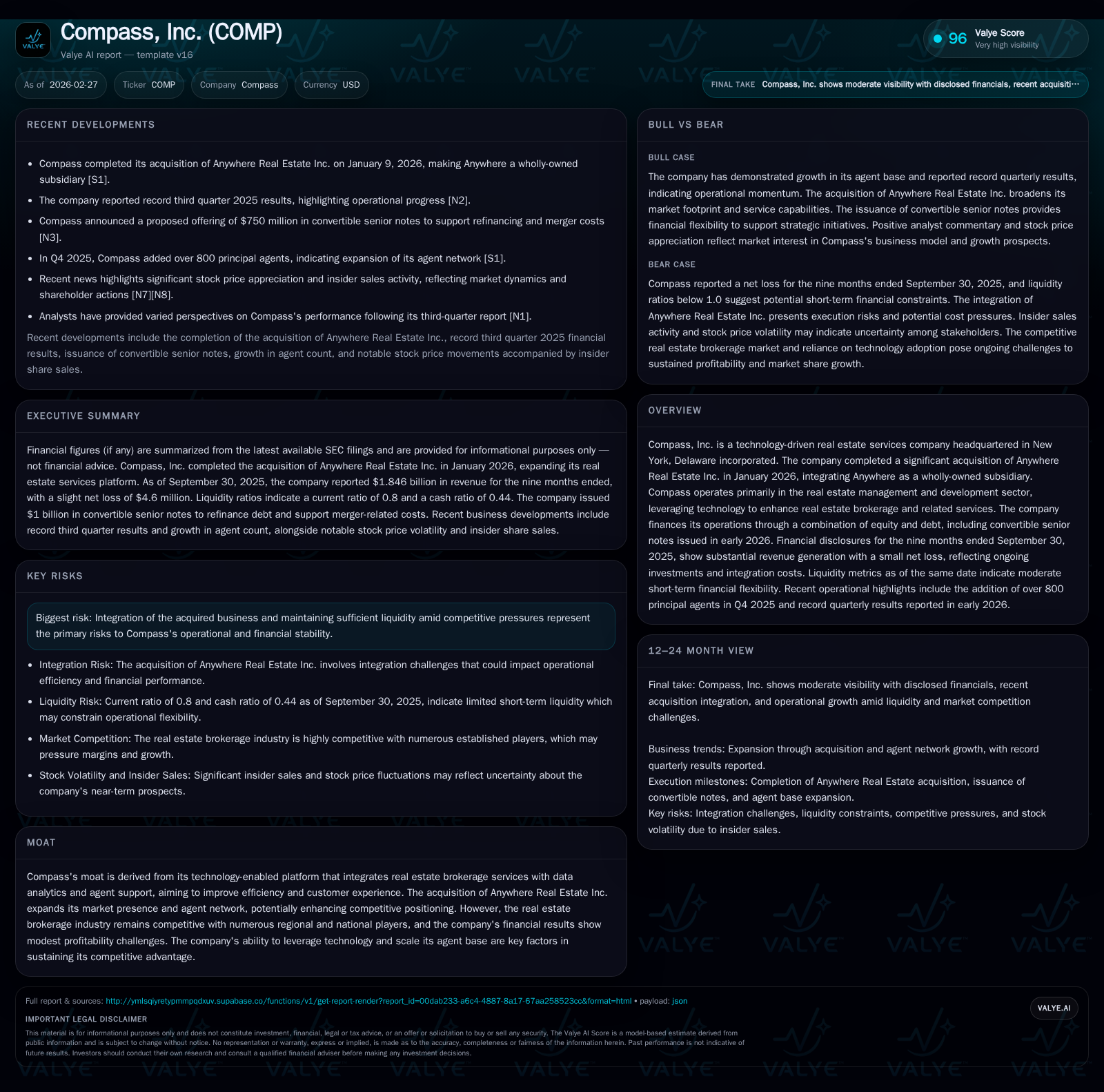

Compass Inc. Scales U.S. and Global Reach via Anywhere Merger While Managing Profitability Pressures

The completion of the Anywhere Real Estate acquisition significantly expands Compass's agent network and global footprint amid ongoing operating losses and integration challenges.

Compass, Inc., a technology-enhanced real estate brokerage, completed its acquisition of Anywhere Real Estate in January 2026, resulting in a combined network of over 340,000 real estate professionals across major U.S. cities and approximately 120 countries. The merger broadens brand portfolio and integrated services offerings but adds near-term complexity including integration costs. Despite robust revenue growth—up 23.7% to $6.96 billion in 2025—operating income remained negative, though losses narrowed from prior years. Compass finances expansion with a new $1 billion convertible notes issuance and maintains moderate liquidity. The firm's growth hinges on successful agent retention, technology leverage, and synergies realization amid competitive real estate markets and regulatory risks.

Company Overview and Industry Position

Compass, Inc., incorporated in Delaware and headquartered in New York City since its founding in 2012 as Urban Compass, operates as a technology-driven real estate services firm with an extensive brokerage platform enhanced by proprietary data analytics and agent tools [S1]. Its business model aligns closely with independent contractor real estate agents operating under multiple flagship brands including Compass itself as well as Coldwell Banker, Sotheby’s International Realty, Corcoran, @properties among others following recent expansions.

The company’s strategic direction notably intensified after completing the acquisition of Anywhere Real Estate Inc. on January 9, 2026 [S19], which propelled Compass into a leading global player spanning every major U.S. city and approximately 120 countries with over 340,000 affiliated real estate professionals [S1]. This combination brings together Compass’s owned-brokerage operations with Anywhere’s franchise-heavy portfolio under recognizable names like Better Homes & Gardens Real Estate, Century 21, Christie’s International Real Estate alongside Coldwell Banker and others.

Historical Financial Performance

Compass has shown notable top-line acceleration in recent years despite facing operating losses throughout the period:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 7.0 | -58 | 217 | -63 | +23.7% | +62.1% |

| 2024 | 5.6 | -154 | 122 | -155 | +15.2% | +51.9% |

| 2023 | 4.9 | -321 | -26 | -315 | -18.8% | +46.6% |

| 2022 | 6.0 | -601 | -292 | -589 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 203 | -7.5 |

| 2024 | 106 | -37.7 |

| 2023 | -37 | -74.9 |

| 2022 | -362 | -116.3 |

Source: SEC companyfacts cache [F1].

Revenue grew by nearly 24% in 2025 compared to the previous year [F1]. This surge partially reflects internal organic growth bolstered by expansive agent recruitment (over 800 principals added Q4 alone) plus increased transaction volumes coincident with the company’s broadening service ecosystem [S21]. Operating losses have substantially contracted from negative $589 million in 2022 to just minus $63 million in 2025—a marked improvement attributed largely to scaling benefits offset partially by investments associated with acquisitions and product development [F1].

Net income losses also diminished significantly but remained negative at about $58.5 million in the latest fiscal year demonstrating ongoing pressure on profitability margins despite revenue scalability [F1]. Operating cash flow turned positive at $217 million reflecting improved core cash generation dynamics while capital expenditure decreased materially from peak levels during prior years [F1].

Capital Structure and Liquidity

To finance the Anywhere transaction and related refinancing efforts, Compass issued $1 billion in aggregate principal of convertible senior notes due April 2031 carrying an interest rate of only 0.25% per annum early January 2026 [S4][S5][S6][S8]. The notes feature conversion options tied to company share prices plus capped call transactions designed to limit dilution risk for shareholders [S11]. These notes are senior unsecured obligations guaranteed on a senior basis by subsidiaries aligned with existing revolver guarantors [S15][S19].

At December end, Compass maintained cash and equivalents totaling approximately $199 million alongside current assets of ~$317 million versus current liabilities near $367 million yielding a current ratio below unity at roughly 0.86—a sign of relatively tight short-term liquidity but manageable given positive operating cash flows anticipated post-merger completion [F1]. The company intends to use net proceeds from note issuance primarily to repay Anywhere debt obligations assumed at closing plus cover related fees [S4][S19].

Post-Merger Strategic Outlook

Expanded Platform Footprint

The acquisition of Anywhere creates one of the largest combined brokerage networks across owned-brokerage and franchise channels spanning over three hundred thousand agents globally—a remarkable scale advantage enhancing Compass’s ability to leverage cross-brand technology adoption, centralized marketing initiatives, data integration across markets, and broadened ancillary service distributions including title escrow and relocation services [S1][S19][S21].

Growth Drivers

Future top-line enhancement will likely stem from:

- Increased transactions through enhanced agent productivity via proprietary platform tools.

- Expansion of integrated services including mortgage joint ventures and title underwriting facilitated by Anywhere legacy businesses.

- Geographic coverage gains particularly internationally through franchises serving diverse markets.

- Incremental agent recruitment supported by multi-brand appeal.

- Synergies realized from back-office consolidations anticipated but not yet quantified publicly.

Constraints & Risks

Growth could be capped or challenged by several factors:

- The residential real estate industry remains susceptible to macroeconomic cycles such as interest rate volatility (30-year fixed mortgage rates still elevated around low-6% range early 2026) that can suppress transaction volumes materially impacting commission revenue [S1].

- Integration risks include complex consolidation of diverse agency cultures, IT systems harmonization, legal disputes pending or emerging from Anywhere acquisition including antitrust litigation settlements inherited [S7][S10].

- Competitive pressures remain intense among national brokerages plus emergence of alternative brokerage models leveraging disruptive technologies outside Compass’s ecosystem.

- Liquidity constraints if operating cash flows dip unexpectedly or capital market conditions tighten.

- Ongoing regulatory uncertainties surrounding U.S housing policies or mortgage financing regulations.

Expectations & Monitoring Indicators

While explicit forward guidance awaits finalization pending financial close for Q4 and full year reporting in early March 2026 [S3], management flagged that fourth quarter revenue would reach the high end of prior guidance ($1.59 - $1.69 billion), with adjusted EBITDA expected near or slightly above the previous top-end estimate [$35 - $49 million] indicating improving margin trends partially driven by scale effects post-merger integration steps [S21].

Key milestones to watch include:

- Completion of formal audited results post-merger for full fiscal year analysis revealing true synergy capture impact.

- Agent count growth trajectory adherence versus churn risks following large-scale integration disruptions.

- Debt servicing capacity tested via note conversion triggers or callable redemption provisions.

- Progress updates on litigation resolution related to legacy complaints against Anywhere pre-merger.

- Technology platform rollout effectiveness strengthening differentiated positioning against competitors.

Capital Allocation & Returns

There is no record of dividend payouts or share repurchases during the recent fiscal years as the firm continues reinvesting available cash flow toward scaling operations and integration costs [F1][S24][S27]. Equity saw a substantive increase from approximately $409 million at end-2024 to $782 million end-2025 reflecting infusion from new debt instruments converted partly into equity or equity components recognized with transactions tied to merger consummation process [F1].

Return on equity remains negative though improved: approximately -7.5% based on last reported net loss relative to equity base calculated for FY2025 [F1]. Free cash flow approximates $203 million (operating cash flow minus capex), suggesting improving fundamental cash returns despite accounting losses incurred under IFRS/GAAP standards conventionally used for technology investment heavy models typical within tech-enabled brokerages [F1].

Industry Context (Analysis)

The residential brokerage space is evolving rapidly where technology platform integration determines competitive survival alongside scale economics derived through agent recruitment success balancing quality service delivery against commoditization risks inherent in high transaction volume driven commission models. Elevating non-brokerage ancillary income streams such as title services—as expanded here—represents an emerging trend aimed at diversifying revenue pools amid cyclical housing markets.

Further complicating industry dynamics is increasing regulatory scrutiny related to broker commission structures highlighted through legal actions affecting former Anywhere businesses along with broader calls for transparency reforms across MLS membership compensation practices downstream impacting agent incentives dependent on commission splits.

Conclusion

Compass's strategic acquisition of Anywhere Real Estate sets up substantial platform scale enabling cross-border footprint expansion and multi-brand dominance but concurrently introduces execution complexity manifesting near-term profitability pressures visible through manageable but persistent operating losses even amid record revenue gains reported through FY2025 despite integration still unfolding at year-end.

Cash flow metrics indicate trajectory towards stabilization supported by prudent financing strategies exemplified by issuance of convertible notes with low coupon rates balancing leverage while protecting equity dilution concerns through capped calls mitigating shareholder risks inherent within capital structure decisions tied to large-scale mergers.

Going forward monitoring integration milestones balanced against macro-residential market volatility alongside regulatory/legal developments will be critical barometers shaping Compass’s path towards sustained profitability leveraging technology-enhanced real estate brokerage synergies generated from this transformative consolidation event.

This analysis is prepared solely for informational purposes based on disclosed filings without expressing any investment recommendation or forecast.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments