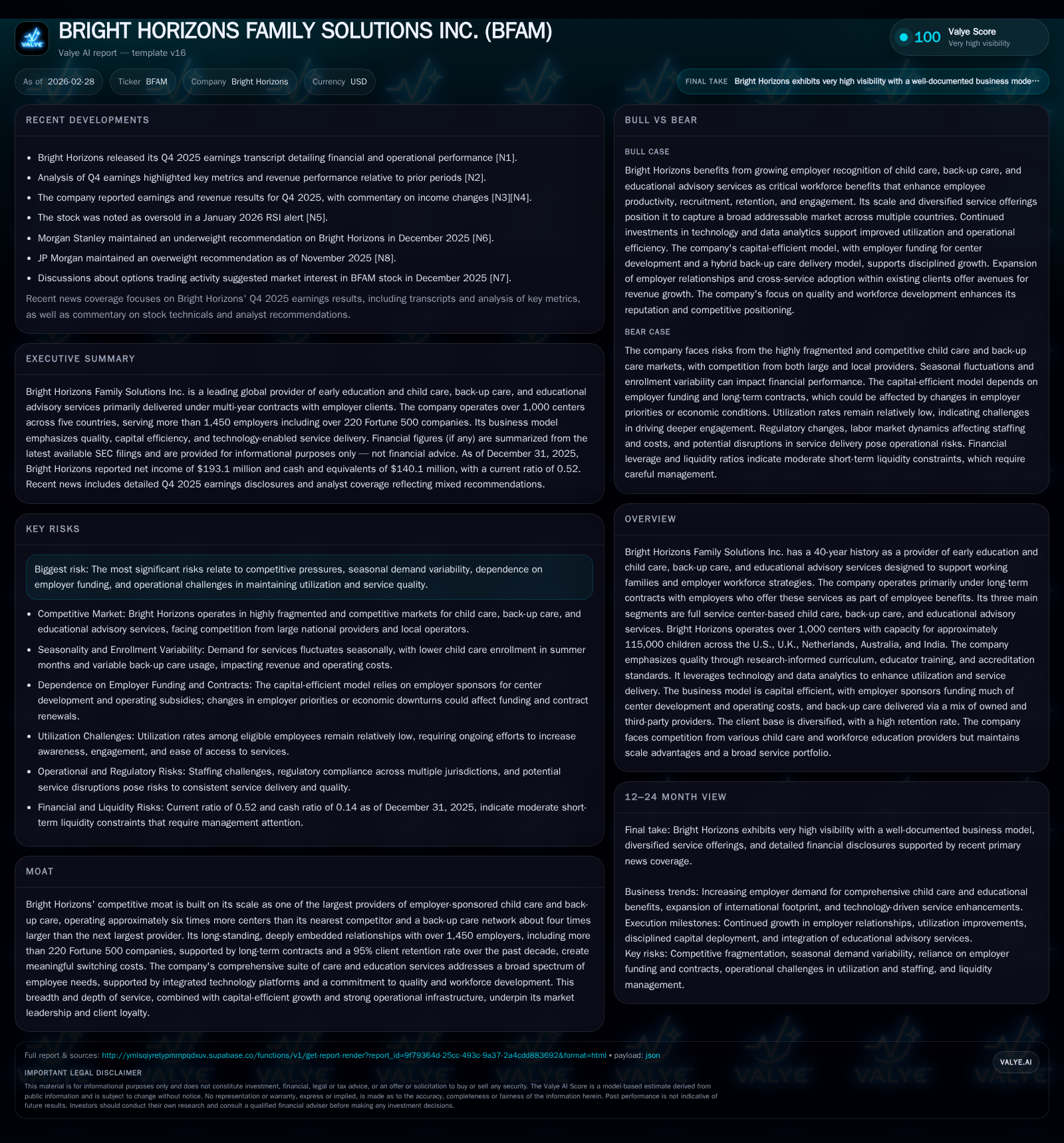

Bright Horizons Scales Employer-Sponsored Child Care with Strong Contract Retention but Faces Seasonal Demand Constraints

Bright Horizons leverages a dominant market position in employer-sponsored child care and back-up care, driven by extensive long-term contracts and quality focus.

Bright Horizons Family Solutions Inc. has solidified its market leadership by operating over 1,000 centers globally and maintaining enduring relationships with more than 1,450 employers, including over 220 Fortune 500 clients. The company’s revenue reached $2.93 billion in 2025, growing at approximately 8.7% year over year, supported by strong operating leverage and contract renewals. Seasonality and dependence on employer funding impose growth limitations, while capital allocation reflects robust free cash flow generation and significant share repurchases. Monitoring enrollment trends, utilization rates, and contract renewals will be critical to assessing future growth trajectories.

Company Overview

Bright Horizons Family Solutions Inc. has established itself over four decades as a global leader in early education and child care services tailored primarily toward employer-sponsored models. With operations spanning the U.S., U.K., Netherlands, Australia, and India, Bright Horizons runs approximately 1,010 centers with capacity for around 115,000 children as of late 2025 [S1][S15]. Its business model is chiefly built on multi-year contracts with employers who offer those services as employee benefits packages.

The company’s service portfolio is segmented into full service center-based child care—accounting for roughly 71% of revenues—back-up care solutions at about 25%, and educational advisory services comprising the remainder [S1]. This diversification enables the firm to address various needs of working families while providing employers with workforce support that enhances recruitment and retention.

Historical Growth and Performance

Bright Horizons has demonstrated consistent top-line growth since at least 2015. Revenue progression was notable:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 193 | 351 | 315 | 92 | +37.8% |

| 2024 | 140 | 337 | 247 | 97 | +88.9% |

| 2023 | 74 | 256 | 171 | 91 | -8.0% |

| 2022 | 81 | 188 | 158 | 71 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 225 | 259 | 14.4 |

| 2024 | 85 | 240 | 11.0 |

| 2023 | 0 | 165 | 6.1 |

| 2022 | 183 | 118 | 7.5 |

Source: SEC companyfacts cache [F1].

Despite some data gaps earlier on due to limited SEC XBRL tagging, from available evidence it is clear that revenue scaled substantially into the multi-billion-dollar range by the mid-2020s.

By fiscal year ended December 31, 2025, revenue was approximately $2.93 billion representing an estimated growth rate of ~8.7% compared to the prior year [F1]. Operating income exhibited stronger growth momentum with a rise of approximately 27.6% reaching nearly $315 million in FY2025 [F1]. Net income followed suit climbing close to $193 million or nearly a 38% increase Y/Y [F1].

Operational cash flow improved steadily as well — increasing from about $188 million in FY2022 to nearly $351 million in FY2025 — outpacing capital expenditures which hovered around $92 million in the latest year [F1]. This enabled free cash flow generation estimated near $259 million that underpins robust internal funding capacity.

Despite the capital light nature compared to asset-heavy industries, Bright Horizons invests steadily in new centers and technology enhancements supporting utilization optimization across its offerings [S1][S28].

Business Model Drivers

The company's moat resides primarily in scale advantages; it operates roughly six times more center-based facilities than its closest market rival and maintains a network for back-up care four times larger than competing providers [S1]. Long-term contractual arrangements with employer-clients — over 1,450 collectively including more than 220 Fortune 500 firms — yield a ~95% client retention rate over a decade-long span fostering stability and high switching costs [S1].

Quality leadership is reinforced through research-informed curricula, stringent educator training programs plus accreditation standards that are difficult for competitors to replicate quickly [S1]. Technology plays a pivotal role allowing data analytics-driven improvements in customer experience and service utilization [S1]. These factors combine with employer funding models to ensure sustainable economic returns.

The child care segment constitutes the lion’s share of revenues with steady demand stemming from workforce benefits budgeting while back-up care usage fluctuates seasonally, often rising during holidays and school breaks impacting cost dynamics [S15]. Educational advisory services remain smaller but strategic as corporate clients increasingly seek holistic family support solutions.

Geographic Segmentation

North America drives approximately 71% of total revenues ($2.09 billion), balanced against international operations representing almost one-third ($843 million) comprising significant presence particularly within the UK, Netherlands, Australia, and evolving Indian markets [S15]. Operating fixed assets are split evenly between North America (51%) and outside North America (49%), demonstrating broad geographical investment balance [S15].

Recent Developments & Financial Structure

Bright Horizons amended its credit facilities multiple times in recent years to improve liquidity flexibility and reduce borrowing costs [S4][S5][S7][S8][S12]. As of mid-2025:

- Term loan B stands at about $500 million maturing in late-2028 but partially prepaid using revolving credit availability.

- Revolving credit facility was increased from $400 million to $900 million with maturity extended to April 2030 enabling enhanced working capital support.

- Interest rates on debt have benefitted from credit rating upgrades with effective interest rates between ~5.7%-6.1% on term loans/revolving debt post amendments [S4][S5][S12][S17].

- Interest rate cap agreements covering up to $900 million protect against rises in SOFR above preset thresholds mitigating cash flow volatility risks related to variable rate debt exposures [S26][S27].

Cash balances totaled approximately $140 million at year-end alongside current assets exceeding current liabilities; however, short-term liabilities dwarf immediate liquidity measures resulting in a current ratio below unity (0.52) requiring close monitoring despite revolving credit facility availability [F1][S1].

Capital Allocation & Returns

Equity measured at roughly $1.34 billion supports an approximate ROE of ~14.4%, demonstrating efficient use of shareholder capital given steady earnings improvement [F1]. The firm actively repurchases shares reflected by buyback expenditures rising notably from about $85 million in FY2024 to over $225 million in FY2025 reinforcing confidence in free cash flow conversion and commitment to shareholder returns [F1].

The dividend payout profile is modest relative to earnings but sustained; explicit payout levels or targets were not detailed though dividend distributions complement buybacks as part of balanced capital return strategies [S1]. Free cash flow generation near $259 million after capex forms the core financial strength underpinning these allocations without excessive reliance on external financing.

Future Prospects & Risks

Growth prospects hinge on several interlocking factors:

- Continued expansion domestically through new center development tied closely with employer demand curves amid tight labor markets for qualified educators.

- International scaling particularly within UK markets already advanced along with strategic entry into emerging economies like India present new avenues.

- Technological innovation aimed at boosting utilization rates across services via online enrollment platforms or AI-enabled scheduling tools could unlock operational leverage.

- Enhanced integration of educational advisory services diversifies offerings albeit currently a smaller revenue component.

- Seasonal fluctuations remain challenging given summer enrollment dips offset partially by increased back-up utilization during school closures elevating operational cost profiles unpredictably.

- Competitive intensity may intensify as alternative child care solutions or gig-economy influenced backup formats evolve.

- Heavy dependence on employer funding means macroeconomic shifts affecting corporate benefits budgets could restrain demand or contract negotiations.

No explicit forward guidance on revenue or earnings targets was furnished publicly beyond standard commentary accompanying Q4/2025 results; thus precise forecast tracking should focus on contract renewal volumes, center occupancy rates, margin trends excluding seasonal distortions alongside ongoing debt management execution .

Conclusion

Bright Horizons sustains a commanding position within employer-sponsored early education through scale dominance validated by multi-decade client ties, quality reputation, and leveraging technology-driven operational enhancements [S1]. Financially robust with accelerating profitability margins and dependable free cash flow generation enables substantial shareholder returns highlighted by growing buybacks alongside prudent debt refinancing initiatives ensuring manageable leverage metrics.

However, growth pacing will be tempered by inherent sector seasonality effects compounded by dependency on employer benefit spend trajectories plus emerging competition risks surrounding innovative child care alternatives requiring vigilant strategic adaptability going forward.

This report compiles verified historical financial data from Bright Horizons Family Solutions’ SEC filings augmented by recent earnings call insights without offering investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments