AMERISAFE Inc’s Workers' Compensation Niche Confronts Profit Pressures Despite Premium Increases

The company’s specialized underwriting and operational efficiency face constraints from rising claims costs and cash flow declines in a competitive hazardous industries market.

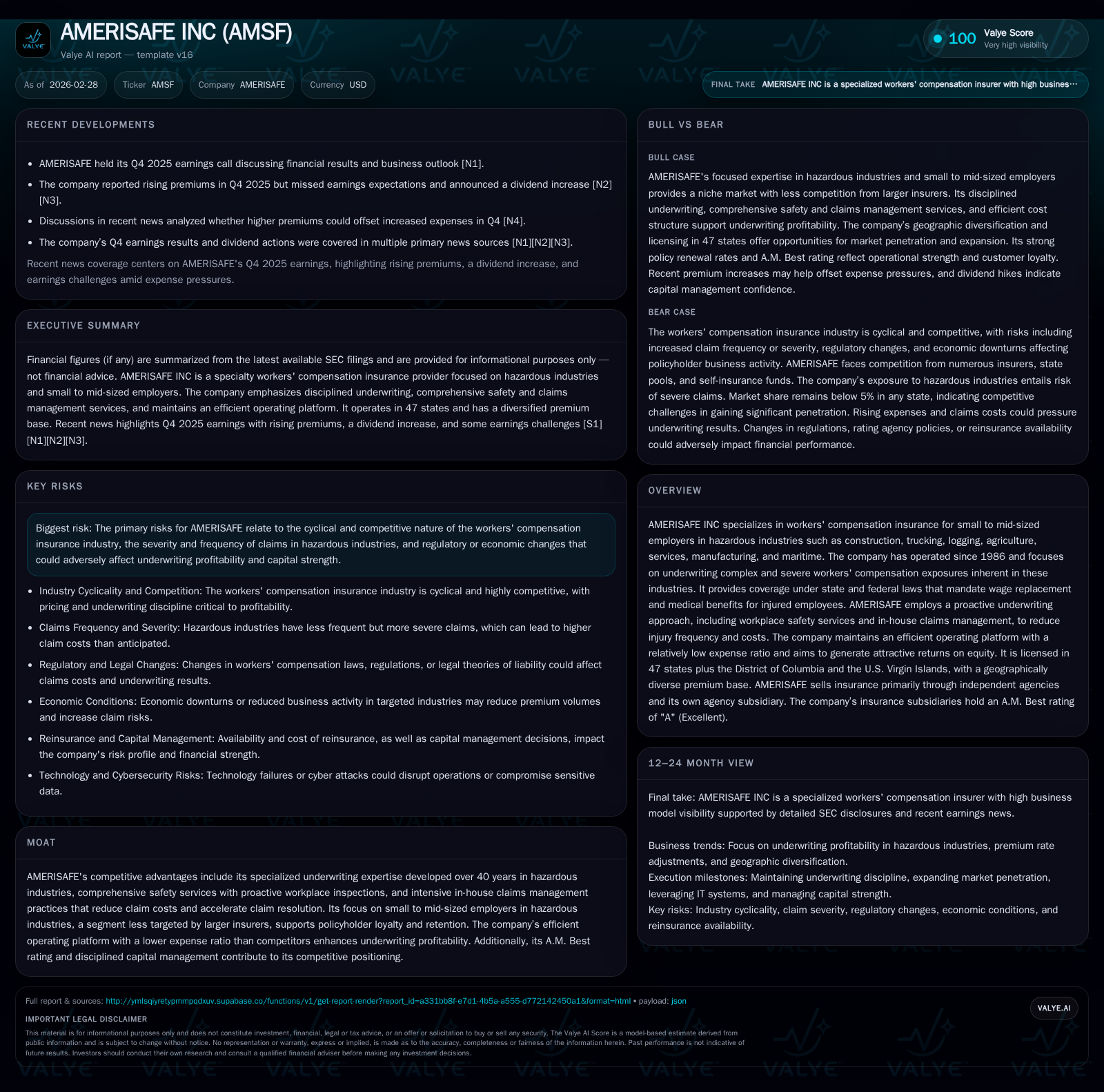

AMERISAFE Inc (AMSF), a specialty workers' compensation insurer focused on high-risk small to mid-sized employers, reported modest revenue growth in 2025 but experienced a significant decline in net income and operating cash flow. The firm’s strategic advantages in underwriting discipline, safety services, and claims management underpin its durable position in hazardous sectors like construction and trucking. However, elevated injury severity and higher expenses pressured earnings, leading to an earnings miss despite premium rate hikes. Capital allocation remains shareholder friendly through dividends and limited buybacks, but free cash flow compression calls for monitoring. Geographic diversification and market penetration provide growth levers, though industry cyclicality and regulatory risks persist.

Company Overview

AMERISAFE Inc (Nasdaq: AMSF) specializes in workers’ compensation insurance targeting small to mid-sized employers engaged primarily in hazardous industries such as construction, trucking, logging, agriculture, manufacturing, maritime operations, and related service sectors [S1]. Founded in 1986 initially focusing on logging contractors in the southeastern US, the company now operates nationally with licenses in 47 states plus the District of Columbia and U.S. Virgin Islands [S1][S4]. Through its three insurance subsidiaries domiciled mainly in Nebraska and Texas, AMERISAFE applies proprietary underwriting expertise developed over four decades aimed at complex injury exposures typical of high-risk workplaces.

Historical Performance

Over the past four years ending FY2025, AMERISAFE has achieved consistent if modest top-line growth driven by incremental premium rate increases matched against total premium volume fluctuations reflecting market penetration efforts [F1]. Revenue expanded from $294.7 million in FY2022 to $317.3 million by FY2025—a compounded annual growth rate just under 2.5%. Notably, the premium increases are linked closely to elevated injury costs faced by policyholders who operate in inherently dangerous environments causing more severe injuries than seen broadly across other insurance segments [S1].

However, profitability has trended downward since its peak in FY2023 when net income reached $62.1 million before easing to $47.1 million last year—a decline of approximately 15% [F1]. Operating cash flows fell even more dramatically by over half compared to prior years ($11.1 million reported CFO vs $24.2 million the year prior), highlighting tightening working capital dynamics tied to claim payments timing and potentially reserving adjustments [F1]. Capital expenditures rose significantly last year—more than doubling year-over-year—which contributed further to reduced free cash flow availability [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 317 | 47 | 11 | 2 | +2.7% | -15.0% |

| 2024 | 309 | 55 | 24 | 1 | +0.7% | -10.7% |

| 2023 | 307 | 62 | 30 | 1 | +4.1% | +11.7% |

| 2022 | 295 | 56 | 28 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 63 | 9 | 18.7 |

| 2024 | 71 | 23 | 21.5 |

| 2023 | 56 | 29 | 21.2 |

| 2022 | 78 | 26 | 17.5 |

Source: SEC companyfacts cache [F1].

Table: Summary of financial performance shows steady revenue gains but declining margins and cash flows [F1]

Future Growth Prospects

AMERISAFE pursues growth primarily through increased market penetration within its existing core states where it holds less than a five percent market share per state [S4]. The company is licensed broadly beyond its marketing footprint, implying capacity for geographic expansion without requiring new approvals or licenses [S4]. Its niche focus allows it to underwrite risks using data-driven actuarial models tuned for hazardous workplace exposures—enabling competitive pricing compared with state pools or larger insurers less specialized [S4][S23].

Product innovation combines underwriting with safety services aimed at reducing injury frequency & severity—an essential value add helping retain clients who might otherwise shop price alone [S1][S23]. Advanced claims management practices also seek rapid case resolution curbing long-tail liabilities common in workers’ comp insurance.

Potential constraints include regulatory shifts affecting mandated benefits or rate-setting processes across jurisdictions where AMERISAFE operates—workers’ compensation remains heavily state regulated [S5]. Economic slowdowns impacting labor-intensive industries targeted may reduce premium volumes or alter loss patterns.

Guidance & Key Milestones

There is no explicit forward-looking guidance disclosed for revenue or earnings targets for CY2026 within the latest filings or earnings calls [N1][N3][S3]. Investors should watch for renewal rate changes given inflationary pressures on medical costs, any shifts in claims loss reserves during quarterly reporting which can materially affect profitability, and ongoing operational leverage metrics like expense ratios.

Dividends remain an important milestone signaling confidence; recently increased quarterly dividend announced at $0.41 per share reflects commitment to returning capital despite near-term earnings pressures [N2][S3].

Capital Allocation & Returns

AMERISAFE delivered an approximate return on equity around 18.7% for FY2025 based on net income of $47.1 million against equity of roughly $251.6 million [F1]. While down from peaks seen earlier due to lower net income levels, this remains a solid absolute level indicating efficient capital deployment relative to risk.

Capital returns focus predominantly on dividends with distributions totaling $62.7 million last year—reduced slightly from $71 million the prior year reflecting more cautious cash flow outlooks amid softening profitability [F1]. Share repurchases have been minimal recently; only a small buyback amount was recorded back in FY2023 reflecting selective use of excess capital after dividend commitments.

Operating cash flow generation was insufficient compared to dividend payouts last year implying some reliance on working capital or financing flexibility—free cash flow after CAPEX stood at just under $9 million showing tightened liquidity buffer versus historical norms [F1]. Investment portfolio quality backs balance sheet strength supporting A.M Best rating "A" (Excellent), with fixed maturities constituting over 80% of portfolio weight characterized largely by municipal bonds and corporate securities rated "A" or better credit quality [S13][S16][S22].

Competitive Position & Industry Context

The workers' compensation insurance segment serving hazardous industries is fragmented with about 300 carriers competing varying by state market and industry specialization [S23]. AMERISAFE's durability rests on its deep underwriting expertise tailored specifically for complex severe exposures uncommon among generalist insurers.

The company leverages proactive workplace safety services involving field inspections that not only mitigate claims frequency but foster policyholder loyalty—a critical moat given the price sensitivity within this segment . Its claims handling features intensive personal engagement shortening claim cycles thereby reducing ultimate settlement costs.

Even as larger insurers contest this space intermittently, AMERISAFE's lower expense ratio (~30% as per latest reports) positions it competitively to yield underwriting profits alongside prudent premium rate adequacy adjustments responding dynamically to loss cost trends [S4][N7].

Risks & Uncertainties

Noteworthy risks include:

- Volatility inherent in claims severity and frequency given unpredictable ruptures at hazardous worksites affecting loss reserves unpredictably.

- Regulatory risk from potential statutory reforms altering benefit structures or caps negatively impacting pricing power.

- Intensifying competition possibly compressing premium rates especially if economic conditions soften demand from core industrial customers.

- Investment portfolio credit or interest rate risks influencing net investment income stability amid rising interest rate environments.

- Operational risk linked to sustaining low expense ratio while investing judiciously into technology and workforce retention crucial for underwriting effectiveness.

Conclusion & Monitoring Points

AMERISAFE embodies a specialist insurer occupying distinct niches within high-hazard sectors providing opportunities for stable revenue growth backed by underwriting discipline and operational efficiencies.

Nevertheless, recent trends show profit margin contraction amidst increasing claims costs pressuring earnings quality while impactful cash flow declines warrant close attention moving forward.

Key developments worth monitoring include renewal pricing effectiveness amidst inflationary cost pressures; evolution of incurred but not reported loss reserves reflected each quarter; maintenance of disciplined expense control; dividend sustainability against underlying cash flows; and any shifts in regulatory landscape across core states influencing business mix or pricing freedom.

Disclaimer

This analysis is intended solely for informational purposes without recommendation regarding any securities or investments related thereto.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments