byNordic Acquisition's Final Stretch: Capital Strategy and Deal Deadline Extension

byNordic Acquisition Corporation extends its business combination deadline to June 2026 amid tightening liquidity and mounting execution urgency.

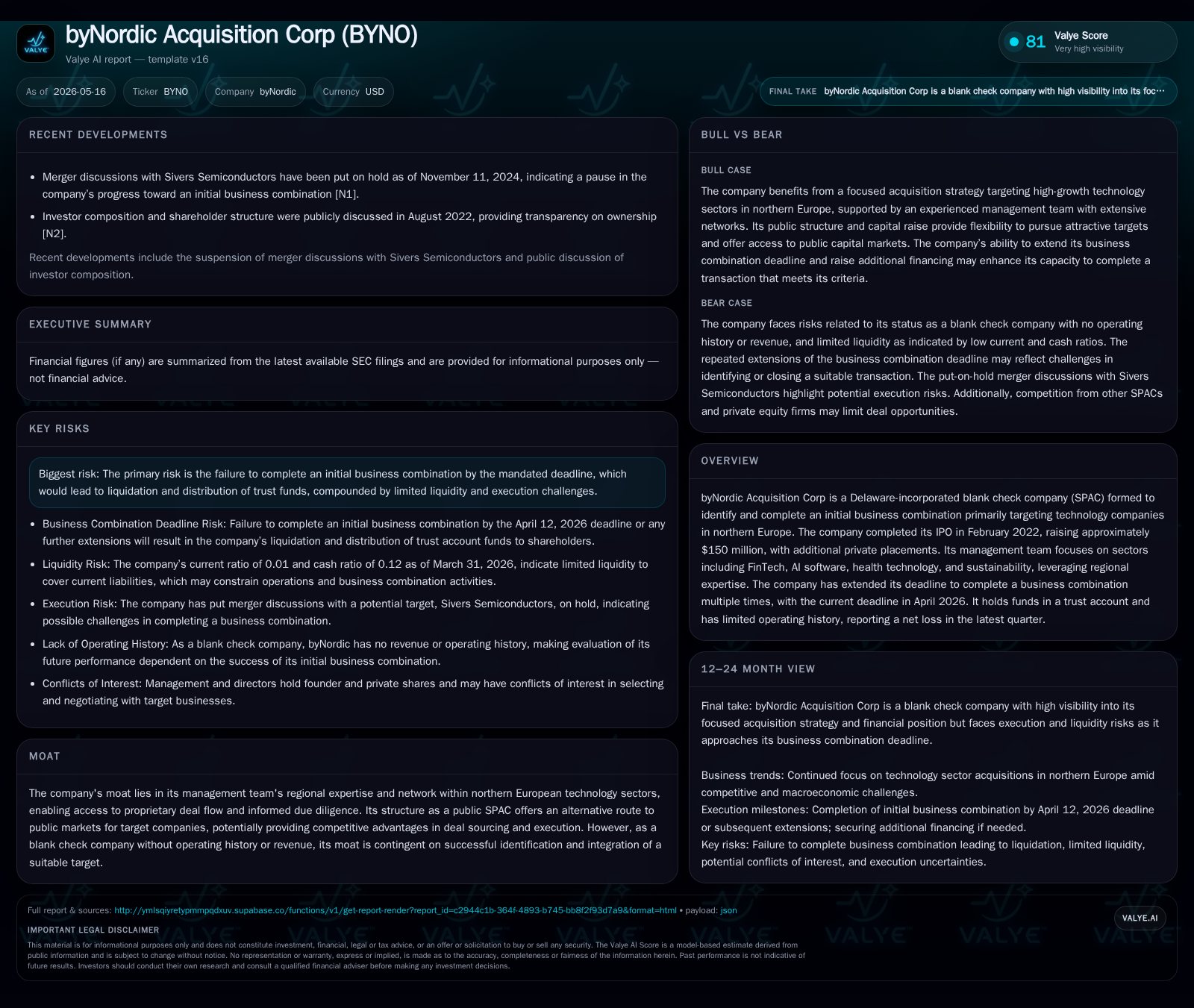

byNordic Acquisition Corp (BYNO), a SPAC focused on Northern European technology targets, has further extended its deadline to complete an initial business combination to June 12, 2026, marking the most recent in a series of extensions facilitated by incremental trust account top-ups. The company continues to operate with limited working capital and no revenue history, emphasizing the critical importance of executing a timely acquisition to avoid liquidation. BYNO’s business model leverages management's regional expertise to access proprietary deal flow in sectors like FinTech, AI, health tech, and sustainability, but it faces intense competition and geopolitical headwinds that constrain its deal sourcing. With liquidity under pressure and major milestones rapidly approaching, upcoming shareholder communications and potential transaction announcements will be pivotal.

Urgent Operating Update Reflecting Imminent Business Combination Deadline

byNordic Acquisition Corp (ticker BYNO) remains in a critical phase as it races toward its final deadline for completing an initial business combination. The latest quarterly filing (10-Q dated May 15, 2026) confirms no material changes in risk factors but underscores that operations continue under tightened cash conditions without any announced acquisition target as yet [S2]. In parallel event filings dated May 8 and April 9, the company detailed incremental trust account deposits of $17,470 each to fund rolling one-month extensions of the deadline—from May 12 to June 12, 2026 [S3][S4][S5]. This pattern of small-scale cash infusions orchestrated by the board echoes previous monthly extensions stretching back over a year.

Such repeated deadline pushes highlight BYNO’s urgency: it must either consummate a transaction imminently or face mandatory liquidation with distribution of trust funds back to public shareholders. The minimal incremental amounts deposited into the trust reflect constrained liquidity outside the protected funds held for redemption value.

byNordic Acquisition’s Business Model: Blank Check SPAC and Regional Niche Focus

BYNO operates as a traditional Special Purpose Acquisition Company (SPAC), raising gross proceeds of about $150 million through its February 2022 IPO which issued units composed of Class A common shares paired with redeemable warrants exercisable at $11.50 per share [S25][S1]. Supplementary private placements injected an additional $8.5 million from sponsors aligning founder interests with public investors.

The company has no standalone operating revenues or business activities; rather it acts as a capital vehicle seeking an attractive Northern European technology company—spanning Nordic countries, Baltics, UK/Ireland, Germany, France and Benelux—to merge with post-IPO. This geographically targeted mandate leverages management’s deep local expertise and networks which form BYNO’s principal strategic advantage [S25]. Key focus verticals include FinTech platforms disrupting traditional finance models; AI-driven software solutions gaining traction across industries; health technology innovations addressing clinical efficiency; and sustainable technologies aligned with increasing ESG focus.

The economics typical of such blank check entities mean all funds raised are held primarily in a trust account pending an acquisition that meets investor approval thresholds. Sponsors generally receive promote shares incentivizing a timely deal closing but bear dilution risk if no transaction materializes.

Industry Competitive Dynamics for Northern European Tech-Focused SPACs

The Northern European tech SPAC sector is becoming increasingly crowded amid broader macroeconomic uncertainties. Multiple contemporaneous SPACs compete for a limited pool of quality targets exposed to geopolitical tensions—most notably the ongoing war in Ukraine—which heightens regulatory scrutiny and capital market volatility impacting valuations [S1].

BYNO’s need for multiple deadline extensions reflects common challenges facing SPACs this cycle: intensified competition for attractive acquisitions driving up transaction costs; more cautious sponsor behavior limiting risky capital deployment; and shareholder reluctance inducing complex redemption dynamics particularly given in-the-money warrant strike prices ($11.50) that shape investor composition [S1][S3]. These factors collectively compress available runway for unclosed deals.

Catalysts Driving Demand for Northern European Technology Targets

Despite headwinds overall demand remains informed by structural growth themes in targeted sectors. Adoption curves accelerate especially in AI software where automation promises sweeping efficiency gains; FinTech companies benefit from digitization trends reshaping consumer financial services; health technology innovations including digital therapeutics gain regulatory momentum; sustainability-focused businesses attract policy support aligned with EU Green Deal initiatives [S1].

BYNO’s management team claims access to proprietary deal pipelines evolved through longstanding regional relationships—a potent differentiator amidst the standard SPAC scramble. This network potentially offers early-stage visibility on promising companies seeking alternatives to traditional IPO routes amid volatile equity markets.

However, specifics on candidate deal pipelines remain unpublished suggesting ongoing search activity without near-term closure certainty.

Key Risks Highlighting Execution Uncertainty and Liquidity Constraints

Execution risk dominates BYNO’s profile: failure to consummate an initial business combination by June 12 mandates liquidation under SEC rules resulting in fund disbursement net of expenses back to shareholders [S3][S4]. This binary outcome places enormous pressure on management performance and sponsor judgment.

Liquidity metrics further underscore vulnerability: based on data as of March 31, 2026, BYNO holds scant current assets ($128k) against towering current liabilities ($8.89 million), yielding an alarming current ratio near 0.01—conventionally indicating acute short-term solvency challenges [F1]. The low working capital is partially mitigated by approximately $1.05 million cash held earlier mid-2023 and a modest $600k total debt recorded related mainly to non-interest bearing promissory notes from affiliates supplying bridge working capital until combination closure [F1][S27].

Additional risks include potential dilution if equity issuances occur below prevailing market prices during combination structuring; regulatory approval uncertainties; political instability effects on target valuations especially given Russia-Ukraine conflict spillovers; unhedged exposure to investor redemptions disrupting deal financing assumptions; and intrinsic uncertainties around post-merger integration capabilities given no operational track record pre-combination [S1].

Critical Milestones and What To Watch as June Deadline Approaches

Investors should closely monitor imminent developments centered on:

- Official announcement(s) of target acquisition agreements or memorandum of understandings before mid-June.

- Notifications regarding shareholder meetings scheduled for voting on proposed combinations.

- Any further board decisions to exercise one-month deadline extensions funded by marginal deposits into the trust account.

- Potential indications of additional financing attempts via private placements or debt offerings disclosed in SEC filings.

- Shareholder redemption activity impacting available transaction financing capacity.

Given the absence of announced targets so far coupled with previous extension patterns these signals will decisively indicate whether BYNO can move beyond its SPAC status or will enter liquidation mode after June.

Latest Financial Snapshot: Liquidity Challenges in Context

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $127939 | |

| 2026-03-31 | ||

| Current liabilities | $9mm | |

| 2026-03-31 | ||

| Current ratio | 0.01x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Amount (USD) | Period End |

|---|---|---|

| Cash & Equivalents | 1,056,328 | |

| 2023-06-30 | ||

| Total Debt | 600,000 | |

| 2023-08-31 | ||

| Current Assets | 127,939 | |

| 2026-03-31 | ||

| Current Liabilities | 8,887,673 | |

| 2026-03-31 | ||

| Current Ratio (Assets/Liabilities) | 0.01 | |

| 2026-03-31 |

This stark imbalance illustrates BYNO’s precarious position: while holding some cash reserves historically sufficient for minimal operations early post-IPO stages, by Q1 2026 liquidity dwindled heavily relative to obligations potentially comprised largely of accrued fees or payable amounts related to administrative costs or sponsor advances. The nominal total debt represents interest-free bridge funding rather than strategic leverage employed for growth.

Overall this financial profile reflects typical SPAC lifecycle tension when approaching end-of-window periods without signed deals in sight—liquidity shortages force reliance on sponsor goodwill through minor trust replenishments just enough to keep deadlines alive temporarily but not indicative of sustained operational runway beyond imminent months.

This analysis is based solely on publicly filed SEC disclosures up through May 15th, 2026 ([S2], [S3], [S4], [F1]) without speculative forecasts or private information. It does not constitute investment advice but aims to provide a fact-based understanding of byNordic Acquisition Corp's operational context and trajectory at this crucial juncture.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments