BIO-key International Faces Nasdaq Delisting Amid Filing Delays and Operating Losses

Recent regulatory compliance issues and sustained operating losses highlight challenges in BIO-key’s biometric identity security business.

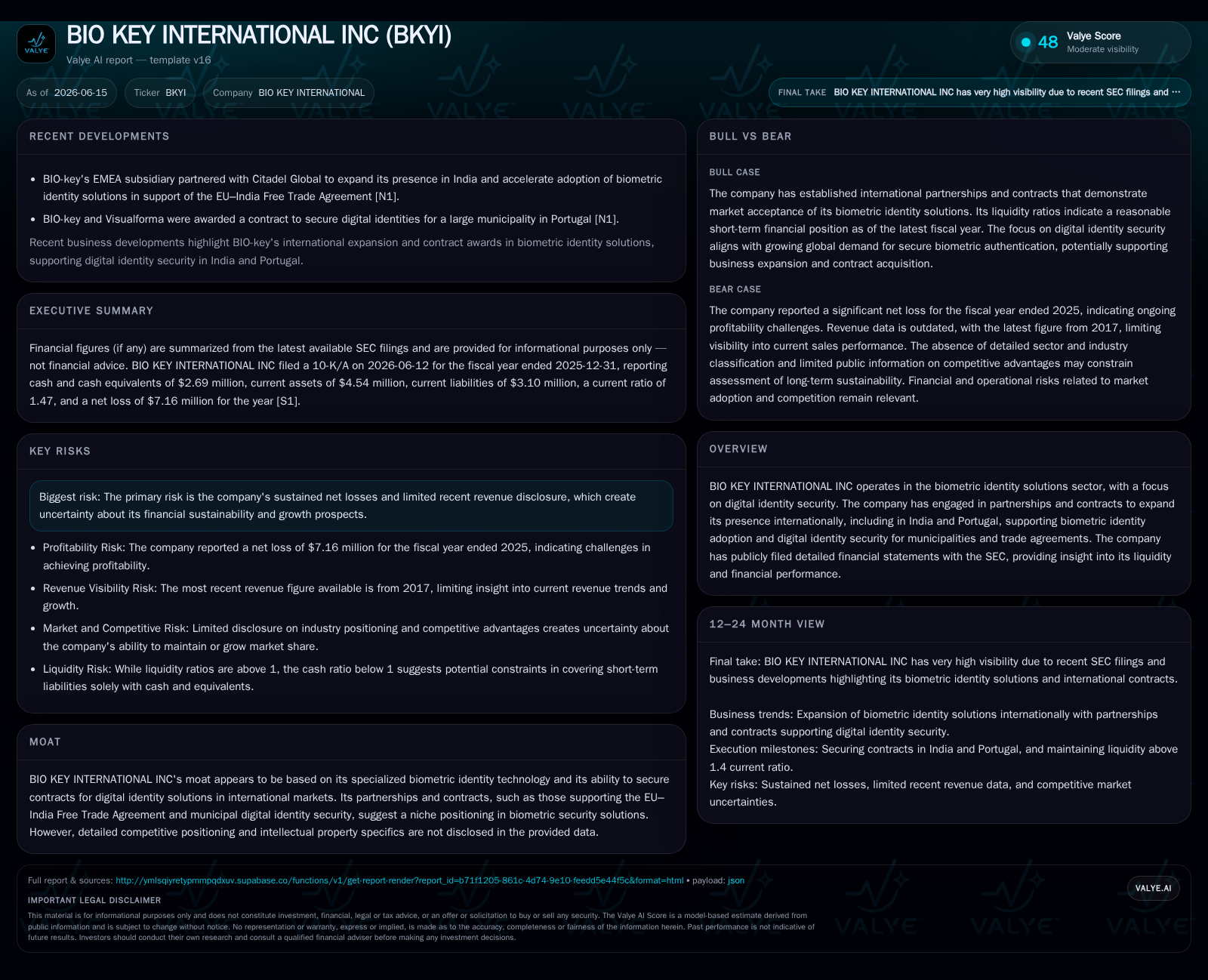

BIO-key International received a Nasdaq delisting notice due to its failure to timely file the required quarterly report for Q1 2026, escalating regulatory pressure and trading suspension risk. The company operates an integrated biometric identity and access management platform targeting enterprise and government clients with biometric MFA solutions designed to replace traditional token or phone-based methods. While it has international contracts supporting digital ID adoption, persistent net losses and high operating expenses underscore financial sustainability concerns. Key industry drivers such as rising MFA adoption and cybersecurity threats support the relevance of BIO-key’s offerings, but competitive gaps, delayed filings, and limited revenue growth pose significant near-term risks.

Recent Regulatory Compliance Challenges

On June 5, 2026, BIO-key International received formal notice from Nasdaq's Listing Qualifications Department citing its failure to file the required Quarterly Report on Form 10-Q for the period ended March 31, 2026 [S3][S17][S19][S20]. This regulatory breach provides grounds for delisting the company's common stock from the Nasdaq Capital Market and reflects ongoing difficulties adhering to timely reporting requirements. A Nasdaq Hearing Panel was scheduled for June 16, signaling imminent decisions regarding exchange listing status. This was preceded by a prior suspension of trading after failure to meet Nasdaq's minimum bid price rule despite a reverse stock split executed in April to address these listing standards

This compliance lapse not only threatens liquidity through reduced investor access but also undermines market confidence during already razor-thin margins and net losses.

Business Model and Product Portfolio

BIO-key operates within the biometric identity and access management (IAM) sector, specializing in multi-factor authentication (MFA) platforms leveraging identity-bound biometrics intended to create passwordless authentication experiences. Its key products are:

PortalGuard IDaaS: A cloud-enabled enterprise IAM platform providing secure authentication for employees, contractors, partners, and customers. It supports single sign-on (SSO), self-service password reset, and integrates within larger IAM ecosystems including Microsoft Azure AD and Okta.

WEB-key: A scalable biometric service management system designed for civil identification projects requiring enrollment, verification, authentication, and regulatory compliance delivered via multi-tenant private or public clouds.

MobileAuth: Biometric mobile phone authentication applications complementing the hardware fingerprint scanners BIO-key produces.

BIO-key’s architecture focuses on removing dependence on physical tokens or smartphone apps which remain susceptible to human error and loss; instead it binds authentication directly to biometric identifiers at endpoints [S1]. This addresses pain points especially relevant where shared workstations or kiosk environments thwart traditional MFA approaches

Revenue is generated primarily through licensing fees for software platforms—recently comprising about 58% of total revenues in 2025—hardware sales (~22%), likely fingerprint scanners and FIDO-compliant devices, alongside service contracts related to support and cloud access [S1]

Industry Context and Competitive Positioning

BIO-key competes in a growing but increasingly crowded ecosystem of biometric IAM providers including software-centric firms like Okta and Ping Identity, hardware specialists such as HID Global, government digital identity solution vendors, and cloud-based Identity-as-a-Service operators. The market is driven by expanding remote workforces demanding secure yet frictionless access methods plus escalating cyber threats targeting passwords as weak points.

BIO-key distinguishes itself with its emphasis on Identity-Bound Biometrics (IBB) that promise both higher security resilience against phishing/hacking attempts and a more intuitive user experience without secondary devices. However, the company faces formidable competition leveraging broader sales networks or deeper integrations within enterprise cloud environments.

Geographically, BIO-key has pursued international expansions through partnerships facilitating digital identity adoption in markets like India and Portugal aligned with cross-border trade agreements—signaling niche specialization though exact contract impacts are unspecified.

Demand Drivers

Several macro trends favor BIO-key’s business model:

Rising Enterprise MFA Adoption: As organizations upgrade beyond basic phone app or token MFA due to security shortcomings exposed by supply chain breaches or ransomware incidents.

Remote Work Expansion: Amplifies needs for passwordless MFA that function seamlessly across dispersed endpoints where users lack dedicated devices.

Government Digital Identity Initiatives: Increasingly mandate biometric authentication frameworks for citizens accessing services securely.

Cloud Computing Growth: Drives adoption of IDaaS platforms integrating with SaaS applications requiring strong user provisioning controls.

These drivers align well with BIO-key’s solutions which aim to reduce cost per authentication while enhancing cybersecurity postures through biometrics deployment instead of legacy approaches [S1].

Risks and Limitations

Despite promising technology positioning, BIO-key faces critical risks:

Financial Sustainability: With an operating loss exceeding $6.8 million and net loss near $7.2 million in fiscal 2025 alongside escalating operating expenses more than offsetting gross margins (~77%), profitability remains elusive [S1][F1]. Continued net losses could constrain investment in R&D needed for platform evolution

Regulatory Compliance Risk: The Nasdaq delisting threat stemming from repeated filing delays impairs capital market access impacting share liquidity as well as external perceptions of governance rigor [S3][S17]

Competitive Intensity: Larger IAM providers benefit from scale economies capturing large enterprise footprints; cloud-native competitors might erode BIO-key’s market share absent rapid innovation or differentiated ecosystem integration.

Integration Complexity: Customers’ existing IAM frameworks using Microsoft, Okta or ForgeRock require seamless extensions via PortalGuard which may slow customer acquisition due to deployment challenges.

Supply Chain Dependencies: Hardware components sourcing—critical for fingerprint scanners—may expose BIO-key to component shortages or cost inflation impacting unit economics.

Economic Vulnerabilities: Potential downturns could delay IT spend cycles affecting new installations or enterprise renewals.

What To Watch Next

Near-term milestones will focus heavily on:

The outcome of the June 16 Nasdaq panel hearing concerning exchange listing continuation which will affect public market capital access.

Timely filing of overdue SEC periodic reports restoring regulatory compliance standing.

Execution progress toward expanding international deployments supporting digital ID initiatives which may provide scalable license fee streams.

Improvement in operating leverage reducing SG&A intensity relative to revenues given prior annual ratios exceeding total revenues by nearly double [S1].

Strategic partnerships enhancing platform integration into prominent IAM ecosystems to augment customer retention rates.

Financial Profile Highlights

Balance sheet metrics illustrate limited leverage; cash & equivalents stood at about $2.7 million against nominal total debt approximating $135 thousand as of mid-year 2025 resulting in positive net cash positions providing some liquidity cushion [F1]

This analysis synthesizes publicly filed financial statements and disclosure documents provided by BIO-key International Inc., combined with sector-native industry knowledge frameworks characteristic of biometric identification solutions providers. It does not constitute investment advice but aims to contextualize recent corporate events within the operational realities of the evolving multi-factor authentication marketplace.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments