agilon Health’s Evolution in Medicare-Centric Care: Financial Strains and Strategic Adjustments

Exploring agilon Health’s financial trajectory alongside the opportunities and challenges of its capitated Medicare Advantage model.

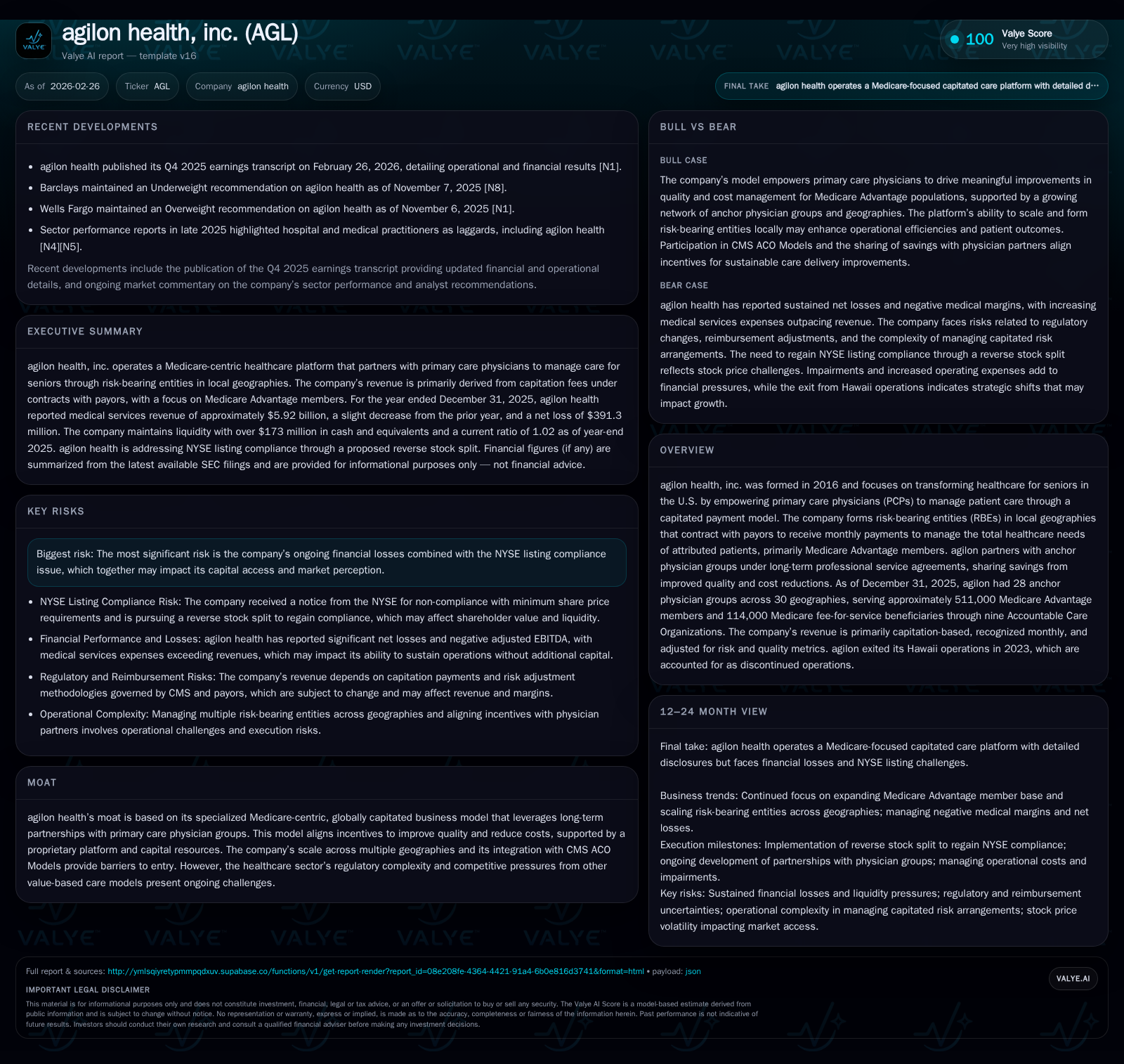

Since its inception in 2016, agilon Health has rapidly expanded its footprint in the Medicare Advantage space by leveraging a capitated payment model centered on primary care physician partnerships. Although membership grew notably from 388,400 MA members in 2023 to approximately 511,000 in 2025, the company has faced increasing revenue pressures with a declining medical margin and escalating operating losses. As of FY2025, net losses deepened to $391 million amid platform costs and regulatory challenges including NYSE listing compliance issues. The company’s capital structure adjustments and amendments to its credit facility aim to provide liquidity flexibility, but persistent negative cash flow and legal exposures underscore ongoing risks. Key milestones in 2026 will focus on stockholder votes for reverse splits and navigating regulatory hurdles while seeking operational stabilization.

From Rapid Expansion to Revenue Pressures: AGL’s Historical Growth Trends

agilon Health has charted a swift growth trajectory since its founding in 2016 by establishing strategic partnerships with primary care physician (PCP) groups under risk-bearing entities (RBEs). This Medicare-centric approach is geared toward managing total health needs of attributed members through capitated payments rather than fee-for-service.

The company increased its Medicare Advantage (MA) membership base significantly from approximately 388,400 members at the end of fiscal year (FY) 2023 to roughly 511,000 members by FY 2025—a growth of nearly 32% over two years [F1], [S1]. This growth included entering new geographies which expanded the footprint across 30 regions with 28 anchor physician groups as of December 31, 2025 [S26].

However, top-line revenue tells a more nuanced story. Medical services revenue totaled $5.9 billion in FY2025, slightly down from $6.05 billion in FY2024 despite membership expansion; this signals increasing price or reimbursement pressures or membership mix shifts diluting unit economics [F1]. Gross profit turned negative at -$160 million for FY2025 after modest gross profits in prior years ($4.8 million in FY24 and $69.7 million in FY23), highlighting margin compression likely driven by cost escalations or changes in claims experience [F1].

The medical margin metric—defined as medical services revenue less medical services expense—turned sharply negative at -$56.6 million versus a robust positive margin of $205 million one year earlier [F1]. New member additions are generally dilutive to per-member margins due to onboarding expenses and potential initial inefficiencies [S1]. Platform support costs remained elevated near $160 million annually reflecting sustained resource investments across regions despite margin declines [S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -391 | -106 | -463 | 13 | -50.4% |

| 2024 | -260 | -58 | -292 | 13 | +0.9% |

| 2023 | -263 | -156 | -232 | 16 | -146.4% |

| 2022 | -107 | -131 | -120 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 200 | -119 | |

| 2024 | 200 | -71 | -55.2 |

| 2023 | 200 | -172 | -39.7 |

| 2022 | 7 | -146 | -10.2 |

Source: SEC companyfacts cache [F1].

Table notes: Medical margin increasingly challenged as new geographies dilute margins; Operating loss deepens substantially despite revenue stability; Cash flow remains negative though fluctuates.

Medicare Advantage Members and Platform Metrics: Growth Deceleration and Margin Dynamics

While membership expansion reflects market reach gains, per-member profitability appears constrained by onboarding new enrollees who tend to depress measured medical margin per member per month (PMPM). This dilution effect is noted by management as a natural consequence when adding new geographic markets or physician groups early in their lifecycle before economies of scale materialize [S1].

Medicare Advantage fees are capitated based on an agreed percentage of CMS benchmark premiums with risk adjustments applied for patient health status—creating complex pricing dynamics sensitive to member risk profile changes over contract terms [S22]. Platform support costs include expenses for regional personnel supporting those new markets alongside essential administrative investments which have remained stubbornly high relative to revenues [S1]. This weighs on overall adjusted EBITDA—the company’s non-GAAP measure—which halved from a loss of $154 million in FY24 to nearly double that loss at $296 million in FY25 [F1].

Practitioner terminology such as "global capitation" refers to agilon’s fixed monthly payment arrangements with payors covering comprehensive patient care costs within defined populations via RBEs [S26]. The firm’s deployment of long-tenured professional service agreements incentivizes anchor PCP groups by sharing savings from improved care quality and cost management [S26]. However, these contracts also entail operational complexities balancing physician compensation structures against savings targets.

The Capitated Payment Model: Operational Strengths and Emerging Constraints

Agilon's Medicare-centric capitated payment model empowers primary care physicians via RBEs which bear downside risk but also share upside savings when quality improvements lower costs—mirroring evolving industry trends toward value-based care arrangements supported by CMS Accountable Care Organization models [S26]. This model attempts to realign incentives traditionally absent under fee-for-service paradigms.

The proprietary agilon platform integrates data analytics, population health management capabilities, and operational support infrastructure tailored explicitly for these global capitation arrangements—strengthening physician engagement and enabling timely interventions [S26]. The company's scale spanning multiple states offers cross-market learning benefits but also introduces substantial implementation complexity often accompanied by upfront investments impacting near-term margins.

Emerging constraints include increased competition from other value-based models competing for similar physician group alliances alongside the ever-shifting CMS regulatory landscape imposing reimbursement rule changes that can materially impact expected returns [S7], [S26]. Resource allocations must balance scaling new geographies without exacerbating existing financial pressures.

Navigating Regulatory and Listing Challenges Amid Financial Losses

Financial performance difficulties coupled with a sustained sub-$1 stock price triggered a formal NYSE notice citing non-compliance with listing standards effective November 2025 [S25]. To remediate this status, the company announced plans for a reverse stock split requiring shareholder approval slated for March 17, 2026—a critical vote with substantial implications for equity market perception and trading liquidity [N1], [S3], [S25].

Additionally, ongoing securities class action lawsuits and derivative litigations alleging misstatements related to financial guidance and operational execution add regulatory scrutiny risks that could weigh on management bandwidth and investor confidence throughout the discovery phases expected to extend into late 2026 [S11], [S12], [S13], [S29]. Such litigation risk exacerbates uncertainty amidst financial headwinds.

Capital Structure, Liquidity, and the Impact of Covenants on Corporate Flexibility

The company maintains a credit facility consisting of a secured term loan ($35 million outstanding at year-end 2025) plus a revolving credit facility (approximate availability of $16.8 million after letters of credit allocations) designed to provide necessary liquidity during operations and expansions [S4], [S5], [S6], [S14], [S15], [S19]. The term loan carries an effective interest rate near 8.19%, imposing ongoing debt service costs against already pressured earnings.

The credit agreement recently underwent its third amendment extending maturity from February 18, 2026 to February 18, 2028 while tightening covenants including daily minimum cash requirements ($50 million), conditioning dividends on consecutive positive EBITDA periods post-amendment date, reducing revolving commitments from $100 million to $90 million, and mandating letter-of-credit collateralization at levels exceeding outstanding amounts by approximately 103% [S6], [S10], [S12].

These covenants limit discretionary spending freedom especially concerning restricted payments such as dividends or share repurchases until operational profitability metrics improve sustainably.

Expectations and Key Milestones Ahead: What to Watch in 2026

Key forthcoming corporate events flagged include:

- Stockholder meeting scheduled mid-March (March 17) regarding approval for reverse stock split aiming toward NYSE compliance cure within the six-month grace period ending May/June timeframe post-notice issuance end-November '25 ([N1],[S25]).

- Continued progress toward operational scale efficiencies which may stabilize or improve medical margins important given guidance absence ([N1]).

- Litigation discovery developments—ongoing motions and clarifications associated with securities class actions may influence investor sentiment ([S11],[S12],[N1]).

- Monitoring CMS policy updates affecting capitation arrangements remains vital given industrywide regulatory flux ([S7]).

While explicit financial guidance remains limited publicly beyond earnings disclosures available as of February '26 ([N1]), market participants should track these milestones closely for indicators of operational turnaround commitment or potential restructuring outcomes.

Evaluating Capital Allocation: Cash Flow Realities Amid Losses and Buybacks History

Reflecting ongoing losses totaling approximately $391 million net income deficit in FY25 versus prior years’ deficits (~$260–262 million), agilon Health’s cash flows continue under pressure with operating cash flow at negative $106 million coupled with steady modest capital expenditure near $13 million annually indicative of measured investment pace aligned with cautious growth posture ([F1]). Free cash flow calculated as operating cash flow minus capex is deeply negative around -$119 million signaling no immediate capacity for shareholder returns outside potential buyback activities which have historically been inconsistent with reported repurchase totals up through FY23 periods but lacking recent confirmations ([F1]).

Dividends remain absent primarily due to not only credit facility restrictions but strategic need for cash conservation amid uncertain profitability trajectories ([S8],[F1]). Continued prioritization likely favors investment in platform development initiatives aimed at supporting longer-term sustainable growth over short-term distributions.

Disclaimer: This report is informational only; it does not constitute investment advice or recommendations regarding securities or strategies related thereto.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments