Alto Neuroscience Expands Clinical Pipeline with Strong Liquidity but Faces Revenue Generation and Regulatory Hurdles

Alto Neuroscience reported sustained R&D investment in clinical-stage psychiatric treatments backed by robust cash reserves following recent private placements.

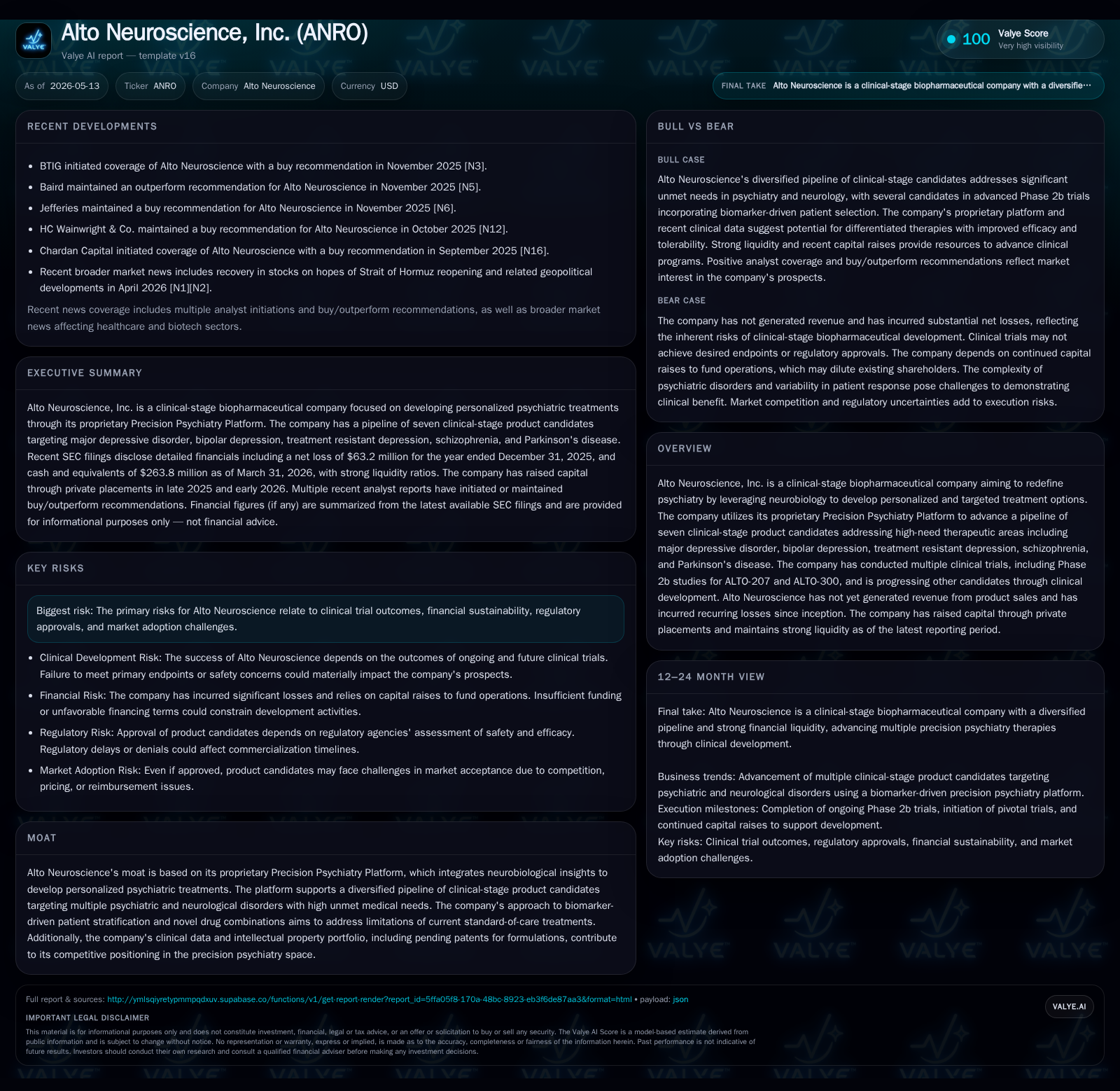

Alto Neuroscience, a clinical-stage biopharmaceutical company focused on personalized psychiatry via its proprietary Precision Psychiatry Platform, reported in its latest quarterly filing ongoing clinical development of seven product candidates targeting major depressive disorder, bipolar depression, treatment-resistant depression, schizophrenia, and Parkinson’s-related depression. It remains pre-revenue but strengthened its liquidity position through two recent private placement financings totaling nearly $165 million net proceeds. The company plans to advance multiple Phase 2b and Phase 3 trials while preparing for potential regulatory approvals and commercialization investments. Key risks include the inherent uncertainties of clinical outcomes, required companion diagnostic development, regulatory approvals, and building commercialization capabilities.

Recent Operating Update

Alto Neuroscience latest quarterly filing (10-Q) dated May 13, 2026 [S2] reveals no changes in revenue status as the company remains pre-commercialization with no product sales. The firm’s extensive clinical programs continue advancing with a focus on multiple psychiatric indications. Notably, cash and cash equivalents stood robust at approximately $264 million as of March 31, 2026 [F1], supported by two rounds of private placement financings — about $50 million in October 2025 and roughly $115 million in March 2026 [S2]. This strong liquidity footprint underpins planned R&D activities through at least 2028.

The filing underscores ongoing substantial investment in research and development including personnel costs, clinical trial expenses with contract research organizations (CROs), manufacturing scale-up preparation, regulatory activities, and licensing fees [S17]. The company reiterates that despite this capital deployment there is no assurance of regulatory approval or successful commercial launch for any candidate. Moreover, upon approval of any product candidate(s), Alto anticipates sizable expenditures related to building its internal commercialization capabilities encompassing sales, marketing, and distribution efforts [S2].

No material changes in risk factors were noted from prior disclosures [S2].

Business Model and Strategic Positioning

Alto Neuroscience operates as a clinical-stage biopharmaceutical entity leveraging its proprietary 'Precision Psychiatry Platform' — a technology suite aimed at identifying brain-based biomarkers to facilitate personalized therapeutic interventions across psychiatric illnesses. The platform informs both the biology-driven selection of patient subgroups and mechanism-based drug composition strategies.

Revenue generation is currently non-existent as all seven pipeline candidates remain pre-approval at various stages from Phase 2b through Phase 3 trials [S1][S2]. Post-approval revenue would principally stem from direct product sales once the company either internally commercializes or partners these drugs. Ahead of that phase, financing activities — predominantly equity-based — have funded operations.

The strategic strength rests in the platform’s potential to reshape treatment paradigms by addressing heterogeneity in psychiatric disorders such as major depressive disorder (MDD), bipolar depression (BPD), treatment resistant depression (TRD), schizophrenia, and Parkinson’s disease-related symptoms. By harnessing biomarker data to optimize patient responsiveness predictions and combining novel agents like ALTO-207 (a dopamine agonist combination), Alto aims to overcome efficacy plateaus common in current antidepressants.

However, building commercialization capability post-approval introduces expected significant cost increases to support marketing efforts intrinsically complex within psychiatry due to nuanced diagnosis patterns and payer reimbursement landscapes [S2]. There are high barriers regarding physician adoption and payor coverage which depend heavily on demonstrating differentiated benefit through companion diagnostics.

Industry Structure and Competitive Landscape

Precision psychiatry remains an embryonic but rapidly evolving domain within neuroscience drug development. Major pharmaceutical incumbents and specialized biotech players alike are pursuing target-specific therapies complemented by diagnostic tools aiming to reduce trial-and-error prescribing prevalent in the mental health field.

Alto holds competitive moats from:

- Its proprietary biomarker-driven approach that facilitates tailored patient stratification potentially improving responder rates;

- A diversified portfolio tackling multiple therapeutic areas with unmet needs;

- Ongoing Phase 2b/Phase 3 clinical undertakings that can establish robust evidence;

- Intellectual property protecting formulations alongside platform methodologies.

Yet challenges remain profound given:

- The complexity of psychiatric biology translating into high developmental risk;

- Heavy regulatory scrutiny surrounding drug-device combination products (therapeutics plus diagnostics);

- Market penetration difficulty due partly to stigma associated with mental illness diagnosis,

- Established standard-of-care drugs with entrenched use though often suboptimal efficacy.

Competition extends from legacy antidepressants makers adapting precision elements into their pipelines to disruptive startups focusing on rapid-acting agents or digital neurotherapeutics. Success depends on proving clear superiority over fragmented treatments spread across psychopharmacology.

Growth Drivers

Key growth vectors for Alto Neuroscience hinge primarily on clinical progression milestones paired with efficient capital utilization:

- Advancement of Clinical Trials: Successful enrolment completion and positive top-line data readouts from Phase 2b/3 studies for candidates such as ALTO-207, ALTO-300 signal credible progress toward regulatory submissions [S2].

- Companion Diagnostic Development: Gaining FDA consensus on biomarker assays integral for patient selection will enhance differentiation and support payer acceptance.

- Capital Raising: Continued access to equity financing or collaborations enables sustained R&D throughput vital until commercial readiness.

- Strategic Partnerships or Licensing: Potential alliances could accelerate late-stage development or commercialization reach while mitigating capital intensity burdens.

- Platform Scaling: Extending the Precision Psychiatry Platform pipeline by adding assets or indications could broaden eventual market opportunity.

The interplay between scientific demonstration of efficacy within well-defined patient subgroups leverages structural demand driven by large populations inadequately served by current treatments. Reimbursement dynamics also play a role pending favorable incorporation of diagnostics into healthcare systems.

Risks and Watchpoints

Alto Neuroscience is exposed to standard sector-specific uncertainties alongside unique precisions psychiatry challenges:

- Clinical Trial Failure Risk: Attrition rates typical in neuroscience drug development impose significant uncertainty; earlier phase success is not guaranteed predictive for later outcomes.

- Regulatory Approval Complexity: Efficacy must be shown alongside safety; additionally approval pathways for companion diagnostics can cause delay or denial impacting timelines [S2].

- Financial Sustainability: Despite strong near-term liquidity ($264m cash), further substantial financing is anticipated given ongoing negative operating cash flow; capital markets conditions may affect raising ability [F1][S2].

- Commercial Execution Risk: Developing commercial infrastructure presents operational challenges especially in fragmented psychiatry markets requiring demanding stakeholder engagement.

- Reimbursement Uncertainty: Coverage decisions by payors depend heavily on demonstrating value beyond existing products; pricing pressures are stringent globally including EU controls [S10][S11].

- Technology Obsolescence: Rapid innovation pace means the platform must continuously evolve or risk becoming outdated versus alternative modalities like digital therapeutics.

- Legal/Compliance Exposure: Biopharma regulations around marketing practices impose additional costs/risks if infractions occur unintentionally.

Monitoring actual patient response data outcomes combined with regulatory feedback on companion diagnostic acceptance represent critical near-term watchpoints for assessing program viability.

What To Watch Next

Investors should focus closely on:

- Clinical Milestones: Announcement timing/results for Phase 2b ALTO-300 MDD study readout; Phase 3 preparation status for ALTO-207; insights from ongoing ALTO-101 proof-of-concept trials [S17].

- FDA Interactions: Official guidance regarding required companion diagnostics for lead candidates can materially influence Go-To-Market strategy [S1][S2].

- Cash Burn Rate Progression: Quarterly updates on R&D expense trajectories reflecting trial enrollment pace or manufacturing scale-up.

- Capital Markets Activity: Additional equity offerings or collaboration/licensing deals signaling financial runway extension or validation.

- Regulatory Filings: Submission dates/acceptance determination for New Drug Applications (NDAs) or Breakthrough Therapy Designations enhancing commercial confidence.

- Partnership Announcements: Alliances especially focused on commercial distribution or co-development could mitigate execution risks.

Financial Profile Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $264mm | |

| 2026-03-31 | ||

| Current assets | $269mm | |

| 2026-03-31 | ||

| Current liabilities | $13mm | |

| 2026-03-31 | ||

| Current ratio | 20.52x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Although detailed financial history is secondary here given early-stage status, key balance sheet metrics provide important context. As of March 31, 2026:

This commanding liquidity position typifies Alto's ability to sustain expensive neurological R&D operations unencumbered by near-term debt maturities [F1]. Operating losses remain elevated reflecting ongoing Phase trial costs with no offsetting revenues yet realized [F1][S1].

In sum, Alto's financial strategy hinges largely on continued equity issuance amid prolonged pre-commercialization loss layers typical of innovative biotech ventures directed at complex CNS diseases.

This analysis intends solely to provide a grounded understanding of Alto Neuroscience's business model evolution driven by latest SEC filings alongside industry context without implying investment advice or forecasts. Any forward-looking statements contained herein depend heavily on yet uncertain variables typical within early-stage biopharmaceutical development.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments