Anika Therapeutics’ Strategic Reliance on J&J and Its Financial Turning Point

Anika Therapeutics leverages exclusive manufacturing partnerships with Johnson & Johnson MedTech while confronting operational losses and improving cash flow dynamics.

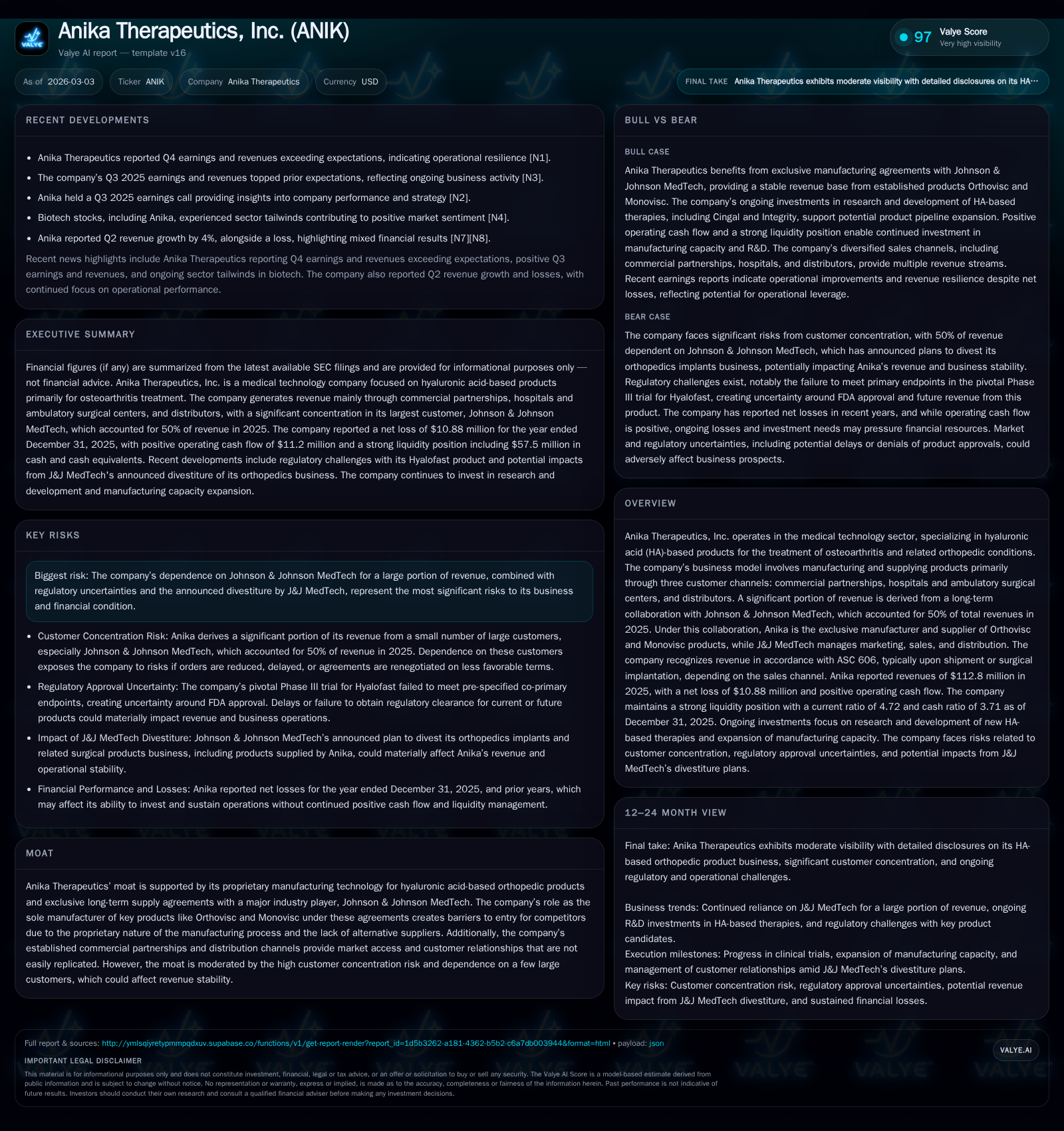

Anika Therapeutics, specializing in hyaluronic acid-based orthopedic products, generated approximately half its revenue through an exclusive manufacturing agreement with Johnson & Johnson MedTech in 2025. Despite a 2.3% year-over-year revenue increase to $112.8 million, operating losses widened due to margin pressures and increased research and development expenses. However, operating cash flow more than doubled to $11.2 million, supporting positive free cash flow after capital expenditures. The company’s dependence on J&J MedTech presents both strategic exclusivity and significant customer concentration risk, heightened by announced divestiture plans at J&J MedTech. Future growth prospects remain linked to regulatory decisions for new products and efforts to diversify commercial channels.

Historical Financial Performance

Anika Therapeutics’ recent financials show a mixed pattern of modest revenue growth alongside increasing operating challenges. Revenue advanced by 2.3% year-over-year in 2025 to approximately $112.8 million following declines from prior years ([F1], [N1]). Despite this top-line resilience, operating losses widened significantly to $11.05 million in 2025 from $5.1 million in 2024 ([F1], [S14]). This deterioration was primarily driven by reduced gross profit margins coupled with increased investment in research and development activities aimed at advancing regenerative medicine programs ([S6]).

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -11 | 11 | -11 | 7 | +80.7% |

| 2024 | -56 | 5 | -5 | 8 | +31.8% |

| 2023 | -83 | -2 | -88 | 5 | -456.3% |

| 2022 | -15 | 4 | -19 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 9 | 4 | -7.6 |

| 2024 | 11 | -2 | -36.6 |

| 2023 | 5 | -7 | -38.9 |

| 2022 | -3 | -5.2 |

Source: SEC companyfacts cache [F1].

Note: Operating income and net income include continuing operations; discontinued operations impact prior years substantially.

Strategic Dependence on Johnson & Johnson MedTech

A critical feature of Anika's business model is its exclusive manufacturing relationship with Johnson & Johnson MedTech (J&J), which accounted for approximately half of total revenue in 2025 ([S7], [S16]). This partnership centers on Anika’s role as the sole manufacturer of two flagship hyaluronic acid osteoarthritis treatments: Orthovisc and Monovisc.

While Anika controls manufacturing exclusively, J&J manages marketing, sales, pricing, and distribution within the U.S., underscoring a division of responsibilities that creates significant barriers for competitors due to proprietary manufacturing processes ([S2], [S26]).

However, this dependency concentrates risk materially; J&J's announced plans to divest its orthopedic implants business inject uncertainty into future contract renewals and volume commitments ([N1], [S2]). Given J&J's unilateral control over end-user pricing and promotion strategies, any changes could materially disrupt Anika’s near-term revenue predictability.

Regulatory Landscape and Product Pipeline

Beyond its core OEM product lines, Anika is pursuing growth through regenerative medicine technologies such as Hyalofast, a cartilage repair therapy currently marketed outside the U.S., with ongoing efforts toward FDA approval ([S2]).

The pivotal FastTRACK Phase III trial results released in mid-2025 did not meet co-primary endpoints required for straightforward FDA approval but showed statistically significant improvements on secondary measures ([S2]). This leaves regulatory approval uncertain and tempers expectations for near-term commercial expansion beyond established OEM revenues.

Cash Flow Improvement Amid Operating Losses

Despite persistent GAAP losses, Anika has improved operational cash generation markedly—operating cash flow nearly doubled from $5.4 million in 2024 to over $11 million in 2025 ([F1], [S12]). This improvement reflects better working capital management and cost discipline amid complex production requirements.

Capital expenditures decreased slightly year-over-year to about $6.8 million as investments stabilized after prior capacity expansions ([F1], [S25]). The resulting positive free cash flow of approximately $4.36 million (operating cash flow minus capex) marks a notable inflection point supporting financial flexibility.

Liquidity remains robust with cash and equivalents totaling $57.5 million at December 31, 2025, alongside working capital exceeding $80 million—yielding a strong current ratio above four times ([F1], [S12]). No borrowings were drawn against the company’s revolving credit facility valued at up to $75 million, which can be expanded subject to lender approvals ([S4]).

Capital Allocation Priorities

In line with shareholder return objectives, Anika repurchased approximately $9.5 million of shares during 2025 through an active buyback program initiated mid-2024 ([F1], [S22]). No dividends have been declared as capital allocation prioritizes reinvestment into research and development pipelines.

Leverage remains conservative with zero debt outstanding under the credit facility despite available borrowing capacity providing optionality if needed.

Outlook: Growth Drivers and Risks Ahead

Forward-looking guidance remains cautious pending regulatory clarity around Hyalofast approval and developments related to the J&J MedTech divestiture process ([N1], [S2]). The company is also gradually expanding its commercial infrastructure beyond OEM reliance but faces entrenched distribution dynamics globally that may slow diversification progress ([N1], [S16]).

Absent regulatory breakthroughs or successful channel expansion, revenue growth may remain constrained by concentrated OEM partnerships.

Proprietary Technology Moat

Anika's competitive advantage derives from its specialized proprietary processes for synthesizing cross-linked hyaluronic acid formulations tailored for orthopedic applications ([S26]). Exclusive supply agreements further entrench barriers preventing competitors or OEM partners from replicating core product offerings swiftly or easily.

This moat supports sustained revenues but requires continuous quality controls given stringent medical device regulations.

Customer Concentration Risk Considerations

Customer concentration risk is significant with a few large customers accounting for most revenues—particularly J&J MedTech representing about half of sales in recent years ([F1], [S21]). Contractual terms grant J&J substantial control over pricing strategy impacting Anika’s revenue potential.

Any adverse changes or early termination could disrupt revenue streams materially.

Summary

Anika Therapeutics demonstrates measured stabilization after challenging years marked by operating losses but improving cash flows and liquidity positions as of fiscal year-end 2025. The company’s reliance on exclusive OEM partnerships offers strategic advantages but carries material concentration risks heightened by evolving market dynamics including J&J MedTech’s divestiture plans.

Future performance hinges critically on regulatory outcomes for pipeline products like Hyalofast and successful diversification of commercial channels beyond concentrated OEM sales.

This analysis synthesizes publicly available SEC filings up through March 3, 2026 ([F1],[S1]-[S29]) along with news reports ([N1]) without speculative forecasts or unprovided guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments