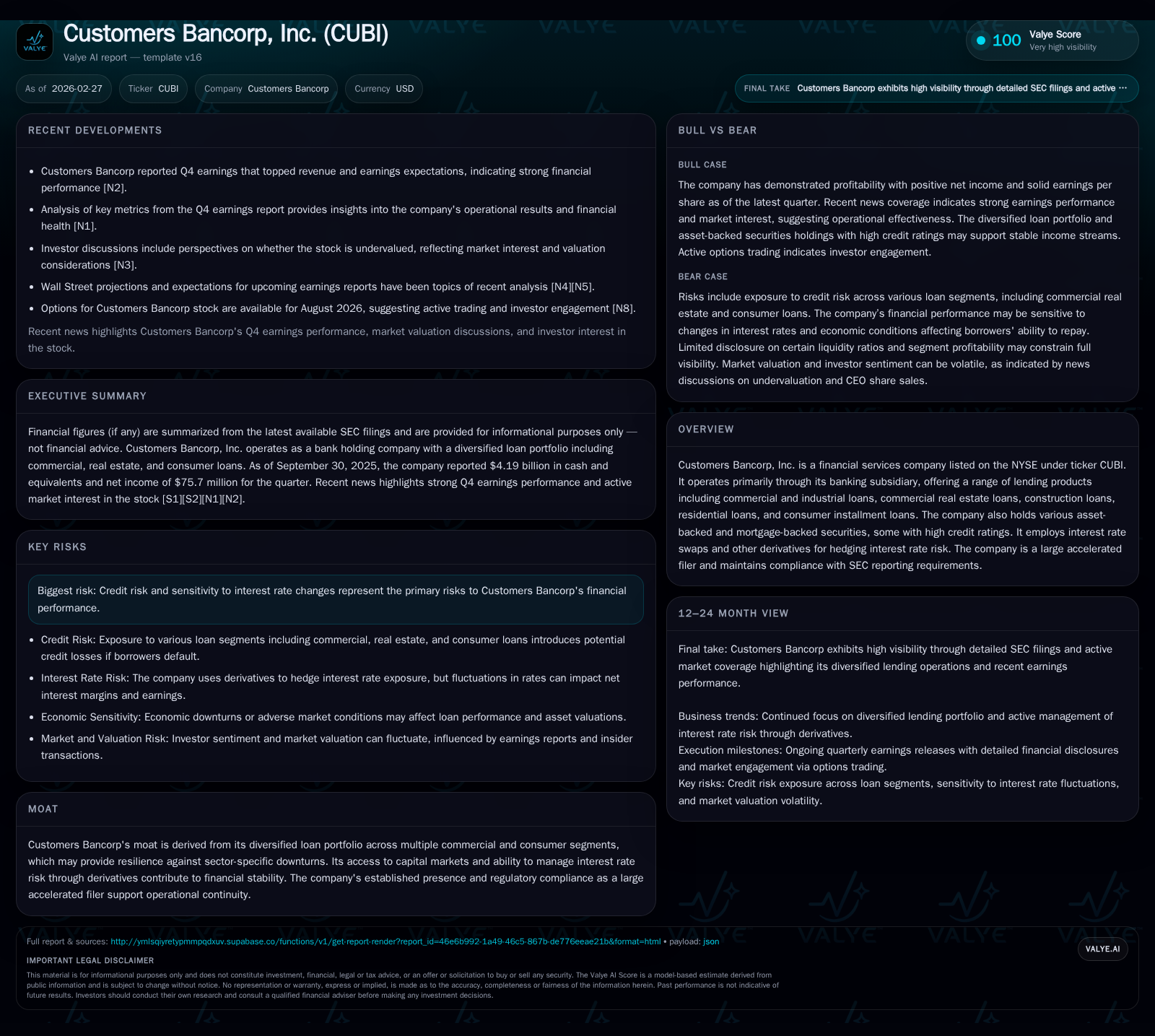

Customers Bancorp’s Growth Momentum and Capital Strategy in a Shifting Rate Environment

A detailed examination of how Customers Bancorp’s diversified lending, effective interest rate risk management, and strategic capital allocation contribute to its recent financial performance and outlook.

Customers Bancorp posted a robust 23.5% increase in net income for FY2025 compared to the prior year, driven by strong operating cash flow growth and focused capital expenditures. Its diversified loan portfolio spanning commercial, real estate, construction, residential, and consumer lending underpins resilient growth, supported by high-quality asset-backed securities. The company manages interest rate sensitivity through strategic use of derivatives like interest rate swaps, enhancing earnings stability amid volatile markets. Prudent capital structure management ensures liquidity with substantial cash reserves and staggered debt maturities. A fresh $100 million share repurchase program signals disciplined capital deployment balanced with growth investment. Looking ahead, loan demand trends and credit risk evolution remain key variables to monitor for sustaining momentum.

Financial Performance Trends: Accelerating Net Income and Cash Flows

Customers Bancorp delivered a solid financial performance in FY2025 with net income ascending to approximately $224 million, marking a 23.5% increase from $181 million recorded in FY2024 [F1]. This upward trajectory underscores operational improvements aligned with strategic initiatives focusing on revenue diversification and disciplined expense management. Notably, operating cash flow experienced a striking jump of over 240%, rising to nearly $495 million from $145 million the prior year [F1]. This surge highlights the quality of earnings improving alongside core business expansion.

While capital expenditures also rose significantly—over eightfold compared to FY2024—they remain moderate at around $13.7 million relative to cash flow availability [F1]. This investment pattern suggests targeted reinvestment into technology or branch infrastructure to support further organic growth rather than broad capex acceleration.

Equity expanded steadily to more than $2.1 billion by fiscal year-end 2025, contributing to an approximate return on equity (ROE) of 10.6%, demonstrating respectable profitability within a competitive banking sector landscape [F1]. This ROE level reflects efficient utilization of equity capital consistent with mid-sized banks maintaining solid risk-return trade-offs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 224 | 495 | 14 | +23.5% |

| 2024 | 181 | 145 | 1 | -27.5% |

| 2023 | 250 | 1 | +771.2% | |

| 2022 | 29 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 6 | 481 | 10.6 |

| 2024 | 19 | 144 | 9.9 |

| 2023 | 40 | 15.3 | |

| 2022 | 33 | 2.0 |

Source: SEC companyfacts cache [F1].

Approximate ROE calculated as Net Income divided by Equity for each respective year [F1]

Diversified Loan Portfolio: The Foundation of Resilient Growth

Customers Bancorp's principal strength lies in its diversified lending platform encompassing multiple verticals: commercial & industrial loans, commercial real estate (both owner-occupied and non-owner occupied), construction loans, residential mortgages, and consumer installment products [S1][S5]. By distributing credit exposure across these sectors, the bank mitigates concentration risk inherent in cyclical downturns affecting specific industries.

Within the asset portfolio, holdings of agency-guaranteed commercial mortgage-backed securities (CMBS), residential mortgage-backed securities (RMBS), collateralized mortgage obligations (CMOs), and asset-backed securities (ABS) carry predominantly high credit ratings — including AAA and AA categories — which enhances overall balance sheet credit quality and regulatory standing [S5]. This layered approach allows flexibility in managing both liquidity needs and interest rate risk.

Notably, the company segments its commercial real estate exposures carefully between owner-occupied properties—typically more stable due to occupant investment—and non-owner occupied properties—which may carry higher volatility but offer yield opportunities when carefully managed through underwriting discipline [S15]. Construction lending remains an important component but is monitored closely given sensitivity to economic cycles affecting development activity.

Interest Rate Hedging and Risk Management in Action

In light of shifting monetary policy landscapes characterized by periods of rate volatility, Customers Bancorp employs interest rate derivatives including swaps as part of an active duration gap management strategy designed to cushion net interest margin (NIM) fluctuations caused by timing mismatches between asset yields and funding costs [S1][N4].

This tactical use of interest rate swaps serves as a hedge against rising rates that might otherwise compress margins on fixed-rate assets funded by variable deposits or short-dated liabilities—a common risk vector for banks with diverse loan books combining fixed- and floating-rate loans. Moreover, such derivatives can smooth earnings volatility stemming from rapid market adjustments while maintaining compliance with hedge accounting regulations.

By integrating these instruments within its asset-liability management framework, Customers Bancorp enhances earnings predictability—an increasingly critical attribute favored by investors amidst uncertain macroeconomic conditions impacting bank stocks broadly.

Capital Structure Overview: Debt Maturity Profile and Liquidity Position

The company's debt structure features subordinated notes staggered over time, with key maturities extending well into the early-to-mid-2030s—including notable issues scheduled for August 2031 and December 2034—as documented in recent SEC filings [S4][S5]. This maturity ladder reduces refinance pressure near-term while locking in funding at fixed rates beneficial during volatile credit markets.

Liquidity remains robust with cash and equivalents reported at roughly $4.41 billion as of fiscal year-end 2025—providing ample headroom for operational needs or opportunistic deployments without reliance on external capital markets under stressed conditions [F1].

Additionally, the company maintains access to Federal Home Loan Bank advances alongside deposits diversified across retail and commercial clients that collectively underpin funding stability supportive of ongoing lending activity [S16][S25].

Such prudent liquidity and capital configuration are crucial for meeting regulatory requirements as a large accelerated filer while sustaining strategic flexibility amid evolving interest rate regimes.

Share Repurchases and Dividend Policies Reflect Strategic Capital Allocation

On February 11, 2026, Customers Bancorp announced a new common stock repurchase program authorizing buybacks up to $100 million over one year—a move reinforcing commitment to returning cash to shareholders where accretive after funding growth initiatives [S3].

Historical data shows variability in buyback volumes — $19 million was expended in fiscal year 2024 compared with lower outlays around $5.6 million in FY2025 — indicating responsive deployment tied closely to prevailing market valuations and internal cash flow generation capacity [F1].

Dividend policy continues alongside repurchases maintaining balanced capital returns without compromising equity cushions underpinning an approximate ROE surpassing 10%—a level reflective of targeted profitability standards within mid-sized banking institutions leveraging diverse loan books [F1].

Such measured capital allocation favors sustaining growth investments while rewarding shareholders amid cyclical headwinds characteristic of contemporary banking environments.

Future Outlook: Expected Growth Drivers and Headwinds to Monitor

Absent explicit forward guidance beyond Jan-Feburary news releases, industry-watchers should focus on shifts in aggregate loan demand—especially within commercial real estate construction where economic cyclicality can sharply influence origination volumes—and evolved credit loss provisions as leading indicators relevant for assessing future earnings trajectories [N3][N6].

Economic conditions influencing yield curves will also directly impact net interest margins post-hedging cost considerations; thus monitoring NIM trends remains essential alongside default rates within diverse lending segments highlighted previously as sensitive risk factors [N6].

Further regulatory changes or macroprudential pressures remain possible wildcards that could recalibrate industry competitive dynamics or cost structures affecting medium-term growth potential.

Key Metrics to Watch Ahead of Upcoming Earnings Releases

Investors should closely observe quarterly updates emphasizing loan portfolio growth rates segmented by product line, changes in provision expense tied to credit quality shifts reflected in nonperforming assets ratios, net interest margin evolution including hedging effectiveness reflections, as well as capital return activities such as actual repurchase execution relative to authorization limits disclosed recently [N6].

These KPIs provide crucial transparency into how Customers Bancorp navigates the intersection of economic cycles, regulatory expectations, and market demand nuances—informing expectations on whether current growth momentum will maintain or face moderation.

-- This analysis is based solely on publicly available filings ([F1],[S#]) and reported market news ([N#]) as of February–March 2026 without incorporating forward-looking statements from management beyond cited sources; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments