Carnival Corp’s Record Q2 Highlights Strength and Strategic Unification

Carnival's June 2026 quarter showcases operational resilience and strategic advantages following unification of its dual-listed entity structure.

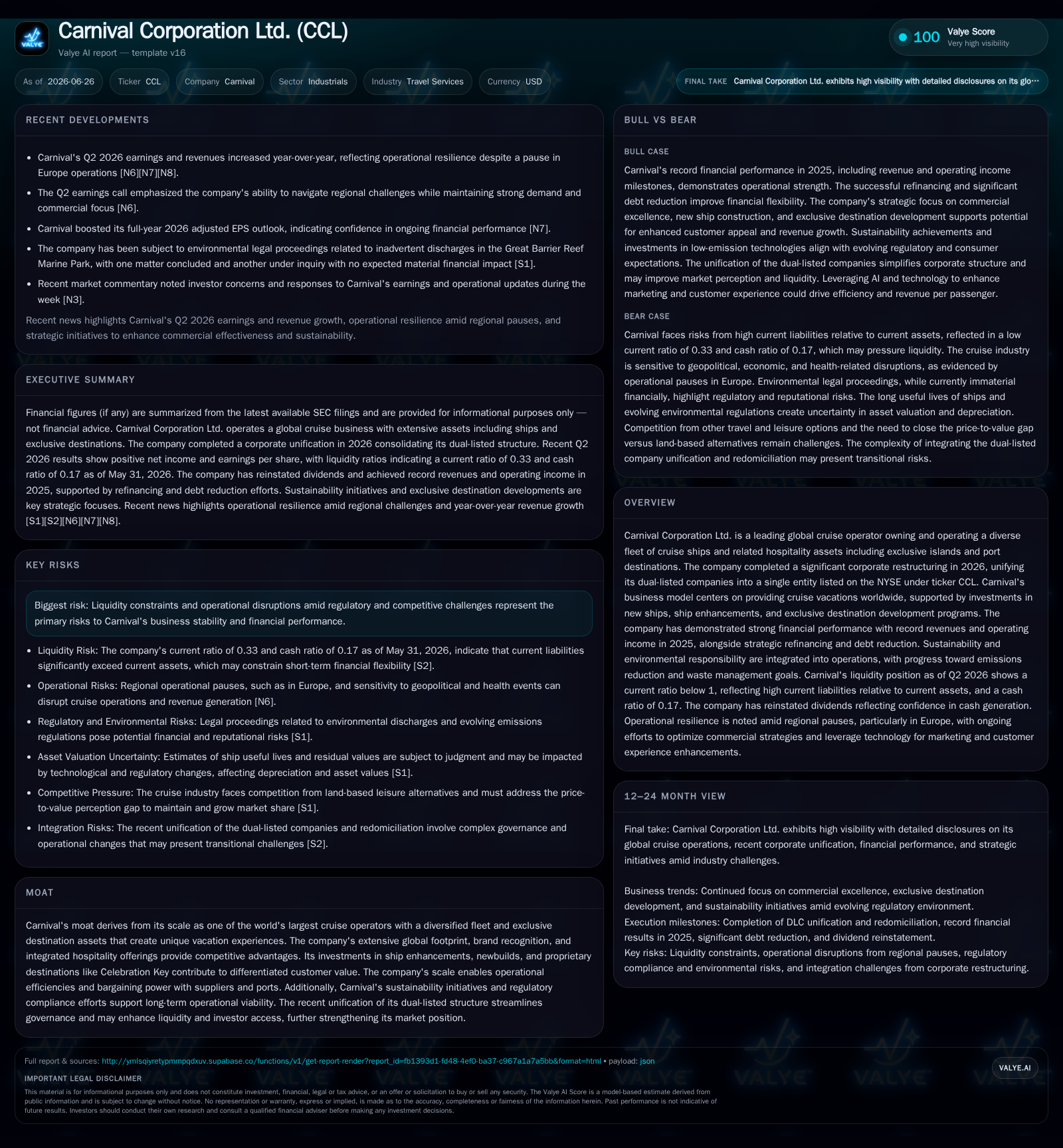

Carnival Corporation Ltd. reported record revenues, net yields, and adjusted net income for Q2 2026, buoyed by improvements in fleet utilization and passenger spending despite geopolitical headwinds. The company's recent unification of its dual-listed companies into a single Bermuda-based entity has streamlined governance and enhanced operational efficiency. Growth drivers include fleet modernization, exclusive destination developments, and expanded itineraries, while ongoing risks reside in liquidity constraints, fuel cost pressures, and geopolitical uncertainties. Monitoring capacity deployment and sustainability compliance will be crucial for continued momentum into FY26.

Second Quarter Performance: Records Set Post-Unification

Carnival Corporation Ltd.’s Q2 2026 results reflect a landmark period following the completion of its DLC unification in early May 2026. Consolidation of Carnival plc under the Bermuda-based Carnival Corporation Ltd. culminated in streamlined governance and de-listing from the London Stock Exchange for Carnival plc shares, with all common stock now trading solely as CCL on the NYSE [S6][S14]. This structural shift is mirrored in operational performance: Carnival posted record quarterly revenues alongside elevated net yields per passenger day and adjusted net income that beat consensus estimates [S2][S3][N4].

Operational execution benefited from improved Available Passenger Cruise Days (APCD) driven by higher fleet utilization across diversified itineraries despite a temporary pause in European operations due to geopolitical headwinds [S2][N3]. Occupancy rates showed resilience as itinerary planning effectively shifted demand geographically. The interplay between enhanced capacity usage and targeted pricing strategies contributed directly to upward momentum in net yield metrics—a core profitability lever in cruise operations.

The unification appears synergistic beyond capital markets: governance efficiencies have allowed for more centralized decision-making regarding fleet deployment, itinerary augmentation, and investment prioritization. Industry context benchmarks Carnival alongside peers like Royal Caribbean but places heavier emphasis on competitive moats tied to exclusivity of destination ownership combined with scale advantages.

Carnival’s Business Model: Revenue Streams and Customer Experience Drivers

Carnival's fundamental revenue model hinges on two intertwined pillars: passenger ticket sales underpin baseline cruise income while onboard spending—including premium dining, entertainment, retail, spa services—generates high-margin incremental revenue streams [S1]. Ticket prices vary with itinerary length, seasonality, ship class, and destination exclusivity; onboard revenue per passenger represents a strategic lever as customer experience enhancements drive discretionary spending.

The company’s proprietary exclusive destinations such as Celebration Key enhance pricing power by differentiating cruise offerings from competitors who primarily use shared or public ports. These destinations integrate hospitality infrastructure that extends the vacation ecosystem beyond the ship itself—bolstering guest satisfaction and loyalty metrics which are critical for repeat bookings and higher lifetime value.

Capital expenditures remain intensive within this model. Investments in ship newbuilds focus on integrating next-generation amenities that appeal to evolving customer preferences while refurbishments extend vessel longevity and maintain brand standards. Fleet modernization further supports operating efficiencies—lower maintenance costs, improved fuel performance—and thus can enhance operating margins over time. Alongside these physical assets is complex itinerary planning balancing consumer demand trends with travel regulations and geopolitical considerations to optimize occupancy rates and APCD.

Industry Positioning: Competitive Scale, Fleet Strategy, and Exclusive Destinations

Carnival’s scale ranks among global giant peers such as Royal Caribbean and Norwegian Cruise Line. Its distinct advantage arises from an especially diverse fleet composition coupled with ownership or controlling interests in multiple exclusive islands and private port destinations—an operational moat that fosters unique vacation experiences difficult for rivals to replicate.[S1]

The recent corporate restructuring has also fortified this position by dissolving corporate complexity inherent to its former dual-listed company structure. This unification enhances liquidity for investors via a singular listing vehicle on the NYSE under ticker CCL while simplifying compliance procedures aligned with Bermuda jurisdictional governance policies rather than the prior Panama domicile [S6][S14]

While other operators have introduced innovative onboard amenities or niche itineraries targeting burgeoning markets, Carnival's integration of destination ownership lowers competitive pressure through limited substitute experiences. Sustainability compliance efforts—such as emissions reduction targets and waste management programs—further solidify collective regulatory standing necessary for long-term operation amid tightening global maritime standards.

Growth Catalysts: Fleet Modernization, Destination Development, and Demand Trends

Key growth drivers spotlighted in recent filings include accelerating deliveries of modern ships equipped with advanced environmental technologies boosting guest satisfaction scores—a KPI linked directly to Net Promoter Scores (NPS) which impact repeat bookings [S1][S2]. These upgraded vessels also contribute favorably to operating expense ratios by reducing per unit fuel consumption amid inflationary cost pressures.

Destination development remains a high-impact growth vector evidenced by continued enhancement of Celebration Key facilities which attract premium clientele willing to pay price premiums reflective of exclusivity. Furthermore, expanding itineraries into emerging markets offers sustained demand potential supported by rising disposable incomes globally—a secular trend underpinning structural growth in leisure travel sectors.

Demand trends show robustness albeit nuanced by geopolitical disruption: management commentary highlights adaptive itinerary planning responding dynamically to the prolonged Europe pause without materially denting overall occupancy across other regions such as the Caribbean or Asia-Pacific [N3][S2]. Onboard revenue per passenger also incrementally increased driven by tailored experiences aligned with shifting guest expectations for health safety post-pandemic.

Risks and Watchpoints: Operational Challenges and Market Sensitivities

Fuel cost volatility represents an ongoing margin risk given substantial consumption rates across extensive sailing schedules; while hedging mitigates some exposure it cannot fully eliminate market-driven variability impacting operating expenses [S1]. Regulatory compliance demands are intensifying worldwide especially concerning emissions reductions mandated by maritime authorities; failure to meet these could result in fines or operational delays.

Reputational risks emanate from potential operational incidents—technical failures or health-related outbreaks—which can cause voyage interruptions or negative media coverage rapidly amplified through social media channels complicating crisis response efforts [S1]. Macroeconomic factors such as inflationary pressures or recession fears can depress discretionary consumer travel budgets adversely affecting booking levels.

"What to Monitor": Upcoming Guidance and Industry Signals Ahead of Q3

Attention should be focused on progressive quarterly updates related to capacity deployment decisions during peak summer seasons where full utilization is critical for margin realization post-fixed-cost absorption [N13][S2]. Tracking shifts in geographic itinerary mixes particularly any further European operational reinstatements or extended pauses informs risk-adjusted demand forecasts.

Management’s updated full-year guidance revisions will serve as barometers for confidence in sustained recovery trajectories amid external headwinds. Progress against sustainability targets remains an important signal both for regulatory adherence and evolving traveler preferences increasingly sensitive to environmental stewardship claims.

Finally, financial liquidity markers including cash flow generation rates relative to planned capital expenditures provide insight into potential funding needs or dividend policy adjustments going forward.

Financial Snapshot Summary

Carnival closed Q2 2026 with record revenue milestones underpinning adjusted net income advances reflecting efficient cost control measures combined with favorable pricing dynamics [S2][F1]. The company's liquidity profile benefits from over $2.2 billion cash reserves juxtaposed against modest total debt levels recorded at approximately $211 million dating back nearly 18 months; this translates into a net cash position conducive to ongoing investment requirements though working capital ratios suggest tight short-term balance sheet flexibility [F1].

Overall leverage appears conservative relative to asset base given scale economies leveraged across its extensive cruise ship fleet complemented by proprietary destination holdings supporting strong cash conversion dynamics intrinsic to cruise sector business models.

Disclaimer: This analysis is based exclusively on information publicly disclosed through SEC filings dated up to June 26, 2026, company press releases, and reputed published news sources referenced herein. It avoids speculative assertions unsupported by direct evidence. The content does not constitute investment advice or research views.

Financial position in context

As of 2026-05-31, companyfacts shows $2.2bn in cash and equivalents [F1]. Current assets of $4.5bn and current liabilities of $13.4bn imply a current ratio near 0.33x for 2026-05-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments