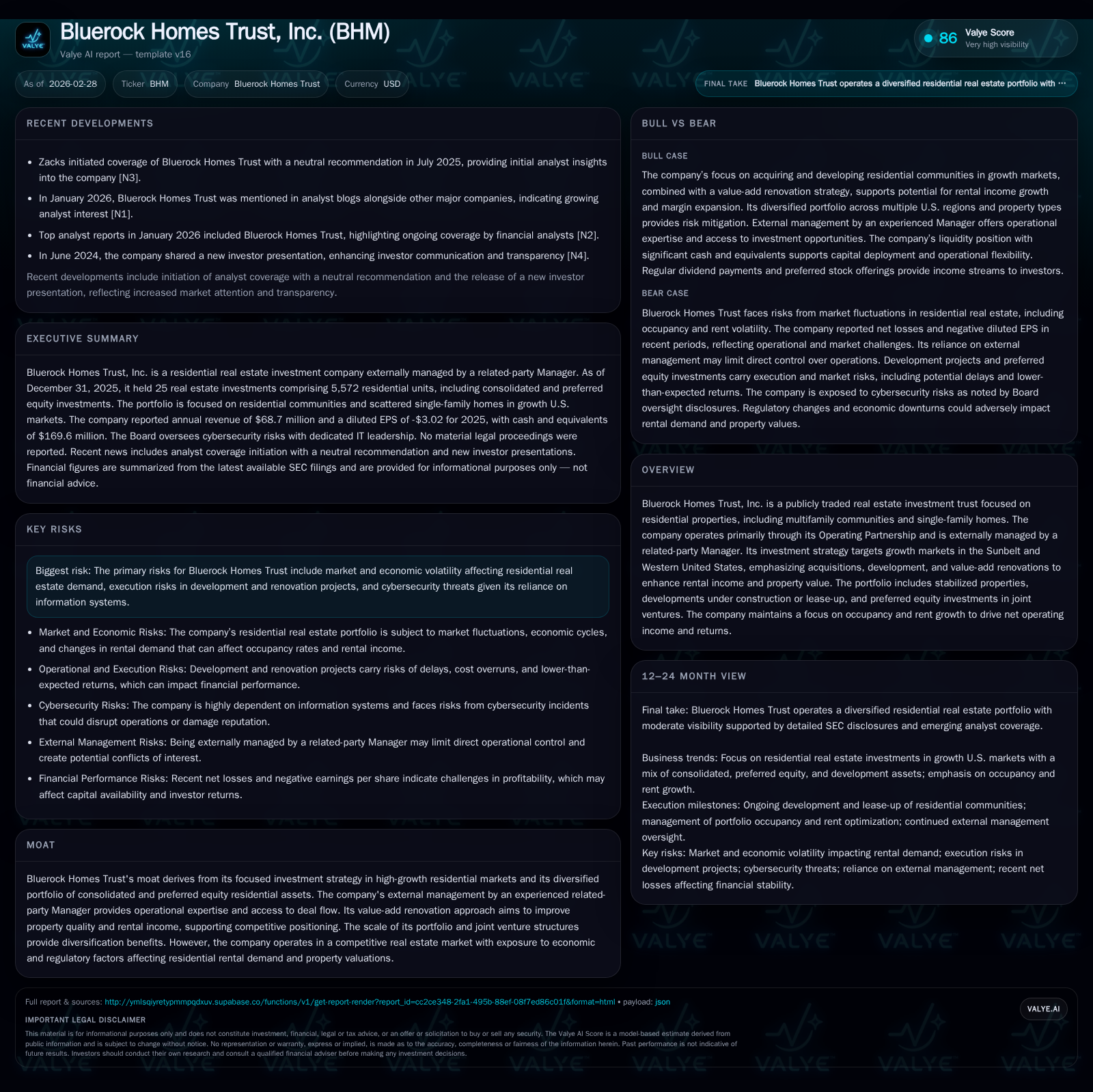

Bluerock Homes Trust’s Accelerated Portfolio Expansion Balances Cash Flow Growth and Leverage

Strong revenue and cash flow growth driven by strategic acquisitions and renovations contrasts with elevated leverage and modest net income.

Bluerock Homes Trust, Inc. has aggressively expanded its residential real estate portfolio over the past few years, focusing on high-growth Sunbelt and Western markets through acquisitions, developments, and value-add renovations. This strategy contributed to a nearly 37% revenue increase in 2025 and a more than doubling of operating cash flow. However, these gains come with rising leverage, as mortgages payable increased by over $175 million in one year, pressuring net income and equity levels. The company’s capital allocation emphasizes reinvestment in growth initiatives supported by revolving credit facilities and preferred stock issuances. Monitoring execution risks on development projects and managing rising debt costs will be critical for sustaining future growth and cash flow generation.

Company Overview

Bluerock Homes Trust, Inc. (BHM) is a residential real estate investment trust that acquires, develops, renovates, and manages multifamily communities and scattered single-family homes primarily targeting the Sunbelt and Western United States—a region known for robust population growth and expanding rental demand. Operating through its Operating Partnership and managed externally by an affiliated Manager, Bluerock pursues a growth strategy centered on acquiring stabilized assets, executing value-add renovations to enhance rent profiles, alongside developments in lease-up phases and preferred equity stakes in joint ventures [N1][S1].

Historical Performance Trends

Over the last four years through fiscal year-end 2025, Bluerock Homes Trust demonstrated consistent top-line expansion: revenue climbed from $34.1 million in FY2022 to $68.7 million in FY2025—a compound uptick fueled by acquisitions and active portfolio enhancement efforts yielding both occupancy gains and rent escalations [F1]. Correspondingly, operating cash flow showed an outsized rise, surging from $3.5 million in 2022 to nearly $28 million in the latest fiscal year—a reflection of operational stabilizations across growing unit counts offsetting initial costs associated with development leasing periods [F1]. Capital expenditures also rose sharply from $9.3–18.6 million range historically to $17.4 million recently illustrating aggressive reinvestment into property upgrades supporting rental income growth [F1].

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|

| 2025 | 69 | 28 | 17 | +36.9% |

| 2024 | 50 | 9 | 9 | +22.2% |

| 2023 | 41 | 14 | 10 | +20.4% |

| 2022 | 34 | 3 | 19 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 3 | 10 |

| 2024 | 2 | 0 |

| 2023 | 13 | 4 |

| 2022 | -15 |

Source: SEC companyfacts cache [F1].

*Note: Equity reflects common stockholders' equity per annual filings; dividends shown are paid amounts.

Despite top-line momentum, Bluerock reported a negative net income approximately -$1 million in its last stated period implying profit challenges tied largely to financing costs, depreciation from capital-intensive investments, or transient operational inefficiencies given rapid scaling [F1][S10]. The implied return on equity hovers near -0.8% underscoring the early-phase investment cycle cost absorption impacting bottom-line profitability.

Capital Structure and Leverage

The company's balance sheet displays notable leverage dynamics linked to funding its acquisition and development pipeline scaled rapidly post-2023:

- Mortgages payable surged approximately $175 million year-on-year from about $253 million at end-2024 to over $428 million by end-2025 [F1][S13][S22].

- Revolving credit borrowing decreased substantially from prior year but remains an available flexibility tool with KeyBank providing up to $50 million revolving loans focused on DST Program financing; at reporting date this facility was fully paid down but immediately accessible [S4][S16][S24].

- The Deutsche Bank loan refinanced the prior Amended Deutsche Bank Credit Facility with interest rates indexed to term SOFR plus ~2.80–2.95%, exposing BHM to floating rate interest costs mitigated partly by rate caps covering medium-term periods through April or October of corresponding years [S4][S16].

- Preferred stock outstanding increased materially with Series A Redeemable Preferred Stock shares issued growing from roughly 4.6 million shares at end-2024 to over 6.2 million shares at end-2025 raising liquidation preference upwards of $142 million versus prior ~$102 million—an important capital buffer but with fixed dividend obligations totaling over $9 million annually recently reflecting steady payout commitments [S11][S19][F1].

This elevated leverage strategy supports rapid portfolio scaling but increases exposure to interest rate fluctuations amidst the current macroeconomic environment characterized by tightening monetary policies.

Growth Drivers and Portfolio Characteristics

Bluerock's emphasis on high-growth regions benefits from favorable demographic trends predominantly marked by domestic migration patterns favoring Sunbelt states such as North Carolina (Charlotte), Texas (Houston suburbs), Georgia (Savannah), Florida (Port St Lucie), Arizona (Chandler), among others where the company holds key investments like Allure at Southpark community [N1][S1]. Value-add renovations upgrading unit interiors combined with new construction/development projects generate opportunities for rental growth exceeding market averages thus driving Net Operating Income (NOI) upwards.

Additionally, the company's blended portfolio spans:

- Stabilized properties generating recurring rental incomes,

- Properties under lease-up or active redevelopment phases,

- Preferred equity stakes offering mezzanine-like returns within joint venture structures enhancing diversification.

Execution risk resides primarily in:

- Lease-up velocities meeting forecast timelines,

- Cost management during renovation/development amidst inflationary pressures,

- Sustaining occupancy rates above market baselines amid evolving economic headwinds.

Cash Flow Profile & Capital Allocation

Operationally derived cash flows improved substantially in FY2025 aligning with management’s reinvestment thesis:

- Operating cash flow reached almost $28 million while capital expenditures totaled about $17 million resulting in positive free cash flow approximating $10 million supporting liquidity reserves [F1].

- The company pays dividends on preferred shares totaling approximately $9 million reflecting stable fixed-income commitments.

- Common dividend payments also rose though remaining modest relative to overall cash flows—around $3.36 million reflecting cautious capital distribution amid expansion [F1][S19][S20].

- No share repurchases occurred under authorized plans during the period indicating prioritization of balance sheet reinforcement over buybacks [S20][S26].

Management utilizes proceeds from preferred offerings along with borrowings against revolving credit lines plus mortgage financings for ongoing investments indicating a balanced approach favoring growth over immediate distributable yield maximization.

Risks & Governance Oversight

Material risks identified include:

- Cyclicality affecting residential rental demand influenced by macroeconomic volatility and regional economic shifts,

- Execution risk inherent in development/renovation projects potentially impacting projected returns,

- Cybersecurity vulnerabilities owing to dependency on complex IT systems; a dedicated leadership team with combined decades of industry experience actively monitors these threats incorporating regular Board-level oversight mechanisms ensuring compliance and mitigation strategies remain robust [S1].

Future Outlook & What To Watch

Though explicit earnings guidance for upcoming periods was not disclosed within the provided filings or news releases [N#]/[S#], key monitoring points include:

- Trajectory of occupancy rates post-renovation completions demonstrating rent roll stabilization,

- Development pipeline progress matching or exceeding scheduled milestones without cost overruns,

- Interest rate environment impact on borrowing costs given significant floating-rate exposure,

- Dividend policy adjustments which might signal shifts between reinvestment intensity versus returns distribution,

- Capital raising activities alongside any asset dispositions that will influence leverage ratios,

- Joint venture investment performance contributing indirectly to earnings via equity method accounting.

Conclusion

Bluerock Homes Trust evidences a deliberate strategy capitalizing on strong demographic trends through targeted multi-family residential real estate investments enhanced by active portfolio management involving renovations and new developments primarily located in favored U.S regions experiencing substantial population inflows. The palpable spike in revenue alongside operating cash flow highlights operational scaling achievements; concurrently mounting mortgage debt levels coupled with ongoing capital expenditure needs exert pressure on net income stability underscoring profitability challenges commonly observed during accelerated expansion phases. The company’s focus on liquidity through credit facilities augmented by preferred stock issuances provides financial flexibility crucial for sustaining growth yet heightens sensitivity toward interest rate fluctuations going forward. Investors should observe execution success factors relating to renovation lease-ups alongside prudent capital management balancing debt servicing with distribution policies as critical indicators shaping future value creation potential.

This analysis is based exclusively on public information available as of February 28, 2026, including SEC filings and news reports cited herein without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments