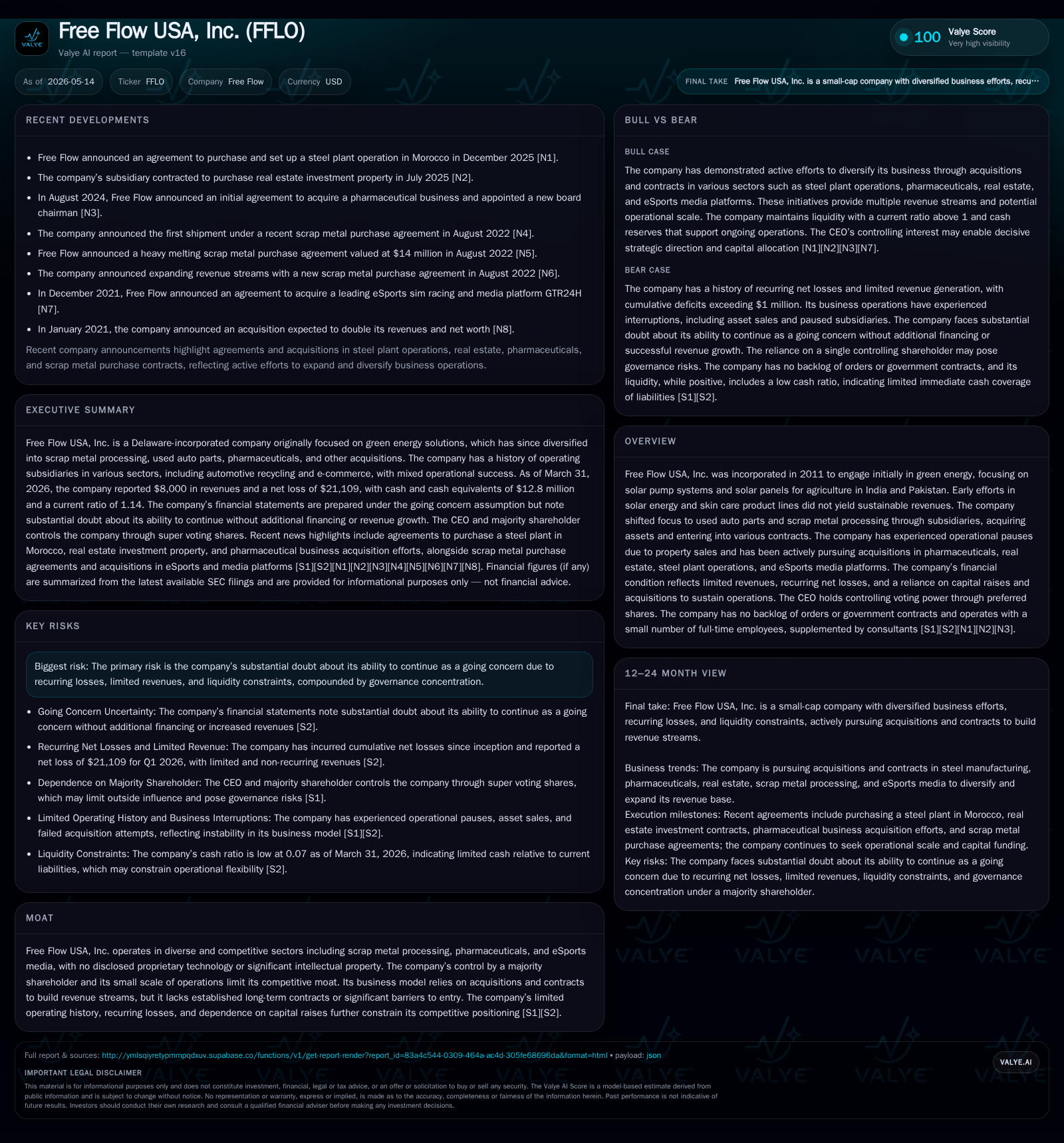

Free Flow USA: Balancing Acquisition Ambitions with Operational Pause

Free Flow USA’s latest quarterly filing reveals ongoing inventory valuation challenges and reliance on promissory notes amid stalled acquisitions and operational pauses.

Free Flow USA, Inc. continues its struggle to generate sustainable revenues as reflected in the recent 10-Q, which highlights potential impairments tied to uncertain demand and recurring stock-based compensation costs. The company’s historical pivot from green energy to auto parts resale and scrap metal processing has been marked by pauses and asset sales, leading to a fragmented business model largely dependent on pending acquisitions. Operational risks include liquidity constraints, high debt held via promissory notes without fixed repayment terms, and governance concentration under the CEO. Future growth hinges on successfully closing acquisitions and contracts that have so far been impeded by audit hurdles and financing challenges.

Quarterly Review Highlights and Operational Implications

The most recent quarterly filing dated May 14, 2026, (Form 10-Q) underscores Free Flow USA’s ongoing operational challenges with a clear focus on inventory valuation adjustments tied to fluctuating demand estimates. The company applies a lower of cost or net realizable value approach for inventory accounting; however, net realizable values depend heavily on anticipated demand that remains uncertain. Should actual demand underperform forecasts, the Company will need to recognize incremental downward adjustments during the reporting period. Such disclosures highlight both weak market traction and potential impairments looming over the inventory carrying values [S2].

Additionally, the firm continues to incur stock-based compensation expenses classified as consulting costs per ASC 718 guidelines. These non-cash but dilutive charges increase operational expense burdens even as cash remains scarce—an indicator of ongoing cost pressures despite minimal revenue generation from core business lines [S2].

This combination of inventory risk exposure linked to volatile demand alongside persistent stock-based compensation expense signals systemic instability in Free Flow’s business operations. Both factors reduce margin prospects and underline mounting challenges in building sustainable earnings.

Evolution of Business Model and Core Revenue Sources

Free Flow USA’s business trajectory since incorporation in 2011 has been characterized by frequent pivots across unrelated industry verticals without establishing consistent revenue sources. Initially targeting green energy applications like solar pumps for agriculture in India and Pakistan, the company failed to secure stable contracts or scale sales volumes due partly to volatile solar panel market pricing [S1].

Attempts at diversifying into a skin care product line via subsidiary Promedaff, Inc. similarly faltered, culminating in liquidation of inventory and cancellation of related promissory notes without generating meaningful revenue streams [S1].

From 2016 onward, the company shifted focus toward selling used auto parts through subsidiaries including Accurate Auto Parts, Inc., but these operations were hindered by property lease issues following landlord bankruptcy leading to an operational pause in mid-2017. While assets were later sold off with significant debt repayment, those moves effectively suspended the division's revenue generation capability [S1][S6].

Currently active operations are limited largely to scrap metal processing conducted through subcontractors pending contract finalization. The company’s other subsidiaries remain dormant or inactive following asset divestitures driven by capital shortages and regulatory hurdles [S4][S7].

The absence of any government contracts or order backlogs further emphasizes lack of stable recurring income sources. Revenue recognition remains nominal—reported consulting revenue reached only $30,000 in late 2025 connected primarily with ancillary services rather than core industrial activities [F1][S23].

Competitive Complexities Across Multi-Sector Ventures

Operating across heterogeneous sectors such as scrap metals trading, pharmaceutical acquisitions attempts, real estate investments, and eSports media platforms has diluted managerial focus while exposing Free Flow USA to highly fragmented competition sets devoid of significant technological differentiation or intellectual property advantages [S1][S2].

In scrap metal processing—a market dominated by established regional recyclers—the company participates through subcontracting arrangements without scale advantages or proprietary processing capabilities. Similarly in pharmaceuticals, acquisition targets have repeatedly failed audit compliance reviews precluding deal closure[S4][S7]. Media ventures face steep customer acquisition costs amid saturated digital content ecosystems.

Compounding these external pressures is governance concentration: the CEO holds all super-voting preferred shares granting decisive influence over strategic direction with minimal external input or counterweight. This concentration may exacerbate risks related to capital allocation inefficiencies or transactional opacity [S1].

The result is a structurally weak competitive moat characterized by low barriers to entry for rivals and limited differentiation that collectively combine to inhibit sustained profitable growth.

Growth Initiatives and Pending Acquisition Prospects

Management continues an M&A-driven growth strategy seeking transformative acquisitions that could supply meaningful revenue pipelines absent organic volume expansion. Since relocating corporate offices to New Jersey post-asset sales in early 2024, Free Flow has pursued various acquisition opportunities primarily targeting pharmaceutical firms but has encountered significant setbacks due to due diligence failures stemming from inadequate audited financial statements produced by targets [S4][S7].

These repeated failures elongate timelines before accretive deals can close—extending periods of stagnation while relying heavily on capital raises for survival rather than operational cash flow.

Moreover, several subsidiaries remain inactive due to suspended operations after property disposals—indicating that pipeline bottlenecks have impaired capacity building initiatives.

Going forward, progression toward closing contract negotiations within scrap metal processing businesses and concluding credible acquisition agreements represent pivotal near-term growth catalysts but are yet contingent on overcoming audit compliance issues and securing financing support commitments.

Operational Risks, Governance Concentration, and Liquidity Constraints

Debt obligations primarily consist of promissory notes amounting to approximately $700,935 resulting from conversions of Series B & C redeemable preferred shares previously held by affiliated parties under conditions where no fixed payback dates exist; these notes bear no interest but represent latent repayment risk contingent on cash availability and creditor consent [S2].

No definitive timelines are provided within filings but management projects ongoing discussions hinting at near-term resolutions potentially within forthcoming quarters [S2][S4][S7].

Latest Financial Snapshot: Liquidity, Debt, and Profitability Metrics

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $12,847 | |

| 2026-03-31 | ||

| Current assets | $206,239 | |

| 2026-03-31 | ||

| Current liabilities | $180,239 | |

| 2026-03-31 | ||

| Current ratio | 1.14x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This snapshot illustrates constrained liquidity with near-balance sheet parity between current assets and liabilities but very low absolute cash reserves undermining operational flexibility. Losses persist reflecting ongoing expense burdens outstripping limited revenues. Debt primarily comprises promissory notes converted from preferred shares with no fixed repayment dates, underscoring the need for sustainable funding sources for viability [F1][S2].

This analysis synthesizes filings up through Q1 2026 without projecting beyond documented statements or internal plans disclosed by Free Flow USA. It does not constitute investment advice but rather an evidentiary summary aimed at understanding structural dynamics impacting this small-cap diversified holding entity contending with acute operational pauses amid acquisition ambitions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments