AltEnergy Acquisition Corp’s IPO Proceeds and Deadline Extensions Underpin Its SPAC Journey

A comprehensive review of AltEnergy Acquisition’s capital structure, operational dormancy, and multiple deadline extensions frames its uncertain SPAC trajectory.

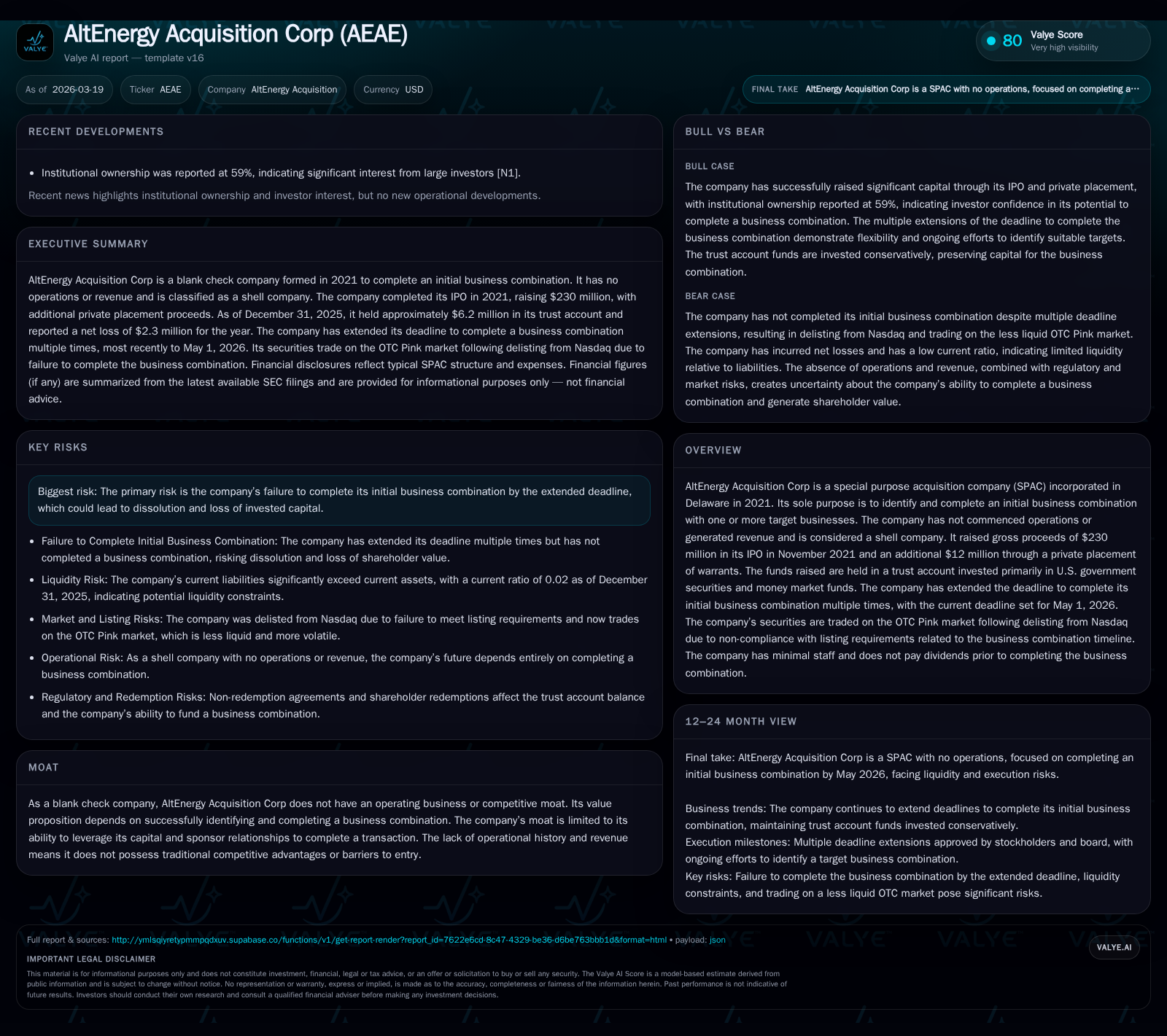

AltEnergy Acquisition Corp raised $230 million in its November 2021 IPO alongside a $12 million warrant private placement, securing substantial capital for a business combination. However, the company has not commenced operations or generated revenue, remaining a shell entity dependent on completing a deal by the extended deadline of May 1, 2026. Repeated deadline extensions and limited operational progress highlight risks including potential dissolution and investor redemption challenges. Sponsor loans have partially supplemented working capital needs amid ongoing negative earnings and cash flows, while buybacks and equity trends reflect attempts at capital management within these constraints.

Early Capital Raise and Structural Setup: Foundation of AltEnergy Acquisition Corp

AltEnergy Acquisition Corp launched as a Delaware-based special purpose acquisition company (SPAC) in February 2021, executing an initial public offering (IPO) on November 2, 2021. The IPO offered 23 million units at $10 each, including a full exercise of the underwriters' over-allotment option for three million units, grossing $230 million in proceeds [S1]. Concurrently, a private placement was executed selling 12 million warrants at $1 apiece to the Sponsor and BRPI affiliates, yielding an additional $12 million [S1]. The founder shares totaling approximately five and three-quarter million were issued earlier at nominal price ($25,000 aggregate). After gross underwriting discounts and commissions totaling about $4.6 million plus other costs near $635,000, net proceeds settled around $236.8 million.

From the net proceeds, approximately $234.6 million was placed into a U.S.-based trust account managed by Morgan Stanley with Continental Stock Transfer & Trust Company acting as trustee [S1][F1]. This trust arrangement aligns with typical SPAC mechanics, safeguarding IPO capital until the consummation of a qualifying business combination or return to investors upon failure. The trust assets are invested primarily in U.S. government securities or money market funds meeting regulatory criteria.

These structural elements—comprising public units with redeemable warrants, founder shares with limited seniority rights pre-combination, and a regulated trust account—set the financial framework enabling AltEnergy Acquisition to pursue its mission of effecting an initial business combination.

Track Record of Operational Dormancy and Financial Performance

Since inception through FY2025, AltEnergy Acquisition Corp has remained operationally dormant without revenue-generating activities typical of active companies [S1][F1]. It qualifies as a "shell company" per Exchange Act standards due to this lack of operations.

Financially, the company has consistently posted net losses except for FY2023 when it reported net income of roughly $2.47 million [F1]. However, net income reverted negative in FY2024 (-$2.70 million) and FY2025 (-$2.34 million), indicating ongoing expenses exceeding any non-operating gains such as interest income from trust assets or changes in warrant valuation.

Operating cash flow has been negative throughout this period as well; -$1.55 million in FY2022 deepening to approximately -$2.56 million in FY2023 before improving slightly but remaining negative (-$1.77 million in FY2024; -$1.80 million in FY2025) [F1]. Cash burn reflects operational costs tied primarily to administrative expenses rather than investments or capex.

Equity positions illustrate an increasingly negative balance reaching nearly -$18.7 million by FY2025 year-end due mostly to accumulated net losses and liabilities possibly including sponsor loans [F1]. The current ratio based on latest available data is extremely low (~0.02), signifying minimal current assets relative to liabilities on the balance sheet [F1].

A summary view follows:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -2 | -2 | +13.3% |

| 2024 | -3 | -2 | -209.1% |

| 2023 | 2 | -3 | -80.8% |

| 2022 | 13 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 3 | 12.5 |

| 2024 | 10 | 16.7 |

| 2023 | 222 | -19.2 |

| 2022 | -135.4 |

Source: SEC companyfacts cache [F1].

This table highlights persistent financial stress outside the outlier positive net income year.

Multiple Deadline Extensions: Rationale and Market Impact

Originally endowed with an eighteen-month window from IPO closing to consummate an initial business combination—set for May 2, 2023—the company has requested multiple stockholder-approved extensions to this deadline [S4][S5]. These extensions include:

- May 2, 2023 → Extended to May 2, 2024

- May 2, 2024 → Further extended with provisions for up to six one-month increments through May 2, 2025

- May 2, 2025 → Final extension granted up to May 1, 2026 [S4][S5]

Such repeated postponements underscore challenges either in identifying suitable merger targets or securing transaction agreements acceptable to all parties involved [S4][S5]. Each extension carries implications regarding shareholder confidence — notably influencing redemption activity where stockholders elect early exit against perceived dilutive risk or uncertain prospects.

Though extensions provide breathing room for strategic transaction execution without immediate liquidation risk [S4], they raise questions around deal readiness and counterparty availability amid competitive SPAC markets saturated post-2020–21 peaks.

Current Liquidity, Trust Account, and Sponsor Loans Overview

As of December 31 2025,the Trust Account balance dwindled to about $6.2 million — down substantially from initial deposits exceeding $230 million due principally to redemptions where shareholders cashed out their Class A shares [S5][S9]. Additionally,cash held outside the Trust Account available for working capital stood at roughly $19 thousand [S9].

Sponsor loan facilities have been deployed incrementally over multiple commitment letters totaling over $3.8 million outstanding plus accrued interest ($210 thousand approx.) at year-end designed mainly to bridge working capital shortfalls as operational costs mount absent revenue intake [S3][S22]. These loans carry interest approximating mid-term federal rates and possess optional conversion features into private placement units at $1 per warrant — functioning as quasi-equity elements enhancing sponsor leverage without immediate cash impact [S3].

No convertible working capital loans were outstanding for FY2024/25 periods besides these sponsor notes; repayments occur upon successful business combinations or otherwise from non-Trust funds if necessary — preserving principal redemption value held for public shareholders within Trust [S3][S22].

Risks to Investors: Redemption Rights and Potential Dissolution

Investors face significant risks rooted primarily in failure scenarios where AltEnergy Acquisition cannot finalize a qualifying business combination by May 1 2026 [S7][S8]. In such event,the Company must redeem public shares pro rata based on Trust Account valuations then existing —minus amounts allocated for dissolution costs capped at roughly $100 thousand — effectively initiating wind-down processes extinguishing ordinary shareholder equity rights [S7][S8].

Founder Shares holders waive rights to liquidating distributions but may acquire exposure if these shares convert post-IPO trading given specific conditions outlined in governing agreements —revealing layers of complexity atypical outside SPAC frameworks [S7].

No dividends or traditional buybacks occur given corporate dormancy; buybacks detected correspond primarily with partial share repurchase programs potentially aimed at structural optimization rather than value returns typical in operating firms [S4][F1].

Moreover,the Trust Account's protection mechanism includes indemnities whereby the Sponsor accepts liability if creditor claims reduce funds below predefined thresholds — though these protections may not fully shield investor capital should third-party claims prove substantial or unenforceable waivers arise [S9].[N/A]

Future Outlook: Probability and Constraints for Business Combination Completion

Absence of disclosed merger targets or business combination candidates injects uncertainty surrounding the viability of achieving consummation before May 1 deadline despite prior extensions affording preparation time [S4][S5]. No recent public news amplifies this ambiguity.

Key constraints constricting likelihood include dwindled trust balances post-redemptions reducing deal negotiation flexibility alongside elevated sponsor indebtedness reflecting mounting working capital pressures absent revenue upside [F1][S3]. Prevailing market conditions curtailing appetite for late-stage SPAC deals also merit consideration though external economic forecasts fall outside company-specific evidence presented.

Given no forward-looking guidance provided by management or defined milestones beyond regulatory filing requirements, investors should monitor impending stockholder meetings that may address further amendments/extensions along with quarterly SEC reports that might shed light on progress.[/analysis]

Capital Allocation Strategy: A Lens on Returns, Buybacks, and Sponsor Support

AltEnergy’s atypical capital allocation reflects its inherent blank-check status: there are no dividends distributed nor meaningful ROE driven by earnings — currently negative (approximate implied ROE near +12% based on net loss relative to negative equity reflects accounting anomaly rather than profitable return)[F1].

Noteworthy are share repurchases approximating $9.5 million in FY2024 falling sharply to roughly $2.6 million in FY2025 — indicative of sporadic efforts possibly designed to adjust share structure following wave-like redemption activity as deadlines approached [F1][S4][S5].

Sponsor loans totaling nearly four million signal continued backstop funding crucial for survival through expiration thresholds while maintaining options around convertible instruments allowing dilution mitigation strategies post-transaction completion[S3][F1].

Collectively this paints a picture more aligned with propping operational viability than pursuing direct investor yield enhancement prior to substantive business combination closure.

Monitoring Milestones: Key Events to Watch for Remaining Timeline

Critical upcoming event remains the May 1 2026 deadline mandated for consummation of an initial business combination [S5]; failure results in forced redemption offerings followed by corporate wind-up.

Stockholders retain voting rights regarding potential further extensions though company amended certificate allows Board limited powers for incremental extension approvals without fresh shareholder consents subject to notification windows[S4][S5]. Any such decisions will materially influence investment horizon risk profiles.

Close attention should be paid to filings revealing:

- Proxy statements relating to merger approval votes,

- Disclosure around potential candidate negotiations,

- Updates on sponsor loan utilization,

- Changes in Trust Account valuations potentially indicating new redemptions,

- Communications regarding amended charter provisions impacting redemption policies. The absence of these signals could foreshadow imminent milestone failures or accelerated liquidations.[/analysis]

Disclaimer: This report synthesizes information drawn exclusively from publicly filed sources including SEC disclosures and companyfinancial data as of March 19th , 2026 . It does not constitute investment advice or recommendations but serves analytic purposes grounded strictly on verified filings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments