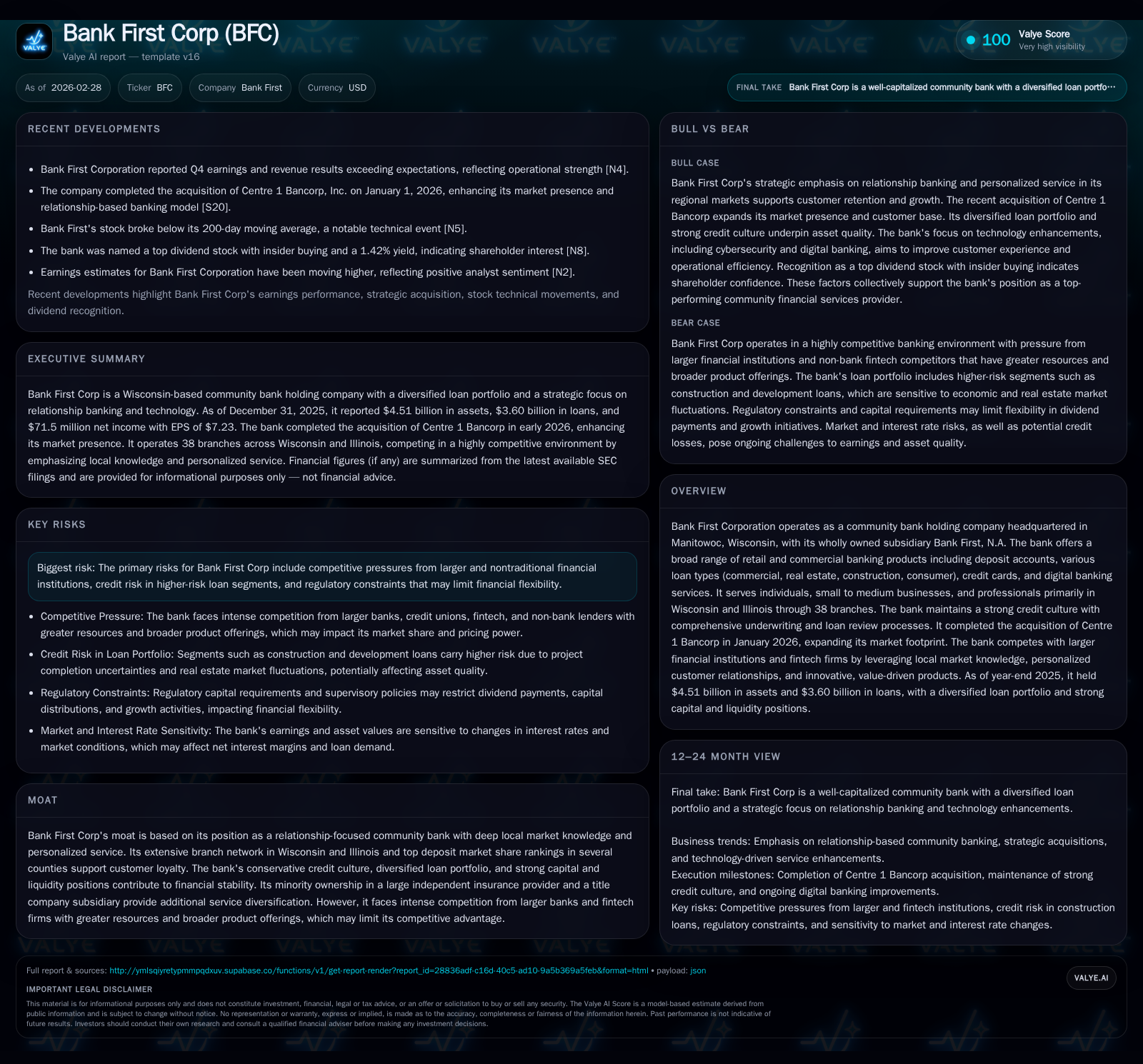

Bank First Corp Strengthens Local Banking Franchise While Balancing Growth and Risk

Bank First Corporation leverages community banking strengths and strategic acquisition to underpin growth amidst competitive and regulatory challenges.

Bank First Corp, a regional community bank headquartered in Manitowoc, Wisconsin, has demonstrated significant earnings growth over recent years, driven by expanding commercial lending and strong deposit retention. The acquisition of Centre 1 Bancorp in early 2026 enhances its footprint in Wisconsin and Illinois, complementing its relationship-based lending model. Despite steady profitability and disciplined capital management with robust shareholder returns, BFC faces competitive pressure from larger banks and fintech firms alongside regulatory constraints. Its conservative credit culture and ongoing investment in digital banking infrastructure aim to sustain resilience and growth in an evolving industry landscape.

Historical Growth Trajectory and Earnings Drivers

Bank First Corp has manifested notable net income growth since FY2022, when net income totaled approximately $12.8 million. The company’s strategic emphasis on deepening client relationships alongside expanding commercial loan originations fueled earnings to peak at $74.5 million in FY2023 before settling at around $71.5 million in FY2025 [F1]. This performance underscores the efficacy of its locally focused lending approach serving small to medium-sized businesses and consumers across Wisconsin and Illinois.

The earnings trajectory indicates the bank’s capability to capitalize on niche market opportunities through personalized banking services that larger institutions may overlook, evidencing a potent competitive moat rooted in community trust and deposit market share leadership within multiple counties [S4][S5].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 71 | 62 | 11 | +9.0% |

| 2024 | 66 | 66 | 7 | -12.0% |

| 2023 | 75 | 53 | 13 | +480.1% |

| 2022 | 13 | 40 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 22 | 51 | 11.1 |

| 2024 | 32 | 59 | 10.2 |

| 2023 | 10 | 39 | 12.0 |

| 2022 | 14 | 33 | 2.8 |

Source: SEC companyfacts cache [F1].

Net income soared markedly post-2022 owing to focused commercial lending expansion before normalizing amidst competitive headwinds.

2025 Performance Metrics: Profitability, Cash Flow, and Operational Efficiency

In FY2025, Bank First posted an approximate return on equity of 11.1%, signaling strong profitability relative to its shareholders' equity base of roughly $644 million [F1]. Operating cash flows declined modestly by about 5% year-over-year to nearly $62.5 million while capital expenditure outlays surged over 58% to approximately $11.4 million, indicative of intensified investments likely targeting digital transformation initiatives or branch modernization efforts [F1][S1].

Free cash flow generation remained robust at over $51 million after accounting for capex commitments.

This financial profile reflects operational efficiency balanced against proactive reinvestment strategies geared towards supporting service innovation and cybersecurity strengthening amid heightened risk environments.

| Fiscal Year | Operating CF (USD mln) | Operating CF YoY % | Capex (USD mln) | Capex YoY % | Equity (USD mln) | Share Buybacks (USD mln) | Approx ROE (%) |

|---|---|---|---|---|---|---|---|

| 2022 | 40.0 | 6.9 | 453 | 14.3 | |||

| 2023 | 52.9 | 32 | 13.5 | 96 | 620 | 10.0 | |

| 2024 | 65.8 | 24 | 7.2 | -46 | 640 | 31.9 | |

| 2025 | 62.5 | -5 | 11.4 | 58 | 644 | 22.0 | ~11.1 |

The increased capital expenditure highlights Bank First's commitment to technological enhancement amid steady cash flow performance.

Market Positioning: Community Roots Versus Competitive Pressures

Bank First's fortress lies in its entrenched local presence via thirty-eight branches spanning nineteen counties across Wisconsin and Illinois [S28][S5]. Its deposit market share ranks top three in seven counties per mid-2025 FDIC data, underscoring customer loyalty built through personalized financial solutions appealing especially to small- to mid-sized enterprises (SMEs) and individual professionals [S4][S5].

However, the bank confronts intensifying competition not only from regional/national banks with superior scale economies but also agile fintech companies that leverage embedded finance models integrating payments, lending, or financial management directly within non-banking platforms — a disruptive force amplifying pricing pressure on deposits and loans [S4].

Despite this environment, Bank First differentiates itself with localized decision-making agility, close customer engagement practices, as well as diversified offerings including minority ownership stakes in independent insurance (Ansay & Associates) and title services firms providing incremental value beyond traditional banking [S1].

Credit Culture and Loan Portfolio Integrity

Bank First adopts a stringent credit administration framework characterized by detailed multi-tiered approval protocols incorporating line officers up to board-level endorsements for large exposures [S12][S7]. Loan review processes are robustly outsourced to specialized firms that conduct thorough risk rating validation on roughly forty percent of the commercial portfolio annually.

Its loan portfolio stands diversified across commercial real estate ($1.78 billion; 49%), residential mortgages ($895 million; ~25%), construction loans ($215 million; ~6%), commercial & industrial loans ($647 million; 18%), plus consumer loans ($55 million; ~1%) as of year-end FY2025 [F1][S7][S20]. Nonperforming assets remain minimal at approximately $5.8 million or a scanty nonaccrual ratio of just about 0.2%, evidencing prudent underwriting rigor balanced against some exposure to cyclical real estate sector risks [S7].

Risk mitigation also includes conservative loan-to-value ceilings typically capped below or equal to eighty-five percent for commercial properties reinforced by personal guaranties on construction projects mitigating default probability [S14][S24]. This conservative stance is foundational to maintaining asset quality despite competitive pressures encouraging looser credit standards elsewhere.

Strategic Acquisition of Centre 1 Bancorp and Geographic Expansion

On January 1, 2026, Bank First consummated the acquisition of Centre 1 Bancorp, marking a strategic milestone augmenting its geographical footprint within target Midwest markets [N2][S5]. This transaction immediately broadened its branch network beyond existing locations enhancing customer reach while reinforcing market share.

Management highlighted this acquisition as compatible with their relationship-focused strategy emphasizing organic growth supplemented selectively by acquisitions that deepen local market penetration [S5]. However integration risk concerns exist — ranging from system harmonization challenges to potential cultural misalignments — necessitating vigilant execution oversight.

The deal strategically positions Bank First for incremental earnings uplift given expected cross-selling synergies alongside operational scale benefits derived through amalgamation of overlapping functions and expanded deposit franchises.

Capital Management: Shareholder Returns Through Buybacks and Dividends

Bank First maintains disciplined capital stewardship evidenced by steady dividend distributions (implied though not numerically disclosed) complemented by active stock repurchases amounting to $22 million during FY2025 down from higher repurchase levels in previous years (e.g., ~$32 million in FY2024) [F1][S1].

Shareholder equity approximated $644 million at end-2025 representing stable capital buffers underpinning an efficient return on equity of around eleven percent [F1]. This allocation framework balances reinvestment into business capabilities with returning excess capital effectively amidst regulatory constraints requiring well-capitalized status adherence for distribution flexibility [S16][S10].

Buybacks serve to offset dilution impacts while signaling confidence from management regarding company valuation within a moderate growth outlook context.

Liquidity, Capital Structure, and Regulatory Compliance

Liquidity remains robust with cash equivalents totaling approximately $243 million as reported at year-end FY2025 offering ample buffer for operational needs including loan demand fluctuations or deposit withdrawals [F1][S6]. Regulatory capital ratios comfortably exceed "well-capitalized" thresholds with Tier 1 leverage ratio above mandated minima aligning with Basel III-like requirements enforced by OCC supervision [S8][S10].

Restrictions governing insider transactions, lending limits set conservatively below statutory caps at roughly eighty percent internal cap ensure concentrated exposure mitigation particularly for single borrower limits approximating $55 million internal threshold relative to capital base [S14][S12].

Compliance extends through rigorous cyber governance frameworks overseen directly by the Board’s Audit Committee via an experienced Information Security Officer (ISO) who coordinates continuous risk assessments including penetration testing alongside third-party consultants ensuring alignment with risk appetite statements [S1]. This integrated IT risk architecture supports both resilience objectives and regulatory expectations including SEC disclosure obligations regarding cybersecurity preparedness.

Technology, Cybersecurity Governance, and Digital Banking Initiatives

Capital expenditure increases predominantly target information technology infrastructure upgrades reflecting an overarching corporate priority on digital transformation intended to optimize client access channels such as mobile banking apps alongside backend efficiency enhancements [F1][S4]. These initiatives enable front-line employees through automated processes facilitating swift customer service delivery consistent with strategic priorities outlined under CAMELS IT focus areas [S28].

Cybersecurity governance is formalized with the ISO reporting independently to both senior management/legal counsel as well as the Audit Committee achieving direct Board engagement fostering transparent risk communication cycles crucial amid escalating cyber threat vectors targeting financial institutions nationally [S1]. Employee training programs augment these controls preserving institutional knowledge while preparing staff for emerging technology-related risks.

Successfully balancing technology adoption with traditional personal touchpoint banking preserves Bank First’s competitive edge against purely digital entrants lacking community integration advantages.

Outlook: Growth Prospects and External Constraints to Monitor (Analysis)

Looking forward, Bank First's strategy appears anchored in reinforcing its core strength as a trusted community lender delivering differentiated value via personalized solutions leveraging local insights supplemented by acquisitive growth exemplified by Centre 1 Bancorp’s purchase [N1][N2][S22].

Potential catalysts include deepening penetration into existing markets through enhanced product innovation especially digital offerings enabling cross-sell fatigue reduction among established customers.

Conversely, external constraints loom — growing fintech competition utilizing embedded finance mechanisms could erode margin pools while tighter regulatory oversight might impose cost escalations related to compliance burden expansions particularly if asset thresholds surpass CFPB routine supervision triggers [N1][N2][S22]. Escalating credit concentration risks arising from commercial real estate segments demand vigilant monitoring given historically cyclical sensitivity profiles [S18][S20].

Success will depend on maintaining underwriting discipline coupled with dynamic customer engagement blended seamlessly with prudent capital deployment maintaining strong liquidity buffers sustained through rigorous risk management frameworks inclusive of cybersecurity resilience measures laying groundwork for sustained operational stability amidst industry digitization dynamics.

This analysis is for informational purposes only based on publicly available filings dated through February 27, 2026, supplemented by select news coverage without reflecting any investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments