Lionheart Holdings Faces Critical Juncture as SPAC Deadline Approaches

With its June 2026 deadline imminent, Lionheart Holdings confronts significant operational and strategic challenges intrinsic to SPAC structures.

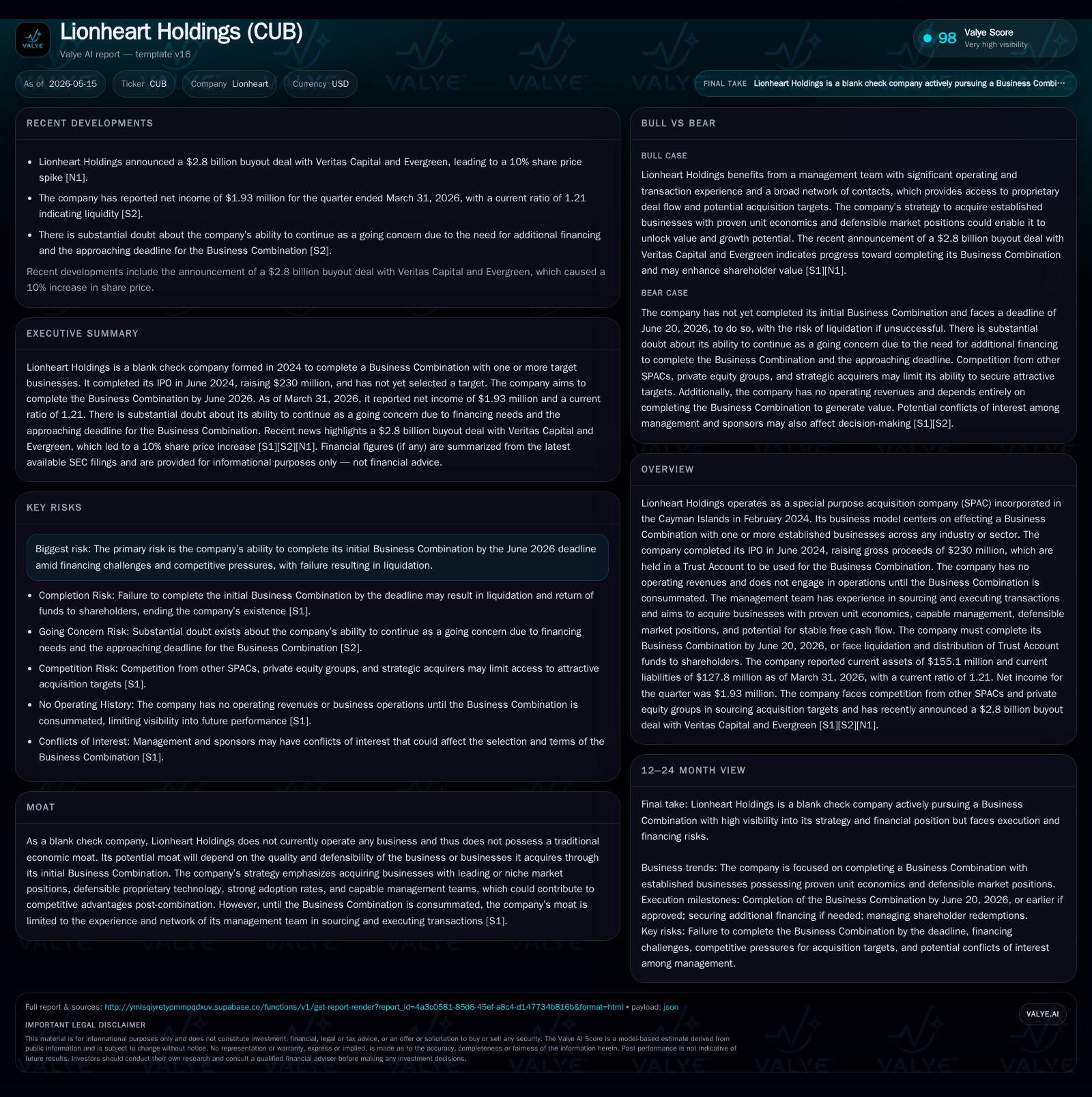

Lionheart Holdings, a Cayman Islands-incorporated blank check company, is entering the final stages before its mandatory business combination deadline of June 20, 2026. The company holds $230 million raised in its IPO within a trust account, yet it has generated no operating revenues and faces substantial doubt regarding its ability to continue as a going concern given the compressed timeline and uncompleted merger. Competition across the SPAC space intensifies deal sourcing difficulties, while management pursues acquisition targets with stable unit economics and defensible market positions to unlock public company advantages post-transaction. The path forward hinges on securing suitable target(s), executing financing arrangements if needed, and ultimately consummating the initial business combination or facing liquidation.

Latest Quarterly Filing Signals Critical Milestone

Lionheart Holdings’ most recent Form 10-Q filing dated May 14, 2026 ([S2]) starkly underscores the company's precarious operational state as it approaches the statutory Business Combination deadline of June 20, 2026. Management explicitly acknowledges "substantial doubt" about its ability to continue as a going concern without completing an initial Business Combination within roughly one year from the filing date. This reflects inherent risks associated with blank check companies that have yet to consummate merger transactions critical for commencing operations and generating revenue streams. Importantly, Lionheart has no current revenues or operating business activities pending consummation of the Business Combination.

This update frames Lionheart at a pivotal structural crossroads; either it effectuates an initial Business Combination imminently or must face liquidation protocols distributing Trust Account funds back to Public Shareholders per its legal charter.

SPAC Business Model and Operational Status

Incorporated in February 2024 in the Cayman Islands as a special purpose acquisition company (SPAC), Lionheart Holdings completed its IPO in June 2024 raising gross proceeds of approximately $230 million ([S1],[S7]). These proceeds are securely maintained in a Trust Account controlled by an independent trustee to exclusively fund the eventual Business Combination transaction(s). Before accomplishing this merger or acquisition event, Lionheart does not engage in operational activities or generate revenue.

The company’s operational model hinges entirely on identifying one or more target businesses across any industry sector that meet specific investment criteria. Its management team—comprised of executives with deal-sourcing and transaction execution experience—is tasked with negotiating these combinations during the limited "Combination Period" set by regulatory and exchange requirements at 24 months from IPO closing (due June 20, 2026). Failure to complete a Business Combination by this juncture results in dissolution.

Via this structure, Lionheart offers prospective private companies an alternative public listing route that can potentially mitigate traditional IPO complexities such as prolonged marketing timelines, underwriting discounts, and market uncertainties ([S4]). The target business owners may receive consideration via equity shares convertible into Lionheart Class A Ordinary Shares or cash or combinations thereof tailored to their preferences.

Competitive Environment for Business Combination Targets

The current arena for executing successful business combinations is notably competitive and complex. Since mid-2024—aligned with Lionheart’s timeline—the proliferation of SPACs has intensified competition for attractive targets that meet stringent criteria including proven unit economics and defensible market positions ([S1],[S6]). Additionally, broader market skepticism towards SPAC-sponsored mergers introduces reputational headwinds potentially limiting willingness among high-quality private companies to engage.

Private equity firms, leveraged buyout funds, operating businesses pursuing strategic acquisitions, plus rival SPACs present formidable competition due to their potentially greater financial firepower or sector expertise ([S1]). Consequently, these dynamics elevate acquisition costs and may narrow viable target pools.

Due diligence complexity also escalates: assessment requires comprehensive scrutiny of management quality, financial controls compliance (including Sarbanes-Oxley readiness), operational stability post-combination potential disruptions—all under tight deadlines ([S12]).

Growth Opportunities and Strategic Advantages Post-Combination

Should Lionheart successfully complete its Business Combination(s), growth prospects derive primarily from newly public companies benefiting from capital market access unavailable privately ([S3],[S6]). This includes enhanced funding mechanisms for organic expansion or acquisitions as well as incentives aligned with shareholder value creation through liquid ownership stakes.

Management specifically seeks targets demonstrating:

- Established scale with attractive unit economics,

- Strong existing or near-term free cash flow generation,

- Defensible niche market positions against competitors,

- Experienced leadership teams capable of sustaining scalable growth models ([S3],[S10]).

Public company status afforded post-merger confers credibility elevation among customers/vendors and aids talent recruitment alongside facilitating strategic corporate actions such as acquisitions leveraging stock currency.

Risks and Execution Challenges in Completing the Business Combination

Major risk centers on failing to consummate a qualifying Business Combination before June 20, 2026. Such failure mandates liquidation distributing Trust Account proceeds pro rata back to Public Shareholders while terminating Lionheart’s existence ([S1],[S2]).

This yields a current ratio near 1.21 consistent with classic pre-combination SPAC profiles where operating expenditures are minimal absent revenue generation ([F1]).

Importantly however, these figures exclude Trust Account assets earmarked solely for merger transactions held separately outside regular operations; thus available liquidity for administrative expenses remains extremely limited reinforcing management’s going concern caution shared in recent reporting ([S2]).

This liquidity context supports operational continuity only in the short term pending either transaction completion or orderly wind-down procedures.

Disclaimer: This analysis is based exclusively on publicly available SEC filings through May 15, 2026. It does not constitute investment advice but aims to provide an informed perspective on Lionheart Holdings’ operational status given its unique blank check company business model constraints. Readers should conduct further research before forming conclusions regarding future developments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments