong liquidity profile. Regulatory uncertainties remain a key risk, underscoring the importance of monitoring policy developments alongside operational execution.

Robust Growth Journey: Analyzing Addus HomeCare’s Historical Financial Performance

Addus HomeCare demonstrated notable financial acceleration in the fiscal year ended December 31, 2025. Operating income surged to $138.6 million, up approximately 35% from $102.7 million in 2024, outpacing the more moderate annual gains seen earlier in the period (e.g., $68.7 million in 2022) [F1]. This compounding profitability reflects not only growing scale but also margin enhancements. Net income mirrored this pattern, climbing to $95.9 million in 2025, representing a roughly 30% increase year-over-year from $73.6 million in 2024, continuing a steady upwards trajectory over the preceding three years (FY2022: $46.0 million) [F1].

Operating cash flow exhibited resilience through these periods of expansion, with CFO at around $111.5 million in FY2025, a slight decline from $116.4 million in FY2024 but still substantially above the FY2022 figure of about $105.1 million, illustrating stable cash generation even amid investment phases [F1]. Capital expenditures increased moderately to about $7.7 million in FY2025 versus $6.0 million the prior year—indicative of targeted reinvestment to sustain growth dynamics without excessive capital strain typical for labor-intensive home healthcare operators [F1]. This balance is critical for service-intensive sectors where asset light models predominate.

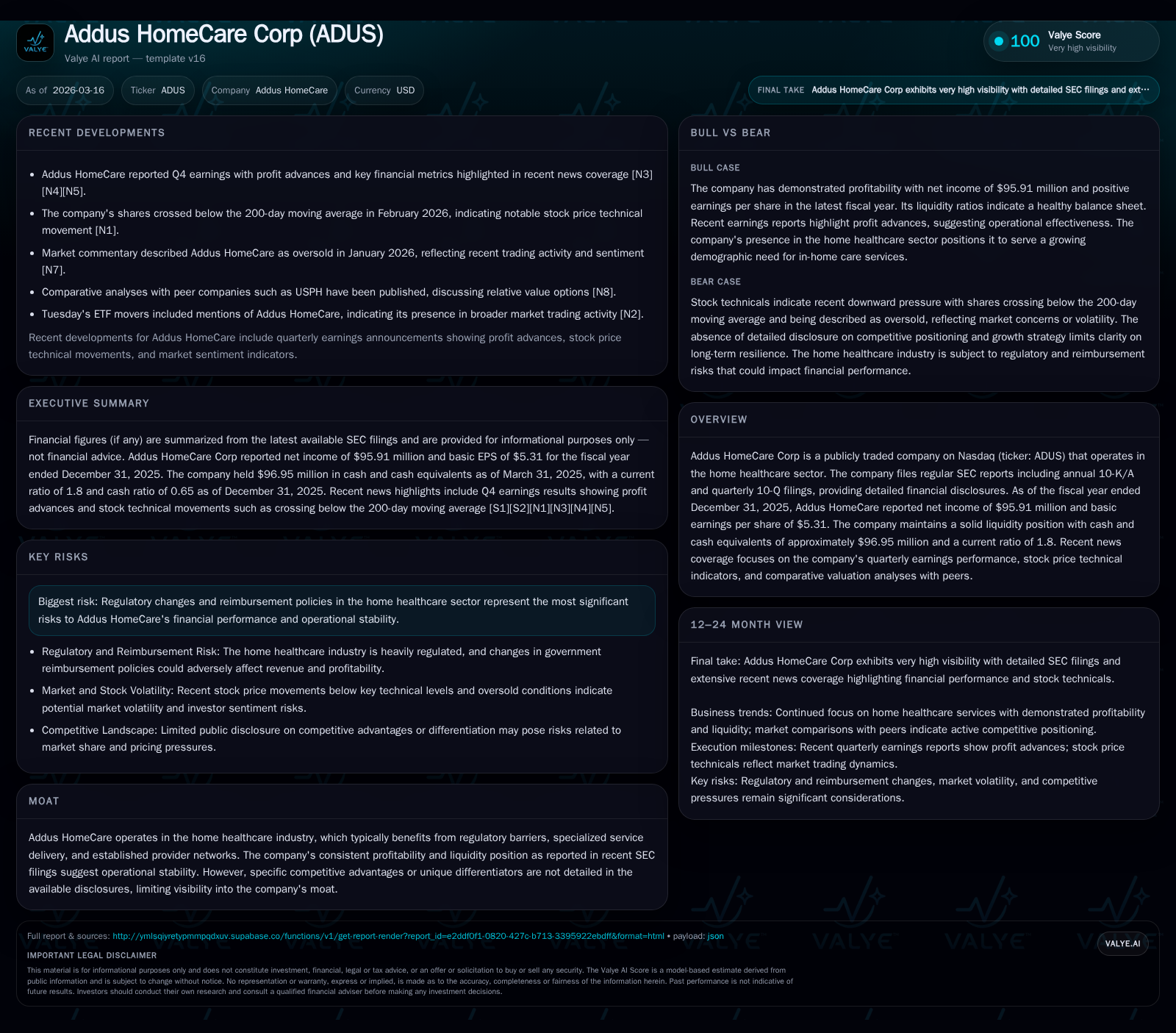

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 96 | 112 | 139 | 8 | +30.3% |

| 2024 | 74 | 116 | 103 | 6 | +17.7% |

| 2023 | 63 | 112 | 91 | 9 | +35.8% |

| 2022 | 46 | 105 | 69 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 104 | 8.8 |

| 2024 | 110 | 7.6 |

| 2023 | 103 | 8.8 |

| 2022 | 97 | 7.3 |

Source: SEC companyfacts cache [F1].

Shows accelerating EBITDA-like performance alongside modest capex increase; reflects compound operational leverage typical for homecare services.

Drivers Behind the Surge: Key Operational Catalysts Elevating Profitability

Addus’ expanding margins stem from several operational drivers central to home healthcare delivery economics. A core contributor lies in improved provider network efficacy—streamlining patient care coordination across diverse geographies without sacrificing quality or compliance fosters favorable cost structures documented during Q4 earnings beat commentary [N2][N6][S3]. Furthermore, Addus has benefited from nuanced shifts in reimbursement policies that allowed better alignment between service utilization and payment rates within Medicaid and Medicare programs—a factor tightly monitored due to its sensitivity but evidently positive for recent margins [N1][F1].

Operational efficiencies also hinge on leveraging technology-enabled care models and workforce flexibilities that reduce unnecessary overheads while boosting direct patient contact time—an imperative given labor challenges prevalent across the sector. Such dynamics support revenue quality as reflected in rising net margins alongside top-line expansion.

These factors have culminated in a meaningful jump not only in operating metrics but also bottom-line profitability, highlighting how adept management of reimbursement intricacies combined with operational focus can drive compounded earnings growth even amid sector-wide pressures.

Regulatory Headwinds and Sector Dynamics: Implications for Future Expansion

Despite strong recent performance, Addus faces material regulatory risks that could temper future growth sustainability. The company explicitly highlights exposure to government reimbursement policy changes—including rate adjustments under Medicaid waivers and Medicare Advantage plan expansions—that could quickly alter revenue profiles if unfavorable modifications occur [S4][S5][S19][N1].

Compliance requirements impose additional burdens related to licensure, reporting standards, and quality benchmarks—with enforcement intensifying across states—which elevate operational costs and can slow geographic scaling efforts if not managed proactively.

Moreover, litigation risks due to regulatory interpretations or data privacy issues represent episodic factors that can impact both reputation and financials given the sensitive nature of healthcare data.

Thus, while Addus’ recent success underscores adept navigation within these complexities, stakeholders should maintain vigilance around policy environments that historically have been volatile, particularly as federal healthcare reform debates continue.

Capital Allocation Strategy: Dividends, Buybacks, and Investment Initiatives

Addus pursues a disciplined capital allocation framework balancing dividend returns with buyback initiatives consistent with free cash flow availability [S6][S7][S18]. Dividend declarations contribute to shareholder yield but are calibrated conservatively in proportion to net income and operating cash generation.

The firm periodically executes share repurchases opportunistically to support per-share metrics while avoiding excessive leverage escalation—a notable practice given healthcare’s project-driven capital demand yet Addus maintains moderate capex levels primarily for technological enhancements or selective facility upgrades rather than broad asset acquisitions [F1].

Reinvestment efforts target sustainable scale improvements—both organic through network expansions and inorganic via strategic acquisitions—which complement internal cash flow deployment strategies designed to preserve liquidity amidst regulatory complexity.

Such measured allocation aids long-term shareholder value creation by optimizing balance sheet flexibility without curtailing growth investments.

Financial Strength Metrics: Liquidity, ROE, and Cash Flow Sustainability

Liquidity metrics affirm Addus’ stable financial footing ahead of prospective uncertainties. As of end-2025, the current ratio stood at approximately 1.8—a comfortable buffer substantiated by reported current assets of roughly $269 million against liabilities near $149 million [F1]. Cash and equivalents were close to $97 million earlier that year supporting operational needs and tactical funding initiatives.

Return on equity hovered near 8.8%, balancing sizeable net income with an expanding common equity base above $1 billion—pointing toward consistent profitability relative to invested capital over time [F1]. Notably, free cash flow approximated $104 million after deducting capex from operating cash flows indicating ample internal funding capacity post-investments.

This robust cash flow profile aligns well with typical home healthcare sector characteristics where capital intensity is moderate but working capital demands require careful management due to payer mix variability.

Hence, Addus possesses effective financial resilience enabling both strategic maneuverability and risk mitigation amidst evolving market conditions.

What Investors Should Monitor: Upcoming Milestones and Potential Risks

While explicit forward guidance is scarce in public disclosures [N3], key areas warrant attention going forward:

- Regulatory updates impacting Medicaid/Medicare reimbursement levels or structural reform efforts could materially affect top-line trajectories.

- Quarterly earnings releases will reveal whether operational efficiencies continue enhancing margins or if cost pressures emerge anew.

- Share price movements crossing critical technical thresholds such as the 200-day moving average may signal shifts in market sentiment amid macroeconomic headwinds [N5].

- Integration progress of new executive leadership appointed recently suggests potential shifts in strategic direction influencing medium-term outcomes [S23].

- Litigation developments related to compliance or data security remain latent event risks requiring monitoring through SEC filings ([S19]) or news channels.

Vigilance over these milestones alongside portfolio composition adjustments may guide anticipatory responses reflecting underpinning business fundamentals juxtaposed with external volatility.

Disclaimer: This analysis synthesizes reported financial data and corporate disclosures as provided through SEC filings and public news sources without incorporating speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments