ROBO.AI INC. Faces Strategic Transition and Liquidity Challenges Post 2025 Fiscal Year

Following a steep revenue decline and heavy operating losses in 2025, Robo.ai is restructuring its business model, focusing on strategic acquisitions and smart mobility in emerging markets while contending with significant liquidity constraints.

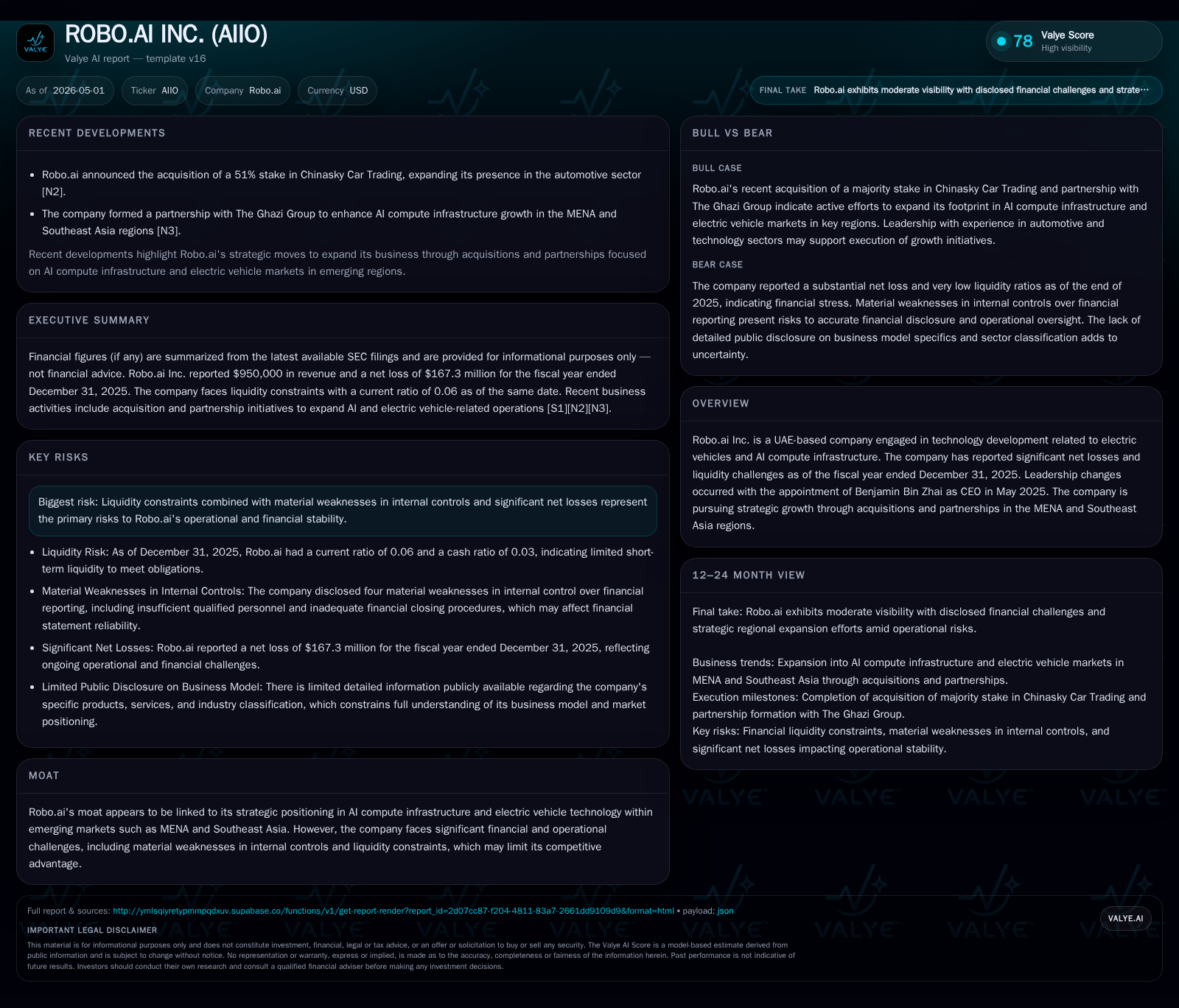

Robo.ai Inc.'s latest filings reveal deep financial strain marked by a drastic 92% revenue fall and persistent operating losses totaling $157 million in 2025. The company is pivoting from vehicle manufacturing towards AI compute infrastructure and smart mobility solutions, especially targeting MENA and Southeast Asia markets through partnerships and acquisitions. Despite these strategic moves, serious liquidity challenges and internal control weaknesses threaten its operational stability. Monitoring execution progress on key acquisitions and managing financial risks will be crucial for Robo.ai's future path.

Recent Operating Update

Robo.ai Inc.'s most recent quarterly filing dated April 1, 2026 [S2] confirms the company continues to file under Form 20-F, signifying ongoing compliance with SEC reporting standards. No new annual or quarterly revenues were disclosed beyond those reported in the December 31, 2025 fiscal year results [S1], which show a dramatic revenue collapse from $12 million in 2024 to just $950,000 in 2025 [F1]. This reflects the consequences of the company's strategic transformation that entailed discontinuation of vehicle lines like Rabdan and intensified market competition.

Furthermore, an important corporate development was the February 2026 acquisition of a controlling stake (51%) in Chinasky Car Trading FZE [S3], a Dubai-based automotive trading firm. This acquisition complements Robo.ai's shift toward an asset-light model emphasizing smart mobility solutions by providing access to a global distribution and logistics network spanning multiple emerging regions including MENA and parts of Eurasia. Post-closing cooperation agreements also aim to extend into automobile leasing, after-sales service, accessory sales, and insurance collaborations.

Leadership transitioned with Benjamin Bin Zhai assuming CEO responsibilities in May 2025, signaling management's commitment to steer Robo.ai through its restructuring phase.

Business Model

Robo.ai traditionally generated revenue principally from sales of smart electric vehicles alongside automotive parts and materials [S1]. However, since the cessation of its Rabdan-branded vehicle line amid intense competition from major EV players like Tesla, Lucid, NIO, and incumbents pivoting into EVs, revenue has cratered. The diminished top-line has pivoted the business model toward integrating AI technologies into smart city infrastructure and AI-powered mobility platforms rather than direct vehicle manufacturing.

The company expenses all research and development costs as incurred to focus on innovation within intelligent operating systems embedded in their hardware products [S1]. Their MUSE platform incorporates AI-NAS systems with cybersecurity features designed to isolate entertainment systems from vehicle control units—a critical safety differentiator [S1]. Adding value through intellectual property rights protection plays a growing role; Robo.ai has transferred over 60 patent rights to its Dubai HQ as part of an asset-light approach centered on technology licensing rather than capital-intensive manufacturing footprint expansion.

Ancillary revenue streams are being developed via acquisition targets such as Chinasky Car Trading FZE which provide established distribution hubs alongside capabilities for automobile leasing and after-sales services [S3]. These lines promise recurring revenue with less capital investment but require effective integration and expansion.

Industry Structure and Competitive Position

Robo.ai operates at the confluence of electric vehicles (EVs), artificial intelligence applications for mobility, and smart city ecosystems—sectors dominated by well-capitalized OEMs as well as increasingly sophisticated technology firms. The competitive moat appears limited due to heavy incumbency advantages held by established global automotive brands expanding their EV portfolios aggressively. Moreover, Tesla’s advanced battery tech and autonomous driving software set high benchmarks.

Regionally focused strategies targeting MENA and Southeast Asia leverage lower saturation levels for smart mobility adoption but also face challenges from local regulations, variable infrastructure maturity levels, and fluctuating economic growth projections. Robo.ai’s asset-light model potentially allows quicker adaptability but lacks scale economies when compared against legacy manufacturers with global production networks.

Furthermore, continued material weaknesses flagged in internal controls over financial reporting complicate operational risks by potentially hindering accurate data-driven decisions or investor confidence [S12][S23].

Growth Drivers

Strategic expansion into partnership-led regional marketplaces remains central. The acquisition of Chinasky Car Trading FZE is particularly notable for enabling access to cross-border trade corridors spanning Middle East through North Africa into Eastern Europe—regions poised for gradual electrification but underserved by international EV rollouts so far.

Robo.ai’s research investment into AI-driven navigation & safety systems embedded within its product suite positions it well amid rising demand for autonomous features globally despite incremental regulatory hurdles.

Emerging trends around integrated smart city solutions combining mobility-as-a-service (MaaS) concepts could provide durable revenue if successfully capitalized on through platform ecosystems integrating hardware (vehicles), software (AI), logistics (distribution network), and services (leasing & maintenance).

Recurring revenue potential from aftermarket services including insurance cooperation projects further enhances customer lifetime value metrics over pure hardware sales [S3].

Risks / Watchpoints / Growth Constraints

Operating losses are persistently high—$157 million recorded in FY25—and net income was similarly negative at $167 million despite non-cash expense adjustments largely related to share-based compensation [F1][S1][S15]. This indicates ongoing cash burn absent material operational improvements or capital inflows.

Material weaknesses identified within internal controls pose compliance risks that could impact audit quality or regulatory scrutiny outcomes if not remedied expeditiously [S12][S23].

Unresolved litigation related issues including a notable dispute involving Tianjin Yizhong Jinshajiang Equity Investment Fund add further downside risks given potential contingent liabilities [S25]. Foreign currency risk is also non-trivial given multi-jurisdictional operations across RMB-, AED-, EUR-denominated markets with USD functional currency reporting exposure [S23].

Availability of committed credit lines or equity funding is conditional on external factors such as market conditions making liquidity uncertain despite announced facilities that could total up to $180 million via PIPE investors [S6][S14]. Execution risk remains significant for planned strategic initiatives including integration of acquisitions.

What to Watch Next

- Progress towards closing any additional tranches or draws under recently arranged equity purchase facility ($100 million) or convertible note facility ($80 million) will be critical liquidity milestones [S6][S14].

- Development of new business lines stemming from Chinasky Car Trading FZE acquisition such as automobile leasing contracts, after-sales service agreements, and insurance partnerships will signal diversification success or struggle [S3].

- Improvement or remediation status regarding material internal control weaknesses will be closely watched by auditors and regulators impacting future compliance costs or investor confidence [S12][S23].

- KPIs around shipments or volume growth for smart EV platforms tied to AI compute infrastructure may reveal early traction amidst company’s strategic transformation efforts.

- Monitoring gross margin improvement reflecting product mix shift towards higher-margin software/AI services vs hardware manufacturing will provide insight into sustainability of business model evolution.

- Resolution outcomes on pending legal proceedings such as Yizhong debt/arbitration disputes will affect contingent liability exposure flagged in reports [S25].

- Changes in competitive landscape with moves by legacy OEMs entering targeted regional markets could alter addressable market opportunity dynamics further.

Financial Profile Brief Context

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $4mm | |

| 2025-12-31 | ||

| Total debt | $123000 | |

| 2025-12-31 | ||

| Net debt | $-4mm | |

| 2025-12-31 | ||

| Current assets | $8mm | |

| 2025-12-31 | ||

| Current liabilities | $125mm | |

| 2025-12-31 | ||

| Current ratio | 0.06x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Liquidity is under severe pressure: cash stands barely above $4 million while curves steeply negative working capital leads to a current ratio near one-twentieth standard coverage thresholds at best (0.06) indicating near insolvency risk if financing woes are not resolved swiftly [F1]. Total debt remains modest relative to cash but covenant details around PIPE investor arrangements introduce complexity around capital structure management [F1][S6][S14].

In conclusion, while Robo.ai’s repositioning toward AI-enabled intelligent mobility solutions aligns with secular industry trends favoring electrification combined with digitalization efforts especially within underpenetrated emerging markets represents structural upside potential—the company confronts substantial near-term operational execution obstacles compounded by fragile liquidity profiles that must be addressed decisively.

Disclaimer: This analysis is based solely on public SEC filings up to April 30, 2026 ([S1]-[S29]) combined with Companyfacts data snapshot as of December 31, 2025 ([F1]). It does not constitute investment advice or recommendations but provides an independent industry perspective anchored on verified disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments