Aptorum Group Advances Lead Therapeutics Amid Financial Strains

Focused drug development and a pending diagnostics merger coincide with liquidity pressures shaping Aptorum’s near-term outlook.

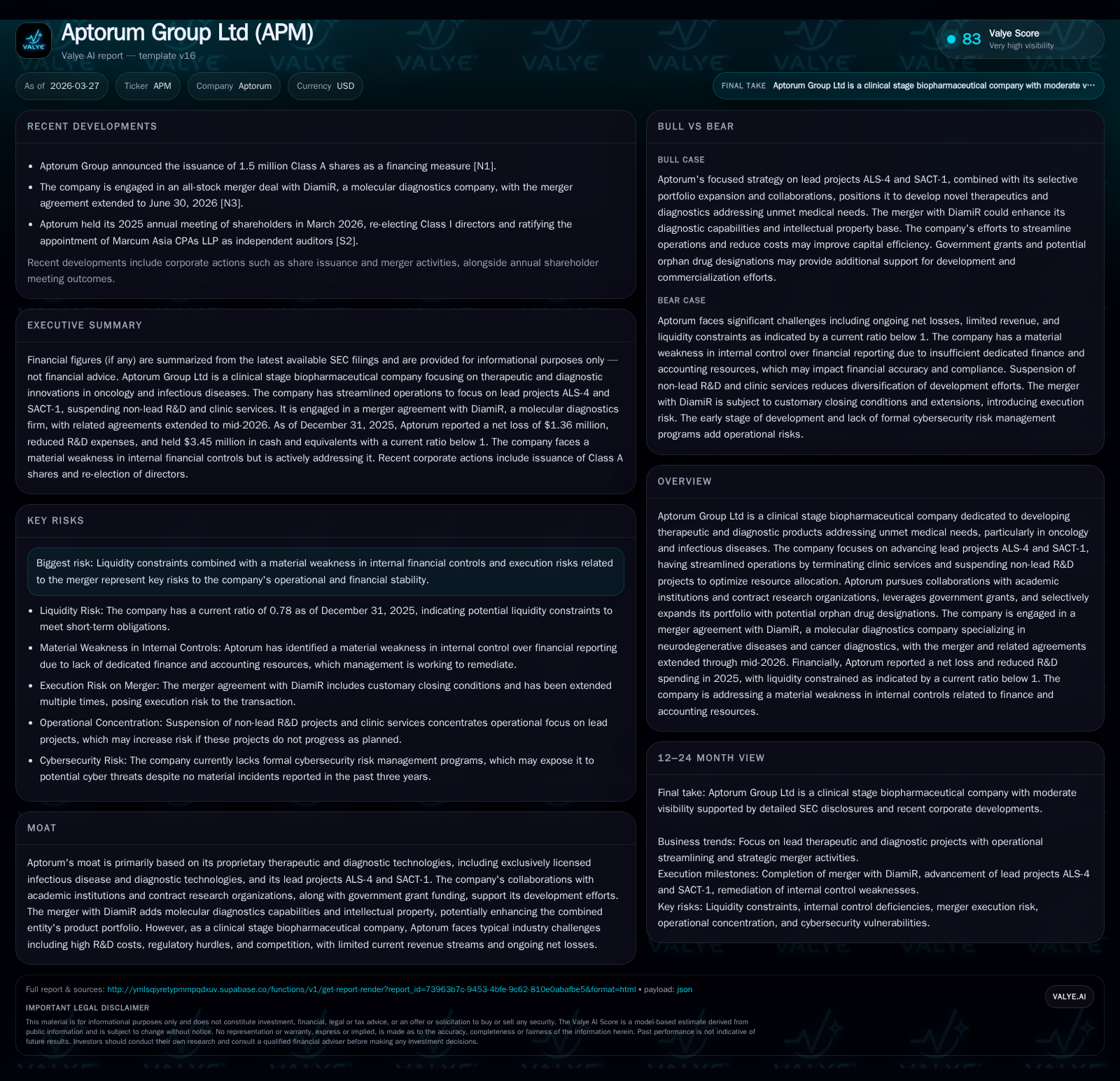

Aptorum Group Ltd has strategically realigned its clinical-stage biopharmaceutical pipeline by prioritizing lead projects ALS-4 and SACT-1 while suspending other R&D efforts and clinic services. This operational pivot helped moderate net losses from $4.27 million in 2024 to $1.36 million in 2025 despite a flat topline of roughly $431K. However, liquidity challenges persist, with current liabilities exceeding current assets, prompting equity raises such as the recent issuance of 1.5 million Class A shares. The company’s merger with molecular diagnostics firm DiamiR represents a significant strategic expansion into neurodegenerative and cancer biomarker diagnostics, potentially diversifying its technology portfolio if successfully executed. Investors should monitor clinical and merger milestones along with cash burn to evaluate Aptorum’s execution and sustainability amid ongoing financial constraints.

From Broad Ambitions to Focused Lead Projects: Historical Growth and Operational Shifts

Aptorum Group Ltd entered the clinical-stage biopharmaceutical arena with an expansive ambition to develop novel and repurposed therapeutic and diagnostic technologies primarily targeting oncology—including orphan indications—and infectious diseases [S1]. Early on, the company pursued diverse programs including clinic services, broad R&D efforts across multiple platforms, and collaborative arrangements with academic institutions and contract research organizations (CROs).

However, in Q2 2023, Aptorum decisively streamlined operations by terminating clinic-related services and suspending all non-core R&D projects [S9][S14]. This strategic pivot centered resource allocation on two lead assets: ALS-4, a proprietary neurologic therapeutic candidate; and SACT-1, a similarly prioritized drug candidate designed to address substantial unmet medical needs. The decision recognized that advancing these highest-potential projects would improve capital efficiency while enhancing programmatic focus—a common tactic in clinical-stage pharma where limited resources mandate stringent prioritization to optimize trial outcomes and potential regulatory pathways.

The abandonment of exploratory diagnostics ventures such as the PathsDx Test collaboration further underscores this refocus [S14]. This reorganization reflects sector norms where companies prune pipelines to extend runway long enough for key data readouts or value-inflecting corporate events.

Financial Performance Recap: Loss Trends Moderating during Stable Topline

Despite maintaining a relatively flat revenue line of approximately $431K for FY2023 through FY2025—largely residual clinic service income prior to cessation—the company significantly curtailed net losses [F1]. Specifically, annual net loss shrank from -$4.27 million in FY2024 to -$1.36 million by FY2025 (a YoY improvement of roughly 68%) [F1][S9][S10].

This moderation is attributable primarily to sharply reduced operating expenses, particularly in R&D which fell from $2.2 million in 2024 to under $0.6 million in 2025 following suspension of non-lead projects [S9][F1]. General administrative costs also declined consistent with streamlined staffing and contracting.

Operating cash flow tracked this trend, improving from an outflow of nearly $1.19 million in FY2024 to about -$1.84 million in FY2025; although still negative, it suggests mitigation of the previous high burn rate typical for early-stage bio/pharma ventures [F1][S7]. This presents some operating leverage benefits albeit against a backdrop of zero organic revenue growth.

Capital Structure Examination: Liquidity Constraints and Equity Issuances

Aptorum’s balance sheet presents challenges common among clinical-stage developers lacking product-derived revenues. At December 31, 2025, current liabilities exceeded current assets ($4.59 million vs $3.59 million), translating into a suboptimal current ratio near 0.78—well below the typical safe threshold—indicating short-term liquidity risks [F1][S4].

To bolster working capital amidst these constraints, Aptorum undertook equity financings including a registered direct offering completed on October 14, 2025 raising approximately $2 million plus concurrent private placement warrants [S15][S22]. More recently on March 27, 2026, the company issued another 1.5 million Class A shares as reported [N1]. Such reliance on equity—versus debt—is characteristic for firms bearing nascent pipelines with uncertain cash inflows.

The going concern disclosures embedded within financial filings highlight management's uncertainties regarding sustained funding without timely capital market access or milestone achievements [S4]. There are no dividend payments or buybacks given negative earnings and cash flow profiles typical for biotech startups.

Pipeline Evolution: ALS-4, SACT-1, and The Strategic Implications of the DiamiR Merger

A cornerstone strategic development has been Aptorum's planned merger with DiamiR—a Delaware-incorporated molecular diagnostics company specializing in minimally invasive blood tests detecting neurodegenerative diseases like Alzheimer’s as well as cancer diagnostics leveraging microRNA biomarker panels protected by extensive patents [S5][S21]. This union could create synergistic value by complementing Aptorum’s therapeutics pipeline with advanced companion diagnostics capabilities helping patient stratification and treatment monitoring.

DiamiR's CLIA/CAP-certified laboratory services further add biopharma analytical specialization that could boost Aptorum's research productivity and expand its commercial scope beyond therapeutics alone—a diversification commonly pursued by biopharma entities seeking de-risked revenue streams through diagnostics integration [S21].

However, merger execution risks are material—including governance complexities around board representation rights granted to DiamiR shareholders controlling up to ~30% ownership post-merger [S17]—and partnership synergies depend heavily on smooth operational integration.

Selective portfolio expansion also continues with an eye toward orphan drug designations that may confer regulatory exclusivity benefits enhancing potential market value—an established approach for niche oncology indications favored by clinical developers for improved reimbursement prospects [S14].

Research and Development Spending: Resource Allocation Choices Post Streamlining

Reflective of the operational focus shift described earlier, Aptorum reduced R&D expenditures dramatically—to approximately $0.6 million for FY2025 compared to over $2.2 million in FY2024 and more than $5 million at its peak before streamlining [F1][S9][S10]. These figures include contract research organization fees paused alongside sponsored research programs previously supporting non-lead compounds.

Capex remains minimal (~$3K annually), consistent with an asset-light pharmaceutical model emphasizing outsourcing over infrastructure investments [F1][S13]. Efficiency gains ensued not just from project suspensions but also cuts in depreciations related to long-lived assets previously impaired or written down reflecting legacy facilities no longer used post-clinic service termination.

This tighter cost structure illustrates the company's efforts at operational discipline necessary for sustaining clinical development cycles within severely constrained budgets.

Governance Amidst Risks: Internal Controls and Execution Challenges

Aptorum disclosed ongoing material weaknesses in internal financial controls contributing to ineffective disclosure controls as per its internal assessment notwithstanding belief that financials fairly present operations within materiality bounds [S1][S15]. Such deficiencies raise concerns around transparency reliability critical for investor confidence especially around complex transactions such as mergers.

The risk factor disclosures also cite active litigation related to alleged securities fraud claims which management firmly disputes but which represent contingent legal uncertainties nonetheless [S15]. These factors collectively underscore elevated governance risks typical of small-cap biotechnology firms undergoing transformative corporate actions amidst regulatory scrutiny.

Outlook and Key Milestones to Monitor in 2026

Although explicit management guidance remains absent from available filings or news releases, stakeholders should monitor several high-impact catalyst tracks defining Aptorum’s near-term prospects:

- Clinical trial results or IND filings advancing lead candidates ALS-4 and SACT-1 signaling technical validation.

- Successful closing and operational integration of the DiamiR merger which would broaden technological platform exposure.

- Subsequent capital raises or convertibles that sustain cash runway given continuing negative free cash flows close to $1.84 million annually net of minimal capex [F1].

- Resolution or progress regarding ongoing litigation impacting financial risk profile.

These developments collectively will influence whether Aptorum can bridge its critical liquidity gap while progressing towards proof-of-concept milestones needed for commercial viability.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 431378 | -1 | -2 | 3015 | 0.0% | +68.1% |

| 2024 | 431378 | -4 | -1 | 3015 | 0.0% | -51.1% |

| 2023 | 431378 | -3 | -8 | 3015 | +75.5% | |

| 2022 | -12 | -12 | 186916 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -5.9 |

| 2024 | -1 | -20.2 |

| 2023 | -8 | -11.4 |

| 2022 | -13 | -73.4 |

Source: SEC companyfacts cache [F1].

This table highlights revenue stability alongside marked improvements in net loss from FY2024 onward attributed mainly to expense reductions stemming from pipeline focus adjustments discussed above.

Disclaimer: This analysis is based exclusively on information publicly disclosed through Aptorum Group Ltd's SEC filings and recent news reports as cited; it does not constitute investment advice or any recommendation regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments