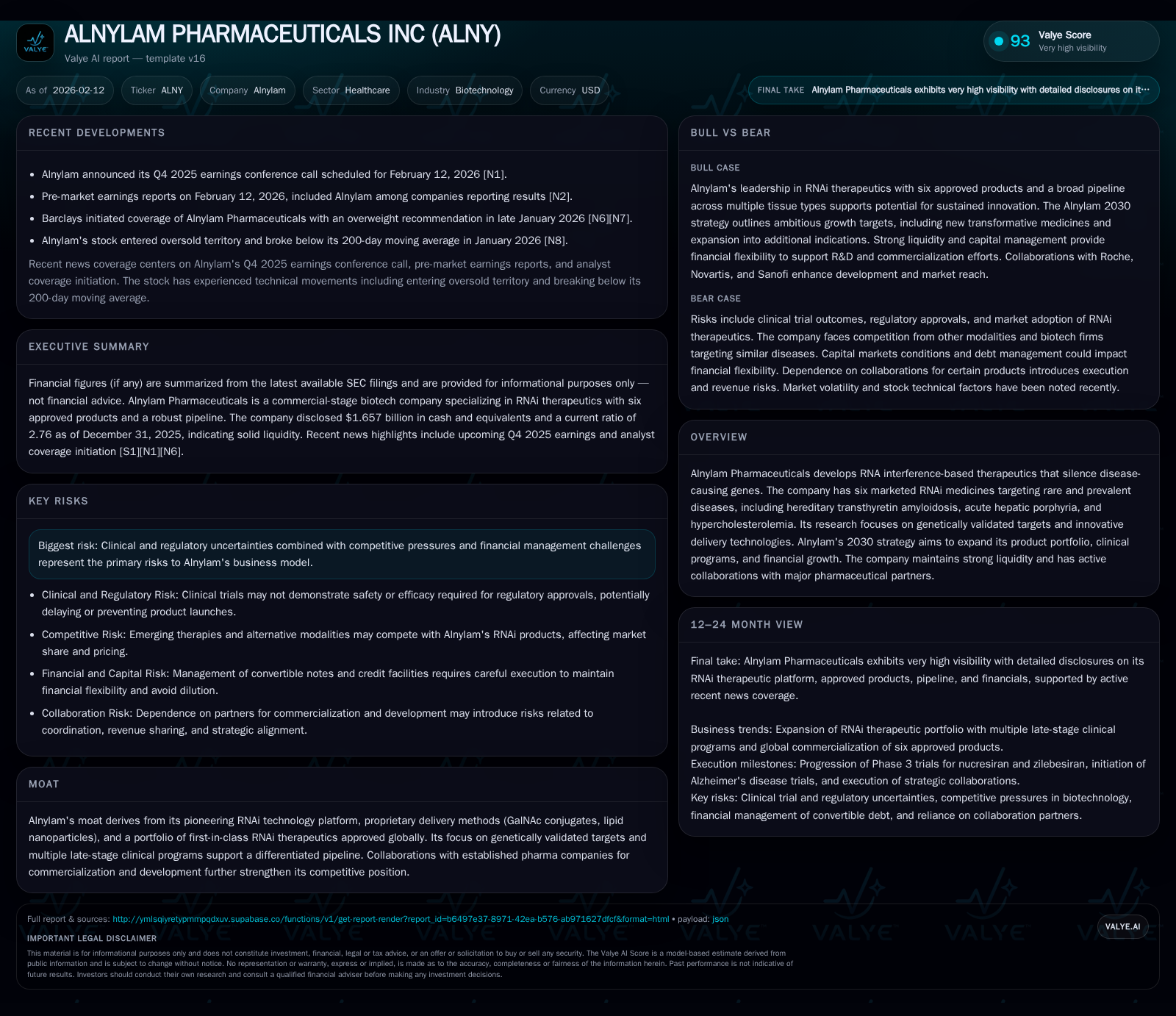

Alnylam Pharmaceuticals: RNAi Pioneer Advancing Transformative Therapeutics with Strategic Growth Ambitions

Alnylam Pharmaceuticals leads the RNA interference therapeutics field with six marketed products and a visionary 2030 strategy to expand its impact across multiple diseases and tissues.

Alnylam Pharmaceuticals has established a durable competitive edge as the pioneer in RNA interference (RNAi) therapeutics, leveraging proprietary delivery technologies to commercialize six first-in-class RNAi-based medicines. The company’s 2030 strategic plan underscores aggressive growth targets encompassing portfolio expansion beyond transthyretin amyloidosis, scaling of clinical programs across diverse tissue types, and sustained financial performance including double-digit revenue CAGR and strong operating margins. Despite risks related to regulatory hurdles, clinical uncertainties, and market competition, Alnylam benefits from robust liquidity, ongoing collaborations, and a growing global footprint underpinning its next wave of innovation and commercialization.

Company Overview and Technology Platform

Founded as a pioneer in harnessing RNA interference (RNAi) biology, Alnylam Pharmaceuticals operates at the forefront of gene silencing therapeutics. Its approach utilizes small interfering RNAs (siRNAs) to degrade messenger RNAs that encode pathogenic proteins—targeting diseases at their genetic root rather than symptomatically modulating protein activity. This mechanism positions Alnylam’s RNAi medicines upstream of conventional drug classes such as small molecules or antibodies.

Central to Alnylam’s technological moat are its proprietary delivery platforms. These include N-acetylgalactosamine (GalNAc) conjugates that facilitate efficient hepatocyte targeting via asialoglycoprotein receptors, principal drivers for liver-directed diseases like hereditary transthyretin amyloidosis (hATTR), acute hepatic porphyria, and hypercholesterolemia. Complementing this are lipid nanoparticle formulations enabling systemic siRNA distribution. The company is actively expanding these capabilities to reach the central nervous system (CNS) via alternative conjugates (e.g., C16 moieties), ocular tissues, skeletal muscle, heart, and adipose tissue—addressing therapeutic areas marked by high unmet need.

Marketed Portfolio and Clinical Pipeline

As of early 2026, Alnylam boasts six approved RNAi therapeutic products globally: AMVUTTRA™ (vutrisiran), ONPATTRO™ (patisiran), GIVLAARI™ (givosiran), OXLUMO™ (lumasiran), Leqvio™ (inclisiran), and Qfitlia™ (fitusiran). These medicines collectively treat genetically validated conditions ranging from rare hereditary amyloidosis forms to more common cardiovascular indications such as hypercholesterolemia. Several are marketed directly by Alnylam or through collaborations with major pharma partners enhancing their commercial penetration.

Alnylam’s robust clinical pipeline includes more than 20 active programs across various phases. Late-stage studies particularly focus on next-generation silencer nucresiran for ATTR amyloidosis polyneuropathy (anticipated launch by 2028) and cardiomyopathy indications targeted for 2030. Beyond TTR diseases, ambitions extend to delivering multiple blockbuster candidates aimed at preventing or reversing disease progression—signaling diversification beyond its traditional hepatic disease base.

Strategic Vision: Alnylam 2030

The recently articulated Alnylam 2030 strategy crystallizes the company’s medium-to-long term objectives:

- Global TTR Leadership: Cementing market leadership in transthyretin-related amyloidosis through existing franchises and upcoming launches.

- Sustainable Innovation: Delivering two or more transformative new medicines beyond TTR with the potential for blockbuster status.

- Tissue Expansion: Targeting over 10 tissue types within more than 40 clinical programs to broaden therapeutic reach.

- Financial Performance: Achieving compounded annual revenue growth exceeding 25% alongside non-GAAP operating margins around 30%, underpinning profitable scale.

- Investment in R&D: Committing circa 30% of revenues toward research and development expenditures ensuring a continuous pipeline flow.

This ambitious roadmap reflects integration of internal innovation acceleration plus selective external partnerships to complement the discovery engine.

Financial Health and Operational Metrics

According to the recently filed SEC Form 10-K for fiscal year ending December 31, 2025 [S1], Alnylam closed the year with approximately $1.66 billion in cash and equivalents, supporting strong liquidity positions essential for ongoing R&D investments and global commercial infrastructure buildup. The current ratio stood at a healthy ~2.76 indicating adequate short-term asset coverage against liabilities.

The reported net income was $314 million for 2025 [F1], illustrating maturing operations compared to earlier years when losses were commonplace—a positive signal although past history demands cautious optimism given typical biotechnology sector volatility.

Revenue streams continue primarily driven by AMVUTTRA sales alongside partner-derived revenues from collaboration agreements. With commercialization efforts expanding internationally including EU, UK, Japan, and others markets, top-line momentum aligns with corporate growth aspirations.

Competitive Positioning and Moat

Alnylam’s differentiated technology platform represents a high barrier to entry among competitors attempting to replicate effective siRNA delivery mechanisms—particularly regarding GalNAc conjugation chemistry which has become an industry benchmark. Its portfolio of globally approved RNAi drugs confirms regulatory acceptance of its approach—an advantage not easily replicated by emerging biotech peers or traditional pharmaceutical companies venturing into genetic medicines.

Collaborations with pharma heavyweights provide commercial scale advantages—for instance through co-promotion or license agreements—which bolster market reach especially in territories requiring local expertise. This network also diffuses risk associated with single-product exposure.

Industry Dynamics and Risk Considerations

Despite promising fundamentals, inherent risks remain prominent:

- Regulatory uncertainties surrounding novel gene silencing modalities can delay approvals or impose stricter post-marketing requirements.

- Clinical development failures—even late stage—pose material setback potential given reliance on genetically validated but complex disease mechanisms.

- Pricing pressures from healthcare payers coupled with reimbursement challenges may affect market uptake especially in cost-sensitive regions.

- Dependence on third-party manufacturers for some product supply chains introduces operational vulnerabilities.

- Talent retention essential to sustaining innovative edge across disciplines remains an ongoing management imperative [S1].

Recent News Highlights and Market Sentiment

In anticipation of Q4 earnings announced on February 12, 2026 ([N1],[N7]), market commentary underscored expectations for continued revenue growth driven by AMVUTTRA adoption enhancements as well as updates on late-stage pipeline candidates ([N4]). Analysts highlighted confidence rooted in Alnylam’s strategic blueprint yet cautioned vigilance over macroeconomic conditions influencing biotech valuations ([N8],[N13]). Barclays initiation coverage mid-January favored overweight positioning reflecting conviction in durable franchise economics ([N9],[N10]).

Conclusion: A Forward-Looking Perspective Without Investment Advice

Alnylam Pharmaceuticals stands as a pioneering force within the evolving landscape of RNAi therapeutics—a domain promising profound shifts in treating genetic disorders through fundamental gene expression modulation rather than conventional pharmacology paradigms. The combination of validated delivery technologies, an expanding suite of approved drugs addressing both rare and common conditions, strategic growth plans emphasizing diversification into multiple tissues/disease areas, and sound financial footing present a compelling narrative for stakeholders tracking innovation-driven biopharma enterprises.

However, navigating typical biotech sector complexities such as clinical trial rigor, regulatory gatekeeping, competitive innovation churn, pricing pressures, manufacturing scalability issues, and talent retention concerns must remain central considerations when analyzing company trajectory beyond headline growth figures.

This memo aims to inform internal stakeholders about the critical facets shaping Alnylam’s business dynamics as it progresses through its notable transformation journey over the coming decade.

This document is intended solely for informational purposes based on publicly available information as of February 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments