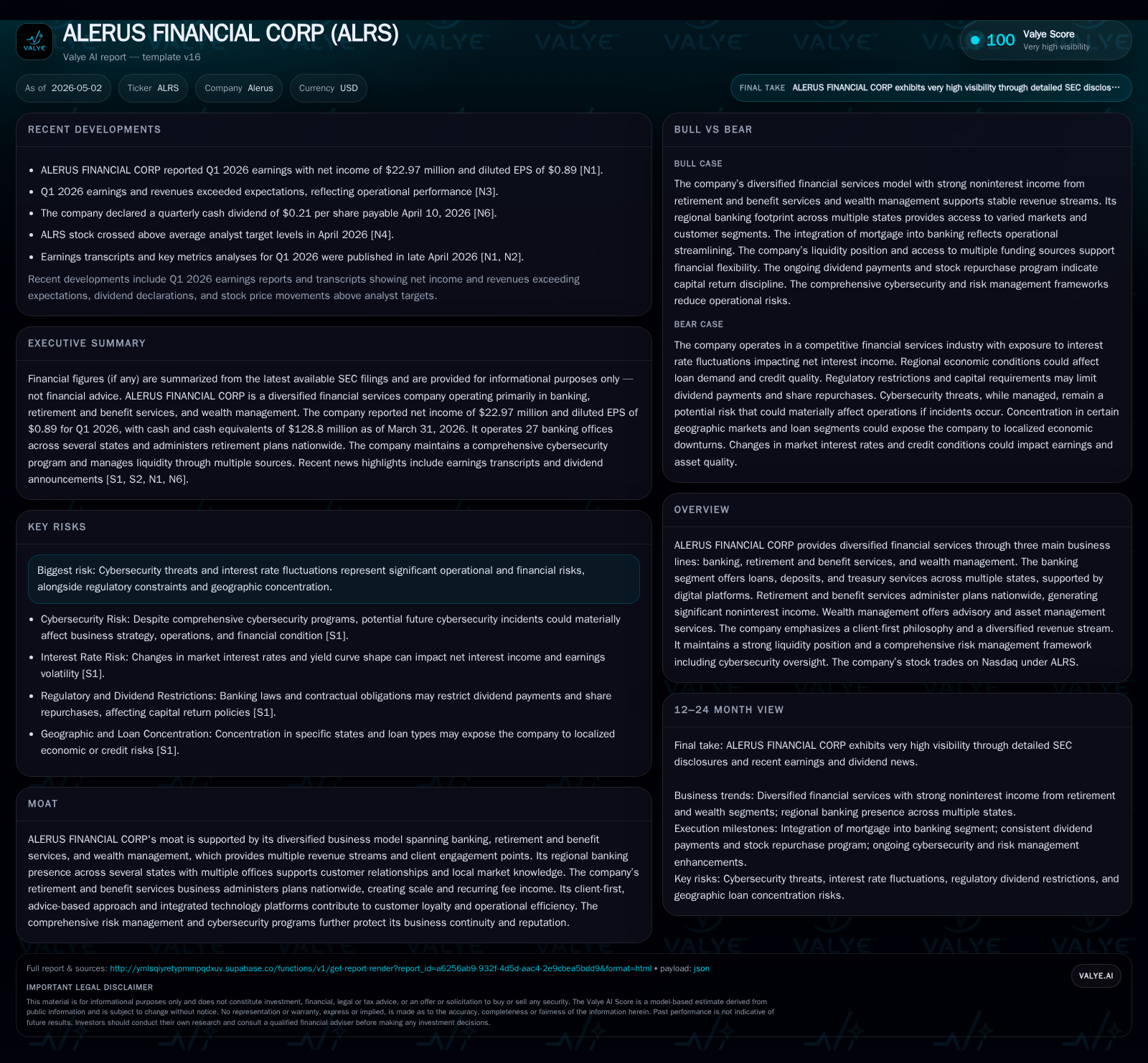

ALERUS FINANCIAL CORP Strengthens Diversification with Solid Q1 Execution and Risk Controls

ALERUS reported stable first-quarter results reflecting disciplined credit risk management, diversified revenue streams, and robust liquidity.

In its latest 10-Q filing for Q1 2026, ALERUS Financial Corp highlighted refined collateral practices around customer loan swaps and reclassification of derivative instruments that streamline income statement presentation. Its three-pronged business model—banking, retirement and benefit services, and wealth management—provides complementary revenue drivers supported by a client-first philosophy and integrated digital platforms. While regional banking competitive dynamics and regulatory capital requirements shape its operational landscape, continued expansion of retirement plan administration fees and technology-enabled wealth advisory services underpin growth. Key risks include cybersecurity threats, interest rate volatility, and regulatory constraints. ALERUS maintains a strong liquidity position with net cash exceeding $69 million as of March 31, 2026.

Quarterly Operating Update Highlights

ALERUS Financial Corp's Q1 2026 disclosures emphasize nuanced improvements in derivative instrument management and credit risk calibration. The company maintains master netting agreements with counterparties for all interest rate swaps, settling collateral on a net basis which simplifies the recognition of related cash flows. This has led to reclassification of derivative-related amounts into the interest expense line on short-term borrowings within the consolidated statements of income [S2]. Derivative assets are recognized under other assets while derivative liabilities are included within accrued expenses and other liabilities on the balance sheet, enhancing transparency.

Additionally, the reported credit loss expense includes discrete components: a $31 thousand expense tied to off-balance sheet credit exposure and a $76 thousand charge related to held-to-maturity investment securities. These minor but explicit disclosures highlight ALERUS’s diligent credit risk monitoring practices extending beyond on-balance-sheet loan portfolios. The company also confirms that it actively manages net exposure on customer loan swaps by obtaining collateral per standard underwriting policies but does not post collateral to customers itself—this asymmetric collateral policy reflects prudent risk containment without burdening clients [S2].

Furthermore, tax effects related to low income housing tax credits are incorporated into income tax expense rather than operating expenses or tax benefits directly impacting earnings lines [S2]. Together these details indicate ongoing refinement in accounting classification and enhanced risk oversight pertinent to ALERUS’s diverse financial activities.

Business Model and Product Portfolio Analysis

ALERUS operates a diversified financial services business anchored by three segments: banking; retirement and benefit services; and wealth management [S1]. The banking segment operates regionally across multiple states providing traditional services such as commercial loans (including real estate development financing), consumer deposits, mortgage lending, and treasury management solutions. Its regional footprint facilitates leveraging local market knowledge to foster client relationships while offering scale economies primarily through digital banking platforms.

The retirement and benefit services business administers employer-sponsored retirement plans nationwide encompassing defined contribution plans like 401(k)s along with other employee benefit packages. This segment generates substantial noninterest income from recurring fees tied to plan administration assets under management. The national scope allows scaling cost structures benefiting margin profiles while diversifying fee revenue streams away from interest rate sensitivity.

Wealth management complements the portfolio by delivering personalized financial advisory services alongside asset management solutions focusing on high-net-worth individuals and institutional clients. Emphasizing client-centric advice over transactional sales supports retention amid competitive wealth advisory markets.

Together with an integrated technology infrastructure facilitating unified client servicing across these divisions, ALERUS’s client-first philosophy drives ecosystem stickiness. Switching costs arise from entrenched plan administration contracts combined with advisory relationships augmented by digital tools enabling seamless access to account information.

Competitive Positioning within Regional Financial Services

Within the regional banking arena where ALERUS competes, scale is moderate relative to larger national or super-regional banks, limiting pricing power especially on commercial loan spreads amid intense competition for creditsensitive borrowers [S1]. However, multiple physical office locations combined with deep local market penetration foster trusted relationships shielding some margin compression risks.

On the regulatory front, the company’s bank subsidiary operates under a national charter regulated by the OCC with FDIC insurance compliance. It maintains "well capitalized" status allowing utilizing brokered deposits up to 20 percent of total assets—this flexibility is crucial for funding diversified loan portfolios without excessive reliance on expensive wholesale borrowing sources [S4],[S7],[S29].

Pricing discipline is influenced by industry-wide capital requirements which dictate maintaining sufficient Tier 1 capital ratios limiting leverage growth but ensuring strong loss-absorbing buffers in macroeconomic uncertainty. Further constraints come from geographic concentration risks inherent in a primarily Midwestern focus.

The synergy among banking deposits fueling retirement plan fee income and wealth management asset bases differentiates ALERUS from pure-play banks or asset managers alone—this integrated model promotes cross-selling efficiencies though scale limitations may cap rapid breakout growth.

Key Growth Engines: Diversification and Technology Integration

Growth drivers at ALERUS are anchored in expanding its noninterest income streams predominantly through increased retirement plan assets under administration nationwide—a structural tailwind given demographic shifts favoring defined contribution plans expanding participant populations [N2],[N3].

Technology integration is another pillar enabling scalable client onboarding as well as servicing automation across all segments reducing per-client cost overruns observed in legacy models. Enhanced digital platforms improve client engagement metrics bolstering advisory retention rates within wealth management while supporting treasury services innovation applicable in banking segment treasury offerings.

Cross-selling opportunities also present upside; securing corporate clients for benefit services increases potential deposit inflows plus investment advisory relationships placing fee-based assets under management adding margin diversity helping offset cyclical loan demand fluctuations.

Rising interest rates have bolstered deposit margins positively affecting treasury services revenues underpinning near-term top-line growth alongside steady loan demand grounded in commercial real estate construction and owner-occupied commercial loans assessed conservatively during origination processes [N2],[S28].

Risks and Constraints: Cybersecurity, Interest Rates, and Regulation

ALERUS identifies cybersecurity as a material operational risk mitigated through comprehensive frameworks involving continuous vulnerability assessments conducted by an experienced internal cybersecurity team led by a director with over three decades in information security [S1]. Oversight extends to board-level Risk Committee reviews incorporating third-party audits ensuring proactive threat identification though residual risk remains from increasingly sophisticated external attacks potentially impairing operations or damaging reputation.

Interest rate volatility represents both an opportunity and threat affecting net interest margins depending on asset-liability re-pricing mismatches despite ALCO’s active monitoring aimed at smoothing earnings variability stemming from market cycles or policy shifts [S16],[S7].

Regulatory constraints—including limits on brokered deposits relative to asset size—and evolving capital adequacy standards necessitate ongoing compliance investment restricting rapid balance sheet expansion thus constraining faster growth trajectories typically favored in larger peers’ models [S4],[S29]. Geographic concentration primarily within Northern Plains states further exposes loan portfolios to localized economic downturns amplifying credit loss risk requiring sustained conservative underwriting prudence.

Upcoming Milestones and Monitoring Points

Investors should closely observe ALERUS's next quarterly results for guidance refinements regarding earnings trends versus consensus estimates particularly focusing on core wealth management asset flows alongside retirement plan participant expansion metrics which serve as proxies for recurring noninterest income stability [N3],[N1].

Monitoring loan portfolio growth vis-à-vis deposit stability will be critical signaling ability to fund expansion organically without degrading liquidity cushions maintained robustly currently [S2],[F1]. Technology deployment success measured via customer adoption rates of enhanced digital advisory tools may provide leading indicators of future margin improvements especially if wealth and retirement segments gain share from traditional incumbents.

Additional attention warranted toward impact of any changes in regulatory frameworks potentially affecting brokered deposit capacity or capital thresholds influencing strategic flexibility.[S16]

Financial Profile and Latest Balance Sheet Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $129mm | |

| 2026-03-31 | ||

| Total debt | $59mm | |

| 2026-03-31 | ||

| Net debt | $-70mm | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, ALERUS held $128.8 million in cash & equivalents against $59.2 million of total debt yielding a net cash position approximating $69.6 million which affords substantial liquidity buffer supporting operational resilience amid macroeconomic fluctuations [F1],[S2],[S29].

Balance sheet allocations reflect disciplined leverage consistent with regulatory well-capitalized designation facilitating access to brokered deposits up to prescribed limits while maintaining robust contingency funding plans administered through an active Asset Liability Committee (ALCO) comprehensively overseeing liquidity needs aligned with growth initiatives.[S4]

This strong financial footing complements ALERUS’s strategy focused on sustainable diversified revenue sources coupled with effective credit loss management evidenced by modest credit loss components detailed explicitly in recent filings signifying prudent provisioning methodologies.[S2]

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 128,826,000 |

| Total Debt | 59,211,000 |

| Net Debt | -69,615,000 |

This analysis draws exclusively from verified SEC filings including the latest quarterly report (10-Q), recent event disclosures (8-K), annual filings (10-K), supplemented by current financial snapshot data ensuring discipline in factual representation without speculative forecasts or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments