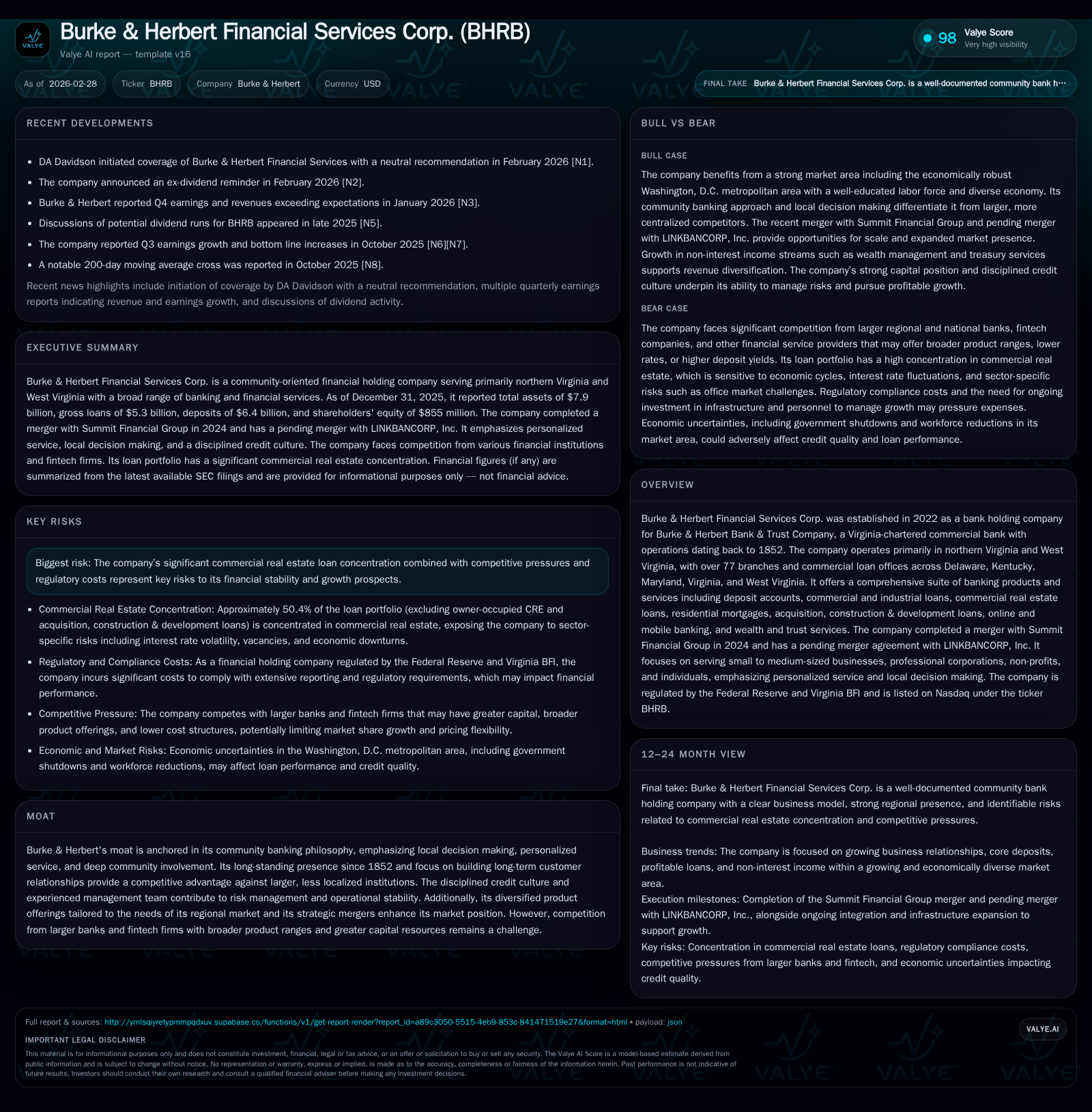

Burke & Herbert Financial Services' Profit Surge Highlights Merger-Driven Growth and Community Banking Strength

Burke & Herbert Financial Services Corp. demonstrates robust earnings growth and solid capital position through strategic mergers and a disciplined community banking approach.

Burke & Herbert Financial Services Corp. has shown impressive financial performance from FY2023 to FY2025, driven largely by strategic acquisitions including the 2024 Summit merger. The company’s assets, deposit base, and equity have grown considerably, supported by strong net income growth of over 228% year-over-year in 2025. Focused on serving small to medium businesses in its Mid-Atlantic regional markets, the company leverages its community banking philosophy and disciplined credit culture to maintain risk management in a highly competitive environment. Capital adequacy is well maintained with prudent liquidity management and active asset-liability oversight. Its pending merger with LINKBANCORP, Inc. suggests a continuation of growth through acquisition. Key risks remain concentrated commercial real estate exposure and competitive pressures from larger banks and fintech firms.

Company Background and Historical Performance

Burke & Herbert Financial Services Corp., established as a holding company in 2022 for Burke & Herbert Bank & Trust Company—operating since 1852—is a regional commercial bank primarily serving northern Virginia, West Virginia, and surrounding states including Delaware, Kentucky, and Maryland [S1][S2]. The company embraces a community banking philosophy that prioritizes localized underwriting decisions, relationship banking, and involvement in local economies.

Financially, Burke & Herbert has recorded rapid expansion since becoming publicly listed on Nasdaq under the ticker BHRB. The most striking feature over its brief corporate history is the profound surge in net income: from $22.7 million in FY2023 to $35.7 million FY2024 (+57% YoY), then leaping to $117.3 million FY2025—a remarkable +228% YoY gain driven by organic growth aligned with strategic acquisitions (notably the Summit merger in mid-2024) [F1][S16]. This amplified profitability underscores successful synergy realization from M&A activity combined with stable underlying demand for commercial banking solutions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 117 | 108 | 12 | +228.5% |

| 2024 | 36 | 86 | 5 | +57.4% |

| 2023 | 23 | 43 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 34 | 96 | 13.7 |

| 2024 | 29 | 81 | 4.9 |

| 2023 | 16 | 28 | 7.2 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures not explicitly disclosed; focus placed on net income and cash flow trends.

Business Model and Market Footprint

Burke & Herbert operates as a full-service community bank targeting small-to-medium enterprises (SMEs), owner-operators of businesses, professional corporations along with non-profits and personal banking clients within its defined regional footprint [S8]. Its lending portfolio focuses on:

- Commercial real estate loans: both owner-occupied properties and investor-held real estate.

- Acquisition/construction/development loans typical for commercial building projects.

- Commercial & industrial loans supplying working capital or equipment financing.

- Residential mortgage loans including traditional fixed-rate and adjustable-rate mortgages.

The bank’s multi-state branch network comprises over 77 branches plus commercial loan offices emphasizing deep local ties critical for the underwriting process [S2]. Deposit products range from basic checking/savings accounts to certificates of deposit complemented by online/mobile digital banking capabilities aligned with client preferences.

Commercial lending remains the pivot point of revenue generation but entails inherent credit risk concentration particularly around commercial real estate—a known vulnerability as stressed in regulatory disclosures (see Risks below) [S20].

Growth Prospects and Strategic Drivers

The pivotal milestone remains the successful integration of Summit Financial Group completed on May 3rd, 2024 which expanded Burke & Herbert’s market presence specifically into West Virginia [S2][S16]. This transaction broadened its asset base materially alongside diversification of loan portfolios.

Furthermore, Burke & Herbert filed a merger agreement on December 18th, 2025 with LINKBANCORP Inc., illustrating continued growth ambitions through M&A activity [S16]. This pending transaction—if consummated—would further deepen penetration across the Mid-Atlantic region while enhancing scale economics such as branch network optimization and cross-selling opportunities.

Organic growth initiatives are also ongoing: leveraging technology-enabled treasury management tools alongside wealth management offerings aims to capture more share within existing relationships while appealing to new customers valuing personalized service uncommon among larger peers [S25]. While competitive headwinds persist—especially from large national banks wielding broader products sets and fintech disruptors—Burke & Herbert's community-centric approach mitigates these threats through loyalty anchored on local expertise.

Financial Forecasts and Key Milestones

Explicit forward guidance is not disclosed publicly; however monitoring key performance indicators such as loan growth rates post-LINKBANCORP deal closure will be instructive. Additionally, the trajectory of credit metrics given current commercial real estate exposure warrants scrutiny alongside continuing efficiency improvements from integration synergies.

The retirement announcement effective mid-2026 of long-serving President H. Charles Maddy III represents a notable leadership transition event warranting attention for operational continuity implications [N3][S3].

Capital Allocation and Returns

Capital structure remains conservative with shareholders’ equity increasing substantially from $314 million at FY2023 year-end to $855 million at FY2025 close supporting ample capital ratios required under Basel III guidelines enforced by Federal Reserve supervision [F1][S7][S13].

ROE for FY2025 approximates a healthy ~13.7% based on reported net income relative to equity—indicative of efficient equity utilization given expansion phase metrics [F1]. The operational cash flow well exceeds capital expenditures leaving Burke & Herbert free cash flow near $96 million suggestive of financial flexibility to support dividends or reinvestment.While buyback programs have not been emphasized recently, growing dividend payouts—$33.9M declared FY2025 versus $28.6M prior year—underscore commitment to returning capital consistent with rising profitability.

Liquidity is managed via diversified deposits including core business deposits supplemented intermittently by brokered CDs alongside committed short-term borrowing lines from FHLB and Federal Reserve programs ensuring resilience amid fluctuating funding costs. At September 30th 2025 brokered deposits fell by ~$120M while non-brokered deposits grew modestly signaling measured liquidity rebalancing post-mergers[S12][S13].

Risk Factors

Key risks stem from high concentration in commercial real estate loans which include acquisition/construction/development projects subject to economic cycles impacting collateral values amplifying potential charge-offs during downturns. Moreover large borrower concentrations (~10 largest borrowers represent around ~10% total loan portfolio) pose idiosyncratic credit risk requiring vigilant monitoring[S16][S20].

Competitive challenges emanate from larger regional/national banks benefiting scale economics plus fintech entrants innovating faster across payment platforms or consumer facing services potentially eroding market share in tech-savvy demographics.

Regulatory compliance imposes substantial operational costs; moreover any failure to maintain well-capitalized status might limit capital distributions or restrict business initiatives. Cybersecurity threats also remain relevant operational hazards necessitating ongoing investment in defenses[S19],[S20].

Conclusion

Burke & Herbert Financial Services exhibits strong momentum fueled by acquisition-led expansion coupled with organic growth rooted firmly in community banking excellence—the hallmark since its inception in the mid-19th century. The company’s robust earnings acceleration from FY23 through FY25 affirms execution capability despite a competitive environment marked by industry consolidation.

Future prospects hinge on the successful consummation of the LINKBANCORP merger along with maintenance of credit discipline especially within concentrated CRE lending portfolios. Capital strength supports measured returns to shareholders while underpinning future investments.

Monitoring key developments around the leadership succession planned in mid-2026 will be necessary given its potential impact on strategy continuity.[N3]

This analysis is based exclusively on publicly available information as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments