AudioEye Inc's Q1 2026 Review: Revenue Resilience Contrasted by Liquidity Challenges

AudioEye’s latest quarter shows steady revenue but highlights liquidity pressures amid ongoing losses.

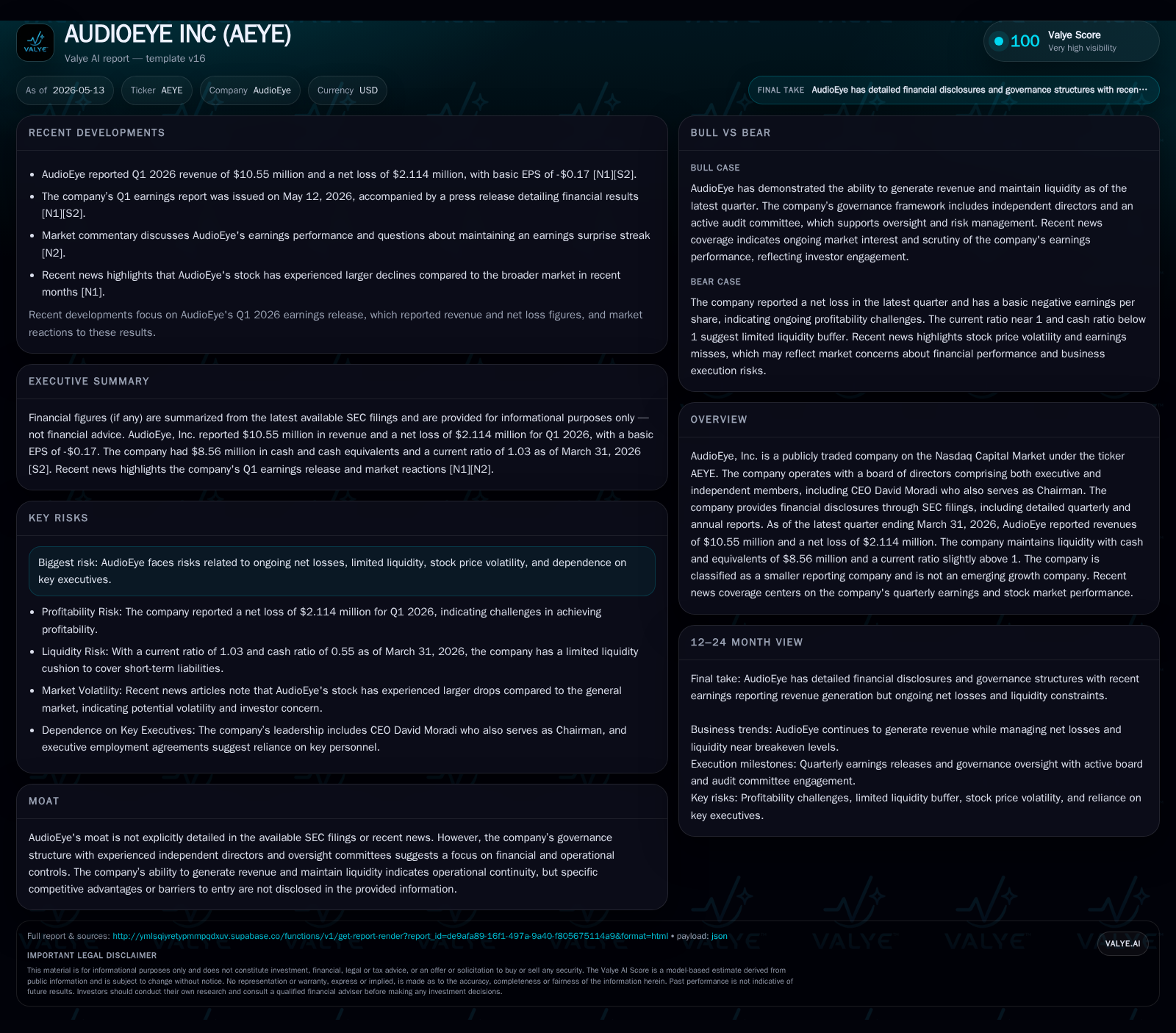

In Q1 2026, AudioEye Inc. delivered revenues of $10.55 million, demonstrating resilience in its digital accessibility services. However, the company posted a net loss of $2.11 million and held cash of $8.56 million against total debt near $17 million, resulting in a tight current ratio of 1.03. The business operates primarily through a SaaS model focused on web accessibility compliance, supported by regulatory demand but facing competitive fragmentation and financial constraints. Key risks include sustained net losses, liquidity strain, and dependence on executive leadership. Upcoming milestones include monitoring revenue trends and capital structure management to assess sustainability.

Q1 2026 Operating Update Highlights

AudioEye Inc's first quarter results for fiscal 2026 underscore a mixed operational scenario. The company reported revenues of $10.55 million, affirming persistent demand for its web accessibility solutions despite the broader technology market volatility [S2]. Yet, it recorded a net loss of roughly $2.11 million in this period, indicating continued challenges in scaling profitably.

On the balance sheet front at March 31, 2026, AudioEye held cash and equivalents totaling approximately $8.56 million against a sizable total debt load around $17 million, culminating in an estimated net debt position near $8.4 million [F1]. Current assets stood at about $15.88 million while current liabilities were close at $15.44 million, producing a current ratio of 1.03 [F1]. These financial metrics reflect a company navigating ongoing losses while striving to maintain operational continuity in a capital-intensive SaaS environment.

AudioEye’s Business Model and Value Proposition

AudioEye specializes in digital accessibility technology designed to help websites comply with legal standards ensuring access for people with disabilities [S1]. Its product suite primarily includes software-as-a-service offerings that automate or assist in meeting compliance requirements such as those mandated under the Americans with Disabilities Act (ADA) and Section 508 regulations.

Revenue is largely generated through subscription fees paid by clients—including public sector entities and private companies—to maintain compliant online presences over time. This recurring revenue model aligns sales incentives with ongoing service delivery but invariably requires continuous feature updates and customer support investments.

Notably, recent governance shifts highlighted in filings indicate an executive team focused on operational discipline and shareholder alignment—a positive factor as the company seeks sustainable growth paths amid competitive pressures [S1].

Industry Environment and Competitive Positioning

Operating within the niche but growing market for digital accessibility compliance solutions places AudioEye amid an industry influenced heavily by regulatory drivers rather than pure market demand cycles [S1]. As governments worldwide intensify enforcement actions related to web accessibility violations, providers like AudioEye capture structurally supported demand.

However, competition appears fragmented among various SaaS vendors offering overlapping capabilities, often differentiated by technology sophistication or client sector focus. In filings there is no clear moat outlined beyond governance rigor; thus, AudioEye must sustain innovation pace and client relationships to defend against pricing pressure or churn from alternative providers [S1].

Integration complexities with diverse website platforms and emerging technology standards pose ongoing operational challenges that industry participants must manage carefully.

Growth Opportunities and Expansion Catalysts

Key growth drivers articulated implicitly through recent quarter disclosures include expanding the company’s footprint across public sector mandates nationwide alongside increased uptake within private enterprises aiming to preempt litigation risks [S2][S3][S1]. Regulatory enforcement intensification acts as a structural tailwind supporting recurring subscription renewals and potential upsell opportunities.

Furthermore, delivering enhanced product features that improve ease-of-use or address broader accessibility frameworks could bolster customer retention rates and average revenue per user metrics.

The SaaS cost structure potentially enables favorable operating leverage if scale accelerates without proportionate increases in fixed expenses, providing a pathway toward margin improvements pending successful execution.

Risks and Constraints Influencing Performance

Official risk disclosures highlight key challenges facing AudioEye. Persistent net losses underline an urgent need for sustainable profitability; without improvement there will be continuous pressure to access external capital markets or alternative financing routes [S2]. Stock price volatility compounds these financial strains by limiting flexibility for equity raises or strategic partnerships reliant on market confidence metrics [S2]. Executive leadership transitions present execution risks given the concentrated dependence on certain individuals to steer product development and customer acquisition efforts [S1]. Ensuring leadership continuity while managing resource limitations will be crucial.

Near-Term Milestones and Key Monitoring Points

Stakeholders should closely monitor forthcoming quarterly earnings reports for evidence of revenue acceleration or margin expansion that could signal effective scaling of core offerings post recent leadership changes [S2][N3][N4]. Liquidity events such as debt refinancing outcomes or cash flow improvements will materially influence operational runway length.

Additionally, announcements regarding new contracts especially large government procurements or pilot program successes might serve as leading indicators for growth momentum. Shareholder communications relating to capital allocation strategies are also pivotal given the high leverage state [S3].

Overall execution on these fronts will determine if AudioEye can transition from resilient revenue generation toward viable profitability trajectories.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $9mm | |

| 2026-03-31 | ||

| Total debt | $17mm | |

| 2026-03-31 | ||

| Net debt | $8mm | |

| 2026-03-31 | ||

| Current assets | $16mm | |

| 2026-03-31 | ||

| Current liabilities | $15mm | |

| 2026-03-31 | ||

| Current ratio | 1.03x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | As of |

|---|---|---|

| Revenue (LTM) | 40,311,000 | |

| 2025-12-31 | ||

| Net Income (Loss) | -3,077,000 | |

| 2025-12-31 | ||

| Cash & Equivalents | 8,563,000 | |

| 2026-03-31 | ||

| Total Debt | 17,000,000 | |

| 2026-03-31 | ||

| Current Assets | 15,876,000 | |

| 2026-03-31 | ||

| Current Liabilities | 15,436,000 | |

| 2026-03-31 |

This snapshot confirms AudioEye’s ability to generate significant revenue but also underscores persistent losses alongside a balance sheet reflecting stretched liquidity conditions requiring careful stewardship [F1].

This analysis is based solely on publicly available SEC filings dated through May 12, 2026, company disclosures, and recent news reports without investing recommendations or projections.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments