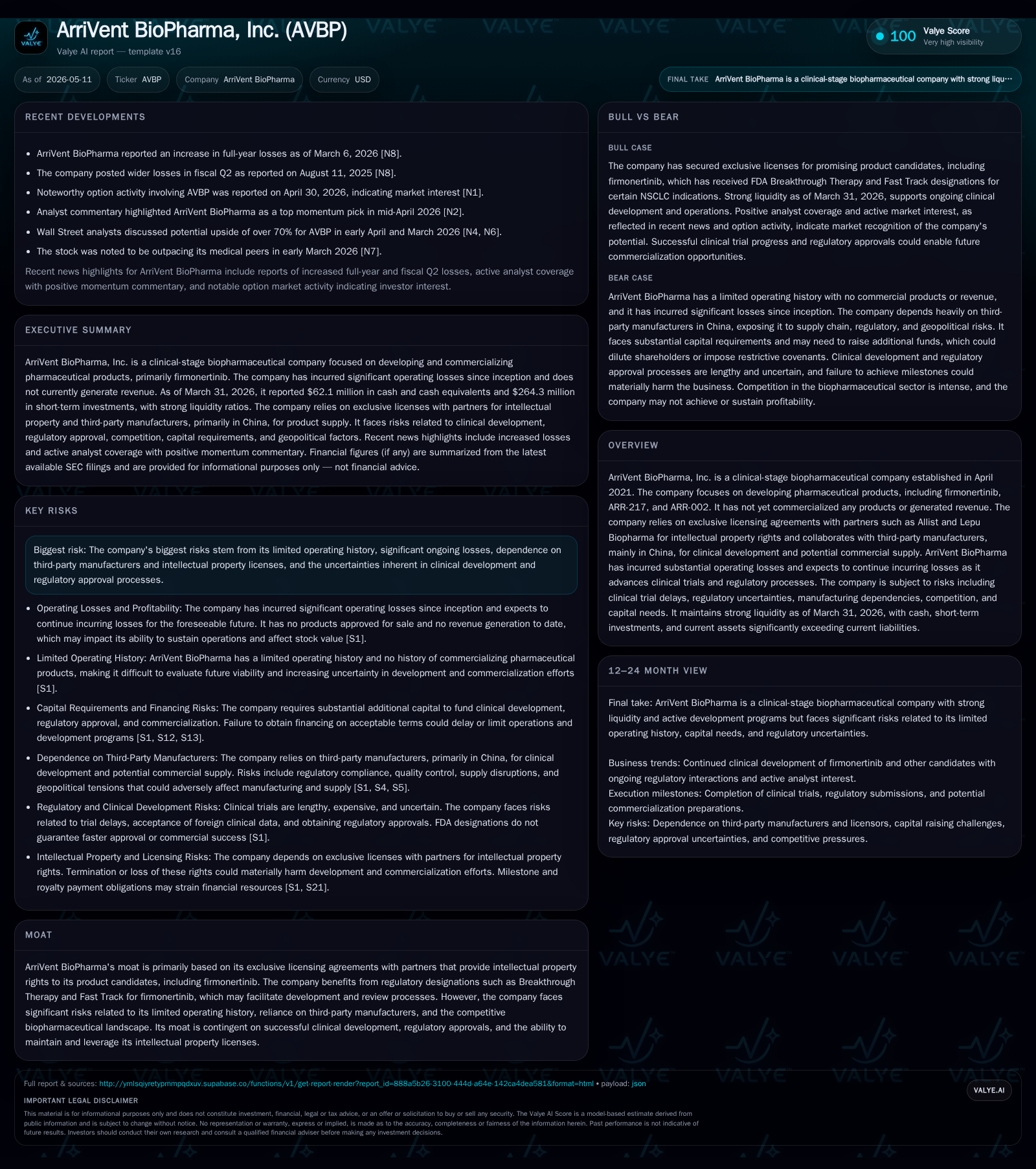

ArriVent BioPharma Focuses on Firmonertinib Development and Manufacturing Risks

Clinical-stage progress on firmonertinib advances while reliance on Chinese CMOs and ongoing cash burn frame critical operational challenges.

ArriVent BioPharma’s latest quarterly report confirms continued clinical advancement of its lead candidate, firmonertinib, alongside other pipeline assets. The company remains pre-revenue, supported by exclusive licensing agreements with key partners Allist and Lepu Biopharma, and depends heavily on third-party manufacturing predominantly based in China. With solid liquidity as of March 2026, ArriVent faces typical biopharma risks including trial delays, regulatory uncertainty, and capital requirements that could constrain long-term growth absent successful clinical outcomes or additional funding.

Latest Quarterly Operating Update: Key Developments and Impact

ArriVent BioPharma’s Q1 2026 Form 10-Q filing dated May 11 discloses ongoing advancement of its lead candidate firmonertinib alongside the ARR-217 program [S2]. The company reported no commercialization or revenue generation to date but reaffirmed its progression through clinical stages primarily supported by its licensed technology portfolio. The concurrent 8-K filing the same day supplements this update by confirming liquidity status and reiterating management’s focus on executing pivotal trial activities [S3]. Notably, ArriVent continues to rely on third-party manufacturers principally located in China to supply clinical materials — a factor flagged as a material dependency in recent disclosures due to potential geopolitical and supply chain sensitivities [S1][S18].

These filings collectively underscore ArriVent’s operating reality as a capital-intensive, development-focused entity with no current product revenues yet advancing towards critical data-reading milestones that will validate or invalidate its investment thesis. The recent disclosures affirm a stable runway enabling continued progress but caution about inherent risks tied to manufacturing dependencies and regulatory complexity remain manifest.

Product Pipeline and Business Model: Exclusive Licensing and Clinical Focus

Founded in April 2021, ArriVent centers its business model on the clinical development of pharmaceutical candidates such as firmonertinib (the foremost asset), ARR-217, and ARR-002. The company operates primarily through exclusive licensing agreements with partners such as Allist and Lepu Biopharma that grant it intellectual property rights essential for development efforts [S1][F1]. This structure allows ArriVent to leverage externally developed compounds while focusing resources on progressing clinical trials and navigating regulatory pathways rather than early-stage discovery.

Firmonertinib targets oncology indications and carries regulatory designations including Breakthrough Therapy and Fast Track status granted by the FDA — tools designed to accelerate review timelines based on unmet medical need [S1]. The pipeline remains non-commercialized at this stage; hence, customer adoption is prospective contingent upon regulatory approvals followed by uptake by healthcare providers. Margins are anticipated to pivot markedly upon transition from trial material production (via outsourced Contract Manufacturing Organizations or CMOs mainly in China) to scaled commercial manufacturing.

The licensing model creates dependency on counterparties both for intellectual property continuity and manufacturing supply reliability. Contracted manufacturers supply APIs and formulations used in human studies today but produce at scale commercially pending approvals. This outsourcing strategy reduces fixed capital burdens but introduces risks around capacity constraints, quality control variabilities, as well as potential geopolitical or tariff-driven cost pressures given the heavy reliance on Chinese incumbents [S1][S18].

Competitive Landscape and Industry Dynamics: Positioning in Biopharma

ArriVent navigates an intensely competitive biopharmaceutical industry characterized by high R&D costs, stringent regulatory standards, and complex patent environments [S1][S4][S5]. Exclusive licensing offers partial moat protection but hinges critically on maintaining intact IP rights amid evolving patent challenges common across oncology therapeutics [S16]. Moreover, international pricing pressures pose structural headwinds; government-imposed price controls in non-U.S. markets may compress future revenue potential even if regulatory approvals are secured [S4].

The company must also contend with challenges intrinsic to drug development ecosystems — competing firms often pursue similar molecular targets or indications creating first-to-market advantages or therapeutic superiority battles. These dynamics require agile clinical execution alongside effective patent defense strategies [S1][S16]. Supply chain complexities introduce further competitive tension because stable commercial-scale manufacturing is indispensable for market penetration; any disruption or cost inflation stemming from reliance on Chinese CMOs could erode pricing flexibility or delay product launches [S18].

Growth Drivers: Clinical Milestones, Regulatory Designations, and Partner Ecosystem

Clinical trial readouts represent the primary growth catalyst for ArriVent. Positive efficacy/safety data from firmonertinib’s pivotal trials could unlock pathways for NDA submissions potentially accelerated by existing Breakthrough Therapy designations [S1][S2]. Similarly, ARR-217 development progress expands the pipeline's breadth.

Regulatory designations provide tangible benefits: they enable more frequent interactions with FDA reviewers, eligibility for rolling submissions reducing time-to-decision windows, and can influence investor sentiment favorably during development phases [S1]. The company's ecosystem anchored by Allist and Lepu Biopharma adds scalability through shared IP resources but also imposes obligations such as milestone payments or profit-sharing that impact net returns post-commercialization.

Successful navigation of these milestones impacts patient access scope—approval in major markets broadens provider willingness to prescribe while payer coverage increasingly conditions ultimate utilization rates. Hence, aligning trial designs with payer evidence requirements becomes relevant beyond regulatory approval alone [S4].

Risks and Challenges: Trial Delays, Manufacturing Dependencies, and Capital Needs

ArriVent faces multifaceted risks emblematic of early-stage biopharma companies coupled with unique vulnerabilities stemming from its operational model:

- Clinical Trial Uncertainties: Suspensions, slow enrollment rates especially given overseas trial sites (notably China), adverse events or suboptimal trial outcomes may derail timelines significantly affecting capital efficiency and market expectations [S1][S7].

- Manufacturing Dependencies: Outsourcing active pharmaceutical ingredient (API) production predominantly to Chinese CMOs heightens susceptibility to supply chain disruptions due to geopolitical tensions or logistical hurdles which could delay production schedules impacting ongoing trials or future launches [S18].

- Capital Horizon: Despite possessing over $62 million cash reserves as of March 31, 2026 with a healthy current ratio near 14x providing a buffer for short term operations ([F1]), continued accrual of operating losses necessitates periodic financings exposing shareholders to dilution risk; failure to secure favorable capital could force scaling back R&D programs [S13][F1].

- Regulatory Environment: Compliance complexities span evolving U.S. federal statutes addressing drug marketing practices alongside foreign pricing regulations that may constrain launch economics profoundly forcing careful market entry strategies [S4][S5][S14][S20].

- Intellectual Property Litigation: Exposure to infringement claims or patent disputes remains high inducing costly litigation risk potentially jeopardizing exclusivity that underpins commercial value propositions [S16][S17].

These considerations underline an inherently binary risk profile where value destruction occurs if clinical/regulatory hurdles prove insurmountable versus significant upside upon product approvals.

Upcoming Catalysts and Monitoring Points: What Investors Should Watch

Key milestones ahead center largely around trial data availability for firmonertinib—both interim safety updates influencing enrollment momentum plus definitive efficacy endpoints readouts expected over next quarters per disclosure trends [S2]. Attention should focus also on management commentary related to recruitment pace within multi-regional trials since patient retention remains challenging especially outside the U.S.

Regulatory feedback episodes such as End-of-Phase meetings with FDA or advisory committee interactions constitute important junctures potentially recalibrating approval timelines or required evidence standards.

Partnership developments including expansions or amendments expanding license territories or introducing new product rights will materially affect long-term strategic ambitions.

Liquidity metrics warrant continuous observation given funding demands inherent in late-stage clinical programs—burn rates compared against remaining cash reserves foreshadow timing for subsequent capital raises which inherently create valuation pressure points.

Shifts impacting manufacturing alliances—whether diversifying away from single geography dependencies or onboarding new CMO relationships—should be viewed as key operational risk mitigants enhancing supply stability.

Financial Profile: Strong Liquidity Supports Continued Development

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $62mm | |

| 2026-03-31 | ||

| Current assets | $349mm | |

| 2026-03-31 | ||

| Current liabilities | $25mm | |

| 2026-03-31 | ||

| Current ratio | 13.95x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, ArriVent reported cash and equivalents totaling approximately $62.1 million with current assets at $348.7 million against current liabilities near $25.0 million yielding a strong current ratio near 13.95x reflecting comfortable short-term solvency [F1]. While operating income was negative trailing at -$177.5 million reflecting ongoing developmental spend typical for pre-commercial biopharmaceutical firms [F1], this cash position affords runway into subsequent quarters allowing management focus squarely on delivery of clinical milestones without immediate liquidity distress.

Despite this robust liquidity buffer nominally mitigating solvency concerns short term, sustained losses underscore the necessity of accessing additional capital internally or via partnerships eventually to fund registration-enabling studies required for commercialization scale-up consistent with disclosed risk narratives [S13]. Control over capital structure remains paramount given dilution effects inherent in equity financing rounds customary at this corporate stage.

This analysis strictly reflects facts disclosed within recent SEC filings dated May 11, 2026 ([S2],[S3]) supplemented by foundational details from the March 5 annual report ([S1]) alongside confirmed financials ([F1]). No forward-looking investment recommendations are made herein — readers should incorporate additional sources when assessing full equity appraisal.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments