DexCom’s Q1 Momentum Highlights Market Leadership in Continuous Glucose Monitoring

DexCom’s strong first-quarter results underscore its dominant position and innovation trajectory within the CGM market.

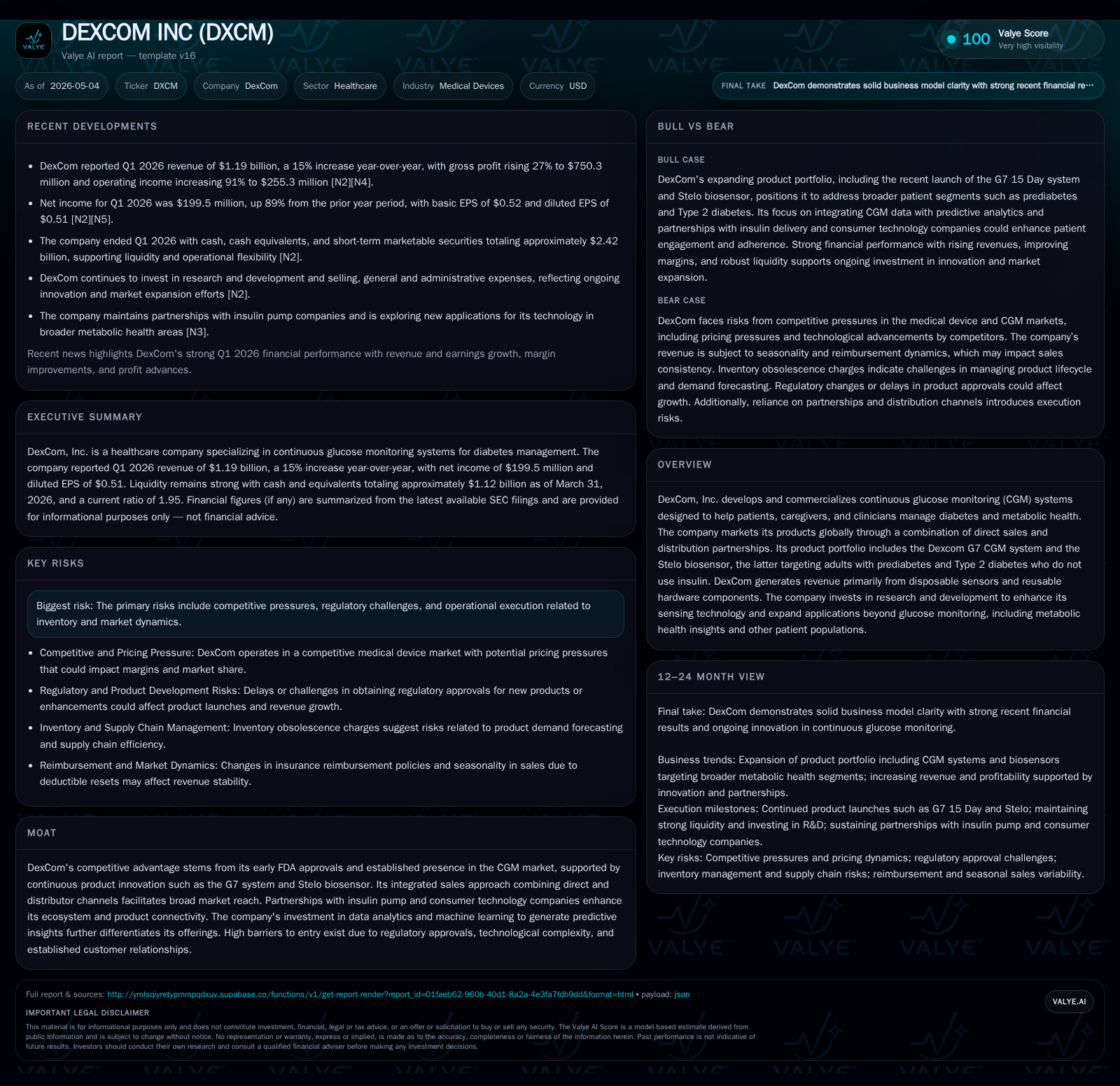

In Q1 2026, DexCom demonstrated resilient revenue growth despite typical seasonal softening due to U.S. insurance deductible resets, driven by robust sensor sales and expanding customer adoption. The company’s core business model centers on recurring disposable sensor sales paired with reusable hardware, leveraging technological leadership in continuous glucose monitoring systems such as the G7 and Stelo biosensor. DexCom maintains a commanding competitive stance supported by early FDA approvals, integrated sales channels, and data-driven product innovation while actively pursuing growth beyond insulin-dependent diabetes. Key risks include intensifying competition, regulatory complexities, and supply chain management. Near-term milestones to watch include reimbursement trends for new product lines and expansion of CGM use into broader metabolic health applications.

Q1 2026 Operating Update: Revenue Strength Despite Seasonality

DexCom reported first-quarter 2026 revenue of $1.19 billion, reflecting an encouraging 15% increase over Q1 2025 despite typical seasonal softness associated with annual U.S. insurance deductible resets and depleted flexible spending accounts affecting end-user purchasing power in early calendar quarters [S2]. This seasonality is a recurrent theme as patients often delay replenishment until deductibles reset in subsequent quarters.

The company’s revenues are segmented into sales of disposable glucose sensors and reusable hardware components — primarily transmitters and receivers — which together compose its singular business segment managed on a global consolidated basis. The U.S. market continues as the dominant geographic contributor reflecting entrenched payer relationships and direct sales coverage [S2,S10].

Gross profit expanded by a robust 27%, indicating margin improvement driven partly by operational scale and manufacturing efficiencies amid stable cost of sales metrics. Operating income nearly doubled year-over-year to $255 million underscoring operating leverage benefits despite increased SG&A investments [S4,S6].

Cash generation was strong with operating cash flow more than doubling to $526 million in Q1 versus prior year setting a foundation for reinvestment.

DexCom’s Core Business Model and Product Portfolio Quality

DexCom derives its top-line primarily through recurring disposables — single-use glucose sensor strips worn on patients — combined with longer-life reusable transmitters that interface via Bluetooth or other wireless protocols to smartphones or standalone receivers [S1]. This model aligns customer retention incentives since sensor usage is monthly or biweekly while transmitters provide continuity over multiple cycles.

The strategic centerpiece is the G7 CGM system launched in 2023 and refined with a 15-day wear variant introduced in late 2025. This system integrates advanced biosensors with user-friendly devices featuring superior accuracy verified through FDA approvals that set high barriers for competitors.

Moreover, the introduction of the Stelo biosensor targets the large adult prediabetes and non-insulin dependent Type 2 diabetes population segment — an emerging addressable market signaling DexCom's intent to expand beyond traditionally insulin-dependent users.

Importantly, DexCom invests heavily in R&D to improve sensing capabilities and extend analytic value through machine-learning driven insights aimed at behavioral changes or metabolic health management beyond simple glucose tracking.

Revenues thus reflect volume growth in disposables driven by patient adoption as well as incremental unit pricing changes tied to new product launches or improved features.

Competitive Positioning within the Continuous Glucose Monitoring Industry

Within medical devices specializing in diabetes management solutions, DexCom holds a leading position based on early entrance (first FDA approvals dating back over a decade), consistent innovation cadence, and an integrated ecosystem approach whereby its CGMs complement third-party insulin pumps or automated delivery systems enhancing switching costs.

Regulatory complexity creates formidable hurdles: establishing safety and efficacy through clinical trials is capital intensive with lengthy timelines limiting new entrants’ speed-to-market.

Additionally, patient preference trends show increasing CGM usage adoption not only among Type 1 but progressively among Type 2 diabetics whose management previously relied predominantly on less frequent testing methods.

Pricing power appears sustainable given clinical evidence supporting improved outcomes (e.g., HbA1c control) that justify payer support; however reimbursement rates vary across geographies requiring ongoing negotiation efforts.

Competitors include large diversified medical device players deploying biosensor technologies but generally lack DexCom’s focused continuous glucose monitoring specialization.

Key Drivers Supporting Future Growth Trajectory

Several measurable catalysts underpin DexCom's growth outlook:

- Ongoing expansion into non-insulin dependent Type 2 diabetic segment leveraging OTC Stelo biosensor launch signals broader metabolic health applicability [S1,N3].

- Incremental patient adoption rates buttressed by direct sales effectiveness complemented by distribution partners expand reach especially outside core U.S. markets.

- Continued enhancement of sensor accuracy and wear duration aiming to reduce patient burden enhances retention rates.

- Development of data platforms applying machine learning offers differentiated predictive insights increasing customer stickiness.

- Regulatory approvals pending for next-generation devices could unlock additional markets including hospital use cases hinted at in corporate disclosures.

- Favorable reimbursement environment progress—namely expanded insurance coverage for CGM in Type 2 populations—directly influences volume growth potential.

Tracking KPIs such as active sensor user counts per quarter, gross margins linked to cost improvements in manufacturing supplies analogous to other high-tech diagnostics firms, and recurrent revenue proportions provides insight into execution momentum.

Risks and Constraints Impacting Performance and Expansion

Despite solid positioning, DexCom faces notable challenges:

- Competitive pressure intensifies as incumbent medical device makers either develop CGM products internally or acquire biotech startups targeting overlapping spaces that may exert price or feature pressure.

- Regulatory landscape outside mature markets exhibits variability introducing uncertainty around timing for approvals necessary for international expansion.

- Operational execution risk is noteworthy given reliance on disposable sensors subject to inventory forecasting complexities where surplus stock might impair margins or shortages impact customer satisfaction.

- Insurance reimbursement policies remain uneven across payers—in particular regarding coverage for prediabetic populations targeted by Stelo potentially constraining immediate uptake.

- Litigation exposure related to product liability or intellectual property disputes poses sporadic but material risk requiring continued risk management efforts.

Overall these risks necessitate balanced resource allocation between aggressive growth initiatives and cautious operational discipline.

Upcoming Milestones and Market Signals to Monitor

Stakeholders should prioritize tracking:

- Next quarterly shipment volumes particularly post Q1 when deductible reset effects normalize indicating organic demand strength [N3].

- FDA review announcements related to new form factors or extended-wear versions enabling competitive differentiation [S3,N11].

- Strategic partnership developments especially those integrating CGMs into broader metabolic health ecosystems expanding end-user base beyond diabetic populations.

- Changes in reimbursement guidelines reflecting expanding access particularly for prediabetes-related indications which could materially influence addressable market size.

- Early-stage pipeline advancements leveraging next-gen sensing technology or AI-enabled analytics adding latent revenue streams long term.

These markers will offer tangible evidence about execution quality against company guidance frames exposed through investor communications post Q1 release periods.

Latest Financial Snapshot: Liquidity, Debt, and Capital Allocation

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1.12 billion | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026 (end of Q1), DexCom maintained approximately $1.12 billion in cash and cash equivalents [F1,S2]. Long-term debt comprises unsecured senior convertible notes due in 2028 totaling about $1.25 billion with no notes maturing imminently following full repayment of $1.21 billion senior convertible notes due November 2025 earlier last year evidencing proactive debt management [S2].

It does not constitute investment advice but aims to offer a detailed understanding of DexCom’s operating environment based exclusively on disclosed evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments