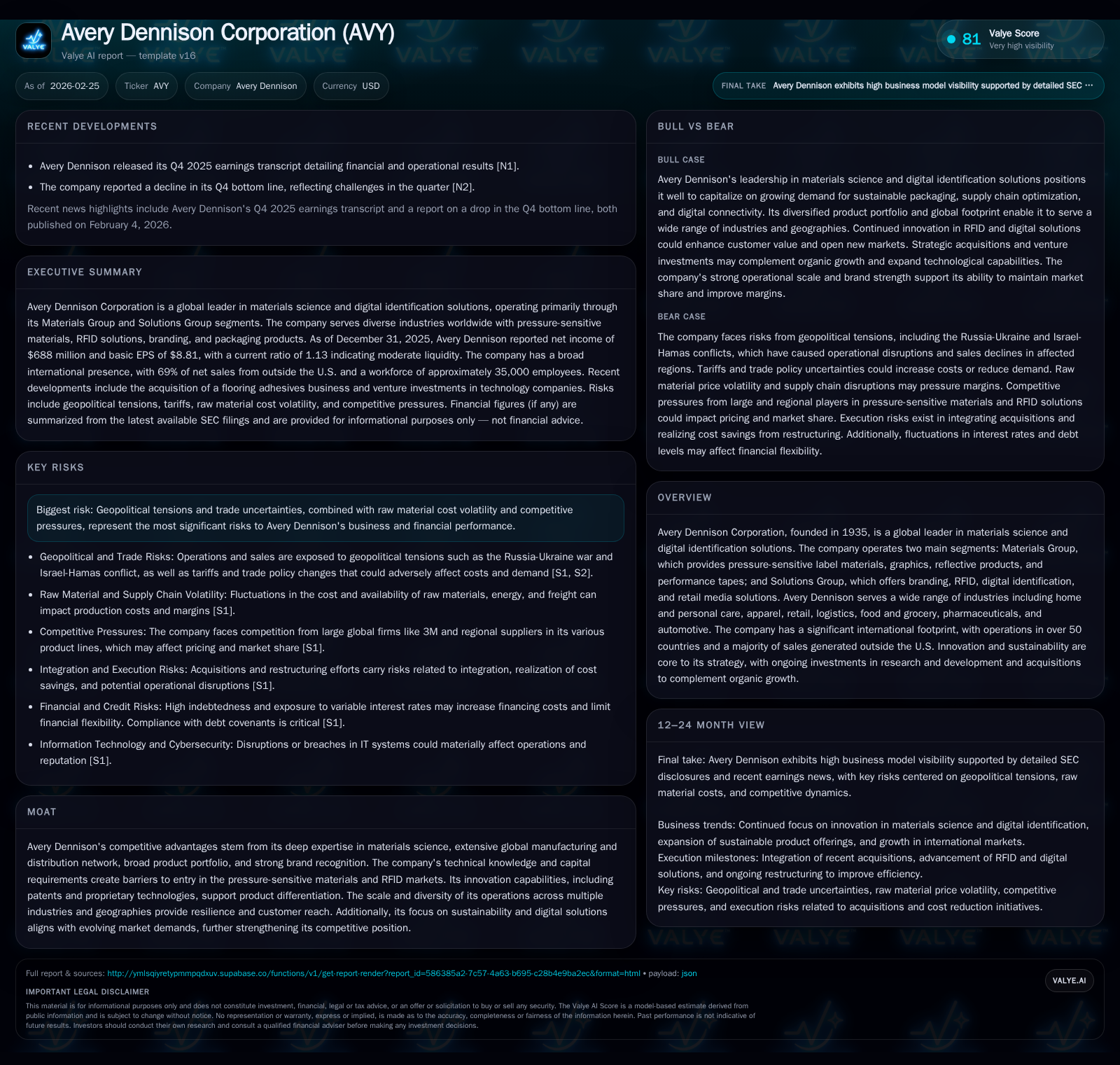

Avery Dennison’s Growth Balances Innovation Investment and Geopolitical Trade Challenges

Examining Avery Dennison's financial trajectory, segment dynamics, and risk profile as it advances materials science and digital identification solutions.

Avery Dennison, a materials science and digital ID leader with a diversified global footprint, exhibited steady net income growth tempered by macroeconomic and trade uncertainties through 2025. Its dual-segment model—Materials Group and Solutions Group—drives innovation and sustainability initiatives to serve broad industries. While the company’s capital allocation reflects disciplined cash returns and investment in R&D and infrastructure, its growth faces limits from geopolitics, tariff volatility, and raw material cost fluctuations. Monitoring customer consolidation effects, evolving supply chain constraints, and digital adoption trends should inform outlook assessments.

Company Overview and Historical Performance

Founded in 1935, Avery Dennison is a longstanding innovator at the nexus of materials science and digital identification solutions. Its two primary segments—Materials Group (pressure-sensitive label materials, graphics, reflective products, performance tapes) and Solutions Group (branding embellishments, RFID tags/inlays, digital retail media)—cover broad industry verticals including apparel, pharmaceuticals, automotive, food/grocery, logistics, home/personal care, and retail [S1][S16].

By fiscal year-end 2025, approximately 69% of net sales derived from international operations across more than 50 countries underscoring a significant global footprint [S1]. The company operates over 200 manufacturing and distribution sites worldwide.

Financial Summary

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 688 | 881 | 169 | -2.4% |

| 2024 | 705 | 939 | 209 | +40.1% |

| 2023 | 503 | 826 | 265 | -33.6% |

| 2022 | 757 | 961 | 278 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 288 | 572 | 712 |

| 2024 | 278 | 248 | 730 |

| 2023 | 257 | 138 | 561 |

| 2022 | 239 | 380 | 683 |

Source: SEC companyfacts cache [F1].

*YoY percentages calculated where data available; **Sharp YoY fluctuations reflect partial recovery post-pandemic disruptions.

Net income demonstrated resilience despite external pressures but saw a slight decline in fiscal ’25 compared to ’24 [F1]. Operating cash flow declined moderately while capital expenditure reductions signal a cautious approach amid uncertain demand conditions [F1][S5]. Approximately $137 million was allocated to R&D expenditures mainly toward materials innovation and intelligent label technologies [S5][S9].

Segment Dynamics

Materials Group

This segment accounted for roughly two-thirds of total net sales in fiscal ’25 [S1]. It supplies label materials that aid brand visibility and operational efficiency. Products include Fasson® pressure-sensitive labels serving industries requiring circular economy enhancements such as recyclability of packaging [S1][S20]. The group also provides industrial tapes used across automotive construction and electronics sectors.

Competition here is characterized by technical complexity involving adhesive chemistry and coating processes that require substantial capital investment acting as an entry barrier [S20]. Prime competitors are large diversified chemical companies like UPM Adhesive Materials (UPM), Fedrigoni Self-Adhesives, Lintec Corp., as well as regional tape producers shaping a fragmented competitive landscape [S20].

Solutions Group

Constituting about one-third of revenue in ’25 [S1], Solutions offers digital identification via RFID technology enabling physical products to connect to the digital ecosystem for tracking and consumer engagement purposes [S16][S20]. This group also supplies branding embellishments such as graphic tickets and tags which add consumer appeal.

Key competitors include Checkpoint Systems (subsidiary of CCL Industries), R-pac International Corporation, SML Group Limited among others with specialization in RFID or security tags technology [S16]. The segment's growth is driven by increasing adoption of IoT solutions in retail inventory management accelerated by omnichannel retailing demands.

Growth Prospects and Risks

Drivers

Avery Dennison is pursuing growth by expanding its high-value product mix emphasizing sustainable innovations — recyclable materials with reduced waste footprints — aligned to societal demand for circular economy principles [S9][S16]. The expansion into emerging markets remains central; approximately forty percent of sales originate from these regions where rising consumer goods penetration supports demand growth despite episodic volatility [S25].

The company’s acquisition strategy complements organic initiatives — notably the $390 million purchase of Taylor Adhesives in late ’25 bolsters its industrial adhesives portfolio targeting flooring applications [S9]. Additional venture investments aim to develop advanced digital identification capabilities further enhancing solutions offerings.

Constraints & Risks

Geopolitical uncertainty poses persistent challenges: In ’25 Avery Dennison was impacted by newly imposed U.S. tariffs on imports (10-15%), especially affecting apparel-related product volumes which led to low single-digit percentage declines within affected categories during several quarters [S1][S22]. Tariff reciprocity measures among major trading partners contribute to demand softness downstream.

Emerging market operations entail exposure to inflationary pressures on raw materials/energy plus labor shortages disrupting production schedules occasionally [S1][S22][S25]. Currency fluctuations further complicate earnings visibility even though hedging policies provide partial mitigation.

Intense competition requires continuous investment in innovation for both segments given rapid advances in RFID technologies competing against firms with comparable scale or specialized IP portfolios [S16][S20]. Vertical integration moves among converter customers also pressure pricing leverage margins necessitating efficiency enhancements.

Climate-related risks have pushed Avery Dennison beyond its initial environmental goals — it achieved nearly a ~60% absolute reduction in scope-1/2 emissions relative to a baseline year of ’15 — now targeting a further ambitious cut exceeding twice the prior goal magnitude by ’30 [S12][S26]. Compliance costs for environmental regulations remain significant but viewed as intrinsic to brand value preservation.

Capital Allocation and Returns Analysis

The company maintains a consistent shareholder return discipline via dividends supplemented by aggressive share repurchase programs; $575 million spent buying back shares in ’25 alone under a $750 million authorization renewed earlier that year leaving ~$526 million available going forward [S4][F1]. Dividends rose approximately seven percent in April ’25 continuing an upward trend reflecting steady free cash flow generation.

Return on equity remains robust at approximately ~31%, consistent with historical levels underscoring efficient capital use despite commodity cyclicality facing the business model [F1]. Free cash flow—operating cash flow less capex—totaled around $712 million for fiscal ’25 indicating strong internal funding capacity for both growth investments and capital returns [F1].

Outlook Considerations (Analysis)

Absent explicit guidance details beyond Q4 ’25 results conference calls issued early February ‘26[ N2–N8], key metrics warrant close observation going forward:

- Inventory adjustments post-pandemic normalizations downstream impacting reorder frequencies,

- Accelerated rollout velocity of RFID-based intelligent label programs driving incremental Solutions revenue,

- Raw material input cost trajectories influencing pricing strategies,

- Trade policy developments potentially altering tariff landscapes impacting apparel-related volumes,

- Integration success from Taylor Adhesives acquisition enhancing industrial tapes product offering,

- Customer consolidation effects influencing bargaining power dynamics. These factors together will frame Avery Dennison’s capacity to mitigate current geopolitical complexities while leveraging its technological moat.

Conclusion

Avery Dennison navigates an intricate interplay between durable scientific innovation leadership and evolving international trade challenges. Its expansive global presence affords diversification benefits but simultaneously exposes it to macroeconomic headwinds requiring active supply chain agility. Strong capital management evidenced through disciplined buybacks alongside sustained dividend growth complements ongoing strategic investments into next-generation labeling technologies including RFID digital identity platforms. The twin engines of proprietary material sciences expertise combined with digital identification solutions position Avery Dennison well against competitive forces while underscoring continued reliance on operational excellence amid shifting regulatory requirements. Stakeholders monitoring this firm must weigh the balancing act between sustaining R&D momentum fostering future growth avenues against prevailing tariff uncertainties capping near-term volumes primarily within apparel segments.

Disclaimer: This analysis is based exclusively on publicly available information including SEC filings up to February 2026 and relevant news transcripts. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments