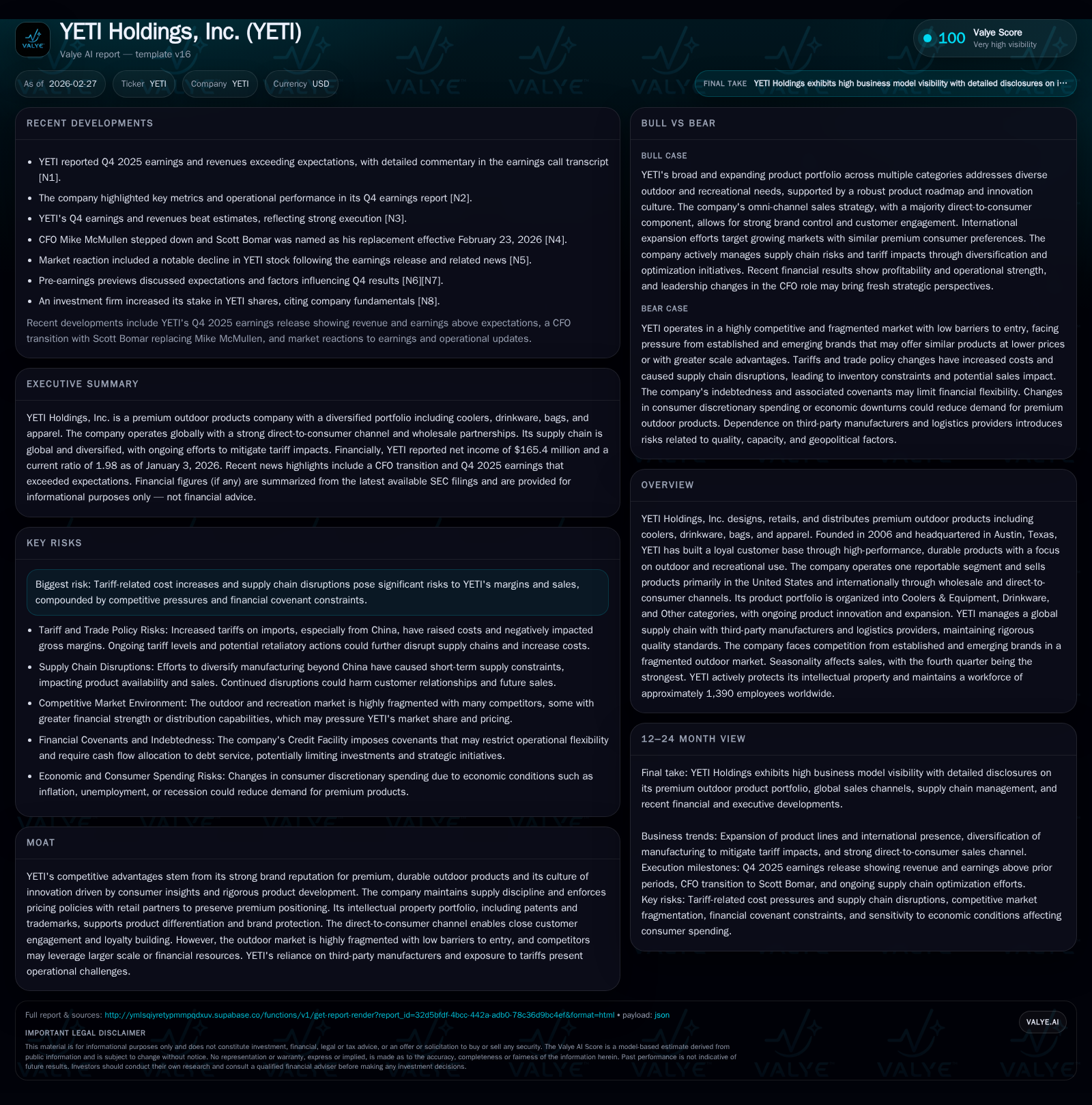

YETI Holdings Balances Premium Brand Strength with Supply Chain and Tariff Challenges

YETI’s growth leverages product innovation and DTC expansion, while tariffs and supply constraints pose margin pressures.

YETI Holdings, Inc. has established itself as a leader in premium outdoor products through strong brand equity, innovative design, and a loyal customer base. The company’s historical growth was driven by expanding its product portfolio across coolers, drinkware, and bags while growing both wholesale and direct-to-consumer channels. However, 2025 saw a contraction in operating income and net income, primarily influenced by increased tariff costs on imported goods and short-term supply chain disruptions caused by diversification away from China manufacturing. YETI faces competitive pressure in a fragmented market but continues to invest heavily in marketing, product innovation, and geographic expansion with a focus on international growth. Capital allocation remains disciplined as the company repurchased nearly $298 million of shares in FY2025 while maintaining positive free cash flow. Monitoring tariff developments, retail partner execution, inventory availability, and marketing effectiveness will be critical for YETI’s near-term trajectory.

Historical Performance

YETI Holdings has charted rapid growth since its founding in 2006 by leveraging high-performance outdoor products that resonate with enthusiasts. The company has focused on three core product categories: Coolers & Equipment; Drinkware; and Other (including bags and apparel). As of fiscal 2025 (year ended January 3, 2026), the Coolers & Equipment segment contributed approximately 40% of net sales while Drinkware accounted for about 58%, illustrating strong diversification beyond the flagship cooler offering [S4][S5].

Financially, YETI experienced strong profitability gains over recent years but encountered headwinds in FY2025. Operating income declined by 13% from $245 million in FY2024 to $214 million in FY2025. Net income also decreased by nearly 6% year-over-year to $165 million [F1]. This decline was against the backdrop of a rising cost environment marked by incremental tariffs on imported products—most notably those manufactured in China—and short-term supply disruptions tied to ongoing efforts to diversify manufacturing outside China.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 165 | 255 | 214 | 43 | -5.9% |

| 2024 | 176 | 261 | 245 | 42 | +3.4% |

| 2023 | 170 | 286 | 225 | 51 | +89.4% |

| 2022 | 90 | 101 | 126 | 46 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 298 | 212 | 25.4 |

| 2024 | 200 | 220 | 23.7 |

| 2023 | 0 | 235 | 23.5 |

| 2022 | 100 | 55 | 17.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue details for recent fiscal years are not explicitly provided; operating income and net income show a downward trend in profitability in FY2025.

Operating cash flow remained robust at $255 million with modest capital expenditure increases supporting continued investment in infrastructure and innovation. Free cash flow approximated $212 million after capex deductions [F1].

Business Overview and Competitive Position

YETI’s single reportable segment reflects integrated sales across wholesale and direct-to-consumer (DTC) channels internationally. Approximately 79% of sales occur within the United States whereas international markets accounted for around 21% in FY2025—with continued geographical expansion targeting Canada, Australia, Europe, Asia, and Japan [S4][S6]. This geographic diversity contributes to broadening consumer reach but also exposes the company to varied market dynamics.

The company’s hallmark is its premium brand anchored by unyielding product quality—exemplified by rotomolded hard coolers featuring superior ice retention—and direct involvement with outdoor communities via ‘‘YETI Ambassadors’’ spanning anglers to brewmasters to surfers. Product innovation extends into drinkware insulated technology (Rambler series) and recently introduced cookware lines encompassing cast iron and steel pans [S12][S14].

Competition exists across segments from well-established names such as Igloo and Coleman for coolers, to HydroFlask and Stanley in drinkware. The outdoor protean market is fragmented with many entrants offering competing features at varying price points. YETI's competitive moat is preserved via strict pricing discipline with retail partners who agree to uphold price integrity alongside robust intellectual property protections through patents and trademarks [S7][S9].

Growth Prospects

Despite recent margin pressures, YETI’s future growth appears hinged upon several strategic levers:

- Continued rollout of innovative products expanding the core portfolio into new categories such as outdoor living equipment.

- Geographic expansion focused on increasing penetration in international developed markets (Canada, Australia) as well as exploratory efforts into Asia where demand for premium outdoor goods is emerging [S6][S19].

- Scaling DTC sales channel which now comprises a majority of net sales (60%), enabling enhanced customer relationships, exclusivity programs including customizations, original content marketing including films and social media outreach leveraging Ambassadors [S5][S16].

- Partnerships with selective wholesale retailers aligned with YETI’s premium positioning to maintain brand authenticity.

However, future growth could be capped by:

- Sustained or escalating tariffs impacting import costs which directly pressure gross margins if not offset by price increases or supply chain improvements.

- Inventory constraints stemming from diversification efforts outside China leading to lost sales opportunities or weakened wholesale relationships.

- Heightened competition introducing lower-cost alternatives eroding market share or forcing discounts.

- Increasing capital requirements tied to scaling international operations or technology investments.

Tariff Impact and Supply Chain Management

Entering fiscal year 2025, YETI faced material cost increases due to incremental U.S. tariffs imposed on imports mostly produced outside North America—including China, Vietnam, Thailand among others—that escalated product landed costs materially affecting gross margins during the year. Efforts to mitigate tariff impact included accelerating diversification of drinkware manufacturing capacity beyond China toward other countries which induced short-term supply chain disruptions impacting inventory availability that continued into Q4 of FY2025 [S2][S17].

The tariffs-related cost escalation coincided with an intricate global logistics environment challenged by port congestion and elevated transportation costs requiring some use of costlier air freight solutions temporarily reducing margin profile further [S18]. Despite these headwinds, YETI maintained rigorous quality control standards given its reliance on third-party manufacturing across multiple geographies including Mexico and Poland plus Asian countries. This diversified supplier base supports flexibility though also introduces complexity balancing cost-efficiency with reliability [S8][S14].

Ongoing monitoring of trade policy changes—such as judicial rulings affecting tariff statutes—and swift adaptation remain critical since any reversal or further imposition could either relieve or exacerbate margin pressures unpredictably [S17].

Returns and Capital Allocation

YETI exhibits a relatively strong return on equity at approximately 25% based on FY2025 net income relative to shareholders' equity [$165M / ~$650M] indicating efficient capital utilization despite earnings setbacks [F1].

The company generated solid operating cash flows ($255 million) that sufficiently cover capital expenditures ($43 million) supporting endurance of free cash flow generation ($212 million). This cash generation underpins shareholder-friendly capital allocation activities including aggressive share repurchase programs which totaled nearly $298 million in FY2025—up significantly from prior years—and no dividends currently paid reflecting preference for buybacks over distributions within current credit covenant constraints [F1][S24].

Long-term debt sits at $74 million under a secured credit facility with covenants restricting leverage levels as well as dividend payments limiting distribution flexibility but preserving liquidity balance [F1][S10][S22]. This prudent leverage profile supports financial stability amid an inflationary macro backdrop characterized by interest rate sensitivity.

Key Risks Summary

Several risks warrant consideration for tactical evaluation:

- Tariff volatility: The uncertain duration of current tariffs following recent court decisions introduces potential refund claims timing complexities alongside possible new tariff implementations.

- Supply chain disruptions: Manufacturing capacity losses or logistical bottlenecks affect timely order fulfillment risking revenue loss or partner dissatisfaction.

- Competitive intensity: Larger rivals may wield scale advantages while private label competition or discounting trends threaten margin sustainability.

- Brand reputation vulnerabilities: Social media-driven negative publicity—including about product recalls or ambassador conduct—can damage long-standing brand equity.

- Retail partner dynamics: The wholesale channel's dependence on retail partners’ commitment toward stocking/promotion introduces channel risk especially amidst changing consumer foot traffic patterns.

- Regulatory compliance: Expanding international presence requires navigating complex foreign regulations including privacy laws (GDPR etc.) adding cost burdens.

- AI implementation risks: Increasing integration of AI tools poses operational risks including bias or misapplications potentially disrupting analytics or customer interaction.

What To Watch Going Forward (Analysis)

Absent explicit forward guidance disclosure in available filings or news transcripts, monitoring key performance indicators such as quarterly gross margins reflecting tariff impact trajectory; new product launch acceptance especially beyond core cooler/drinkware lines; inventory levels versus sell-through rates indicating supply chain recovery; DTC customer acquisition cost efficiency; wholesale partner order sizes; overall marketing ROI; international revenue growth pacing; credit covenant compliance signals; leadership transitions' impact notably CFO dynamics announced February 2026; regulatory developments on tariffs; lingering recall-related reputational effects; plus competitor moves employing AI or digital experience enhancements will shape YETI’s ability to sustain momentum.

Conclusion

YETI Holdings remains a formidable player within the premium outdoor lifestyle sector built upon authentic brand heritage backed by innovative durable products carefully designed for rugged use cases. While persistent headwinds related to tariffs and supply chain disruption have moderated profitability during fiscal year 2025 compared with recent peaks, the company demonstrates consistent free cash flow generation enabling substantial share repurchases enhancing shareholder value metrics such as ROE.

Navigating evolving trade landscapes skilfully while expanding internationally via multi-channel distribution remains pivotal alongside safeguarding brand reputation through targeted marketing investments supported by integrated R&D capabilities fueling product pipeline development. Fostering strong retail partnerships balanced against an increasing direct-to-consumer focus appears central to sustaining differentiated positioning amid fragmented yet intensifying competition across dynamic global outdoor goods markets.

Disclaimer: This analysis is intended solely for informational purposes reflecting data as of February 27, 2026. It does not constitute investment advice or recommendations regarding YETI Holdings securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments