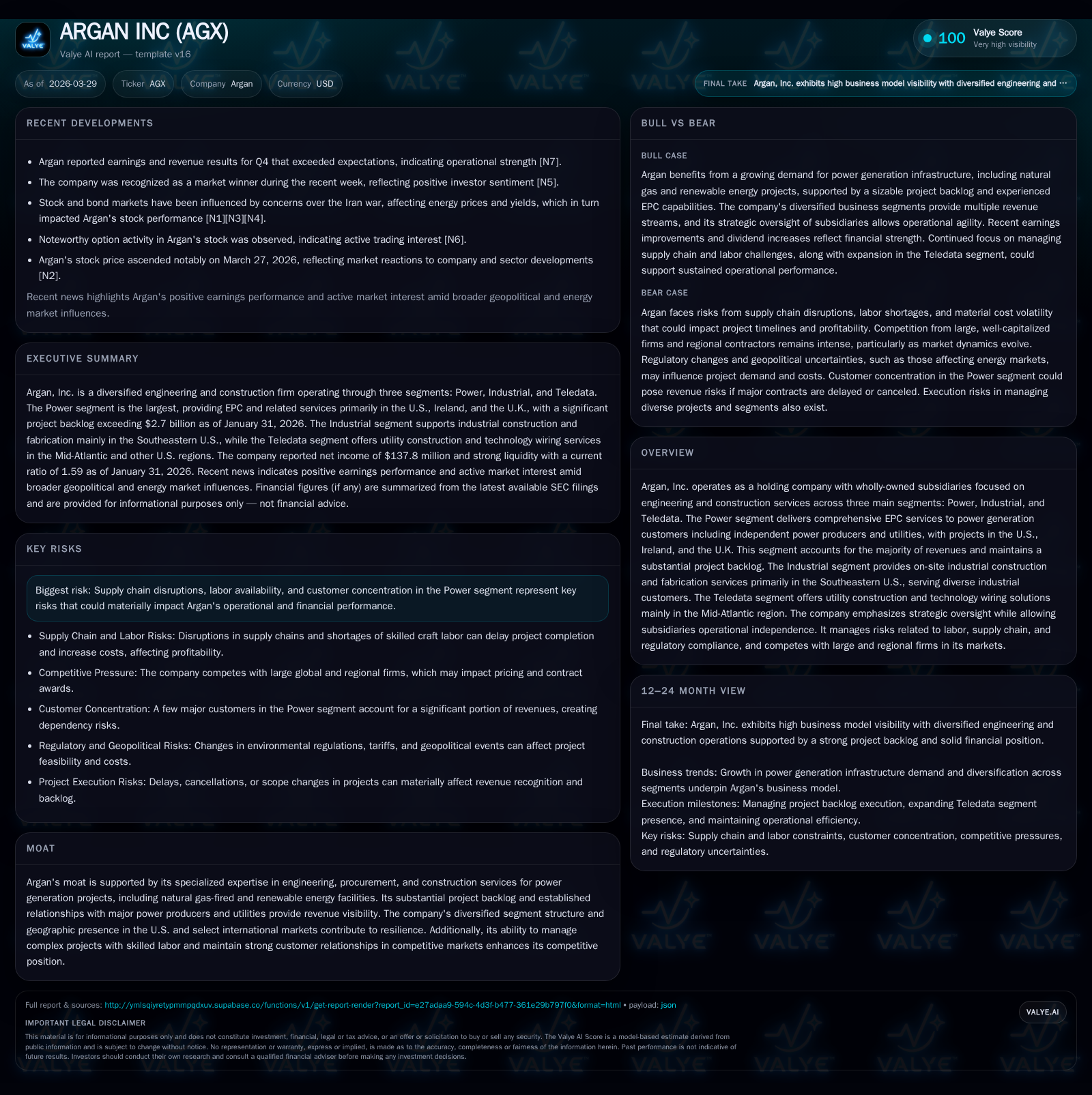

Argan’s Surge in 2026: Engineering Growth Fueled by Power Segment Momentum

Argan Inc’s strong fiscal 2026 financial results highlight the impact of its dominant Power segment and disciplined capital management amid industry cyclicality.

Argan Inc delivered a substantial leap in operating and net income alongside robust cash flows in fiscal year 2026, propelled primarily by its Power segment’s EPC projects across the U.S., U.K., and Ireland. Despite typical sector headwinds such as labor shortages and supply chain volatility, Argan’s backlog depth and multi-geographic reach have provided strong revenue visibility. The company’s modest capital expenditures combined with conservative buyback activity underline prudent balance sheet stewardship. Risks related to project timing, customer concentration, and ongoing legal disputes remain key factors to monitor.

From Cyclical Challenges to Breakout Growth: Argan’s Recent Performance Trajectory

Argan Inc’s fiscal year ending January 31, 2026 marked a decisive inflection point characterized by sharp financial improvement compared to the prior three years [F1]. Operating income rocketed by approximately 53% YoY to $134.7 million, while net income increased by over 61% to nearly $137.8 million. These gains track closely with expanding operations in the Power segment—the company’s largest revenue contributor [S1]. Even more striking was the operating cash flow surge by nearly 150%, reaching $414.7 million, fueled by progress billings and project execution efficiencies inherent in fixed-price EPC contract models.

This step change extends beyond pure top-line expansion; it reflects an operational gearing effect as large utility-scale projects ramped up amidst broader construction industry cyclicality. The prior fiscal years displayed more moderate growth patterns but with episodic earnings volatility attributable to timing variation of Notices to Proceed (NTPs) on multi-year contracts [S1]. Notably, capex dropped substantially (-41%) reflecting limited equipment investment needs relative to cash generation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 138 | 415 | 135 | 4 | +61.2% |

| 2025 | 85 | 168 | 88 | 7 | +164.1% |

| 2024 | 32 | 117 | 36 | 3 | -2.2% |

| 2023 | 33 | -30 | 42 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 10 | 411 | 29.8 |

| 2025 | 2 | 161 | 24.3 |

| 2024 | 12 | 114 | 11.1 |

| 2023 | 68 | -33 | 11.8 |

Source: SEC companyfacts cache [F1].

Table: Argan Inc Historical Financial Performance Summary (FY2023 to FY2026)

Unpacking Power Segment’s Dominance and Multi-Geographic Reach

The Power segment consistently represents over eighty percent of consolidated revenues—80.1%, 79.3%, and 72.6% for fiscal years ending January ‘26 through ‘24 respectively [S1],[S5]. This business unit specializes in full turnkey EPC services for natural gas-fired combined-cycle plants alongside renewable energy installations such as solar fields (including battery storage), biomass plants, wind farms, and biofuel facilities [S18],[S20]. Its client base is concentrated among independent power producers, utilities, equipment suppliers, with projects spanning the U.S., United Kingdom, and Ireland.

Project lifecycles typically range from one to four years and are executed predominantly under fixed-price EPC contracts utilizing progress billing methods keyed to costs incurred—a accounting approach conducive to revenue recognition over time [S1],[S21]. Importantly, receipt of full notices-to-proceed governs the commencement of revenue recognition from awarded projects—a critical liquidity inflection for the firm given sizable backlog [N1],[N3].

Though competition has thinned among domestic large gas-fired plant contractors due to market exits and acquisitions, this dynamic may invite resurgence or new entrants attracted by improving spark spreads—highlighting ongoing market vigilance requirements for Argan [S18],[S24]. Additionally, international operations involve complex turbine/boiler commissioning and outage services for major utilities’ power stations in Ireland and the UK—adding considerable geopolitical regulatory overlay underwriting risk.

Industrial and Teledata Segments: Diversification Supporting Stability

While smaller than Power in scale, Argan’s Industrial ($167+ million annually recently) and Teledata ($20+ million) segments extend geographic coverage into the Southeastern US industrial construction arena and Mid-Atlantic telecommunication infrastructure space respectively [S5],[S12],[S13].

The Industrial segment provides onsite fabrication including piping systems & pressure vessels plus field services supporting maintenance turnarounds—serving diversified industries such as aluminum recycling, data centers, EV manufacturing, fertilizer production, pulp & paper, water treatment plants [S5]. The holding company model allows these subsidiaries substantial operational autonomy providing agile responses tailored to their local market dynamics even while benefiting from centralized strategic oversight.

Teledata focuses on technology wiring solutions including underground conduit installation using trenchless directional boring techniques along with high/low voltage line setups servicing commercial/government sectors [S13]. Despite operating within fragmented competitive markets populated by both regional specialists and national firms, Teledata leverages security-cleared personnel and long-term contractual relationships for stable order intake.

Navigating Supply Chain and Labor Constraints in Construction Services

Argan faces persistent challenges typical of mid-sized EPC contractors operating in volatile commodity markets subject to supply chain disruptions affecting critical structural steel, piping materials, vessel components, specialty equipment delivery timelines—and fluctuating subcontractor pricing due to skilled craft labor scarcity [S16],[S24]. Recent tariff-related import restrictions have elevated material costs uncertainties requiring proactive procurement strategies like early upfront purchasing on lump sum contracts [S18].

Labor availability constraints particularly impact scheduling flexibility during peak industrial construction cycles increasing risk premiums embedded in project bids or necessitating supplemental use of temporary workers/subcontractors adding operational complexity around productivity metrics [S15]. Despite these headwinds Argan maintains OSHA reportable incident rates considerably below industry averages demonstrating effective safety culture that supports workforce retention helping mitigate scheduling risks [S4],[S15].

Backlog Visibility and Project Pipeline: What Lies Ahead?

The company disclosed remaining unsatisfied performance obligations (RUPO) approximating $3 billion as of late fiscal ’25 quarter end representing significant multi-year work-in-hand—a strong indicator of future revenue streams assuming timely Notices-to-Proceed are received per contract milestones [S19],[N3]. Approximately eight percent of RUPO is expected to convert into revenue during the remainder of fiscal ’26 indicating sustained progress billing inflows.[S19]

Backlog pacing strongly influences quarterly earnings variability given reliance on a handful of large projects’ start/completion timing [S1]. Thus awards cadence announcements or NTP issuances serve as leading indicators for earnings trajectory—which investors keenly monitor amid cyclical macro pressures affecting capital expenditure plans downstream.

Capital Allocation Priorities: Buybacks, Dividends, and Liquidity Positioning

Argan deploys capital conservatively emphasizing shareholder returns balanced against liquidity needs arising from large project working capital demand fluctuations [F1],[S27]. FY2026 repurchases totaled approximately $9.9 million versus just $1.5 million prior year—a modest step-up reflecting prudent deployment without excessive leverage given no outstanding borrowings under bank facilities although letters of credit support bonding capacity totaling tens of millions [S4],[S15]. Dividend payment policies were consistent though not detailed explicitly.

Cash & equivalents stood robust at $339 million marking a sizable buffer for anticipated contract asset funding cycles while maintaining positive covenant compliance under revolving credit agreements secured by company assets valued above $1 billion total [F1],[S4],[S15]. Low capex requirements underscore free cash flow generation strength (> $400M) which underwrites financial flexibility needed for opportunistic acquisitions or unexpected claim settlements.[F1],[S27]

Financial Health through Key Metrics: ROE, Cash Flows, and Balance Sheet Strength

Return on equity approached an impressive ~30% in FY2026 reflecting effective profitability enhancement alongside steadily strengthening equity base reflective of retained earnings growth from expanding net income [F1]. Operating cash flow swing from negative territory three years ago into a four-hundred-million-dollar inflow underscores operational execution quality especially managing working capital amid fluctuating project schedules.[F1]

Balance sheet metrics reveal current assets exceeding current liabilities by a factor close to 1.59x evidencing short-term liquidity adequacy crucial for navigating bond-backed contractual performance obligations estimated near half a billion dollars including warranty reserves.[F1],[S4]

Regulatory and Contractual Risks Impact on Margins and Execution

Major ongoing legal proceedings involve a significant project terminated due to owner breaches that triggered a drawdown on a $10 million irrevocable letter of credit/bond issued by Argan’s UK subsidiary—with disputed claims between parties adding complexity around accounts receivable realization risk [S1],[S17],[S28]. Such bond recalls represent contingent liabilities potentially impacting margin transparency for affected projects.

Contractual performance bonds remain core risk mitigants yet introduce potential financial strain if disputes escalate requiring reserve set-asides or litigation expenses.[S17] Anti-bribery law compliance across multinational jurisdictions further layers reputational risk exposure necessitating rigorous policies given complex subcontractor networks pervasive in this sector.[S24]

Milestones To Watch: Contract Awards, Notice-to-Proceed Timing, and Market Signals

Investor focus will center on timely awarding of new EPC contracts especially within regulated utility sectors benefiting from favorable electricity market fundamentals including improving spark spreads influencing development economics once again after intermittent softness.[N3] JP Morgan upgrade signals bullish institutional interest reaffirming expectations around backlog conversion efficiency post Q4 release.[N11]

Close monitoring of notices-to-proceed—the pivotal trigger advancing revenue recognition—is necessary given their outsized influence on quarterly results volatility.[N3] Developments surrounding unresolved overseas project counterclaims could materially affect noncurrent receivable recoverability.[N14] Sector-wide labor cost inflation trends alongside global supply chain normalization will also shape operating margin outcomes going forward.

This analysis synthesizes Argan Inc's intricate engineering procurement construction business model supported by detailed SEC filings supplemented with recent news insights reflecting its multi-segment operational complexity across geographies tempered by inherent industry cyclicality risks without making investment recommendations or forecasts beyond explicit disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments