CareCloud, Inc. Returns to Profitability with Expanding SaaS and RCM Services

CareCloud leverages technology-enabled services and AI to drive revenue cycle management growth despite offshore operational risks.

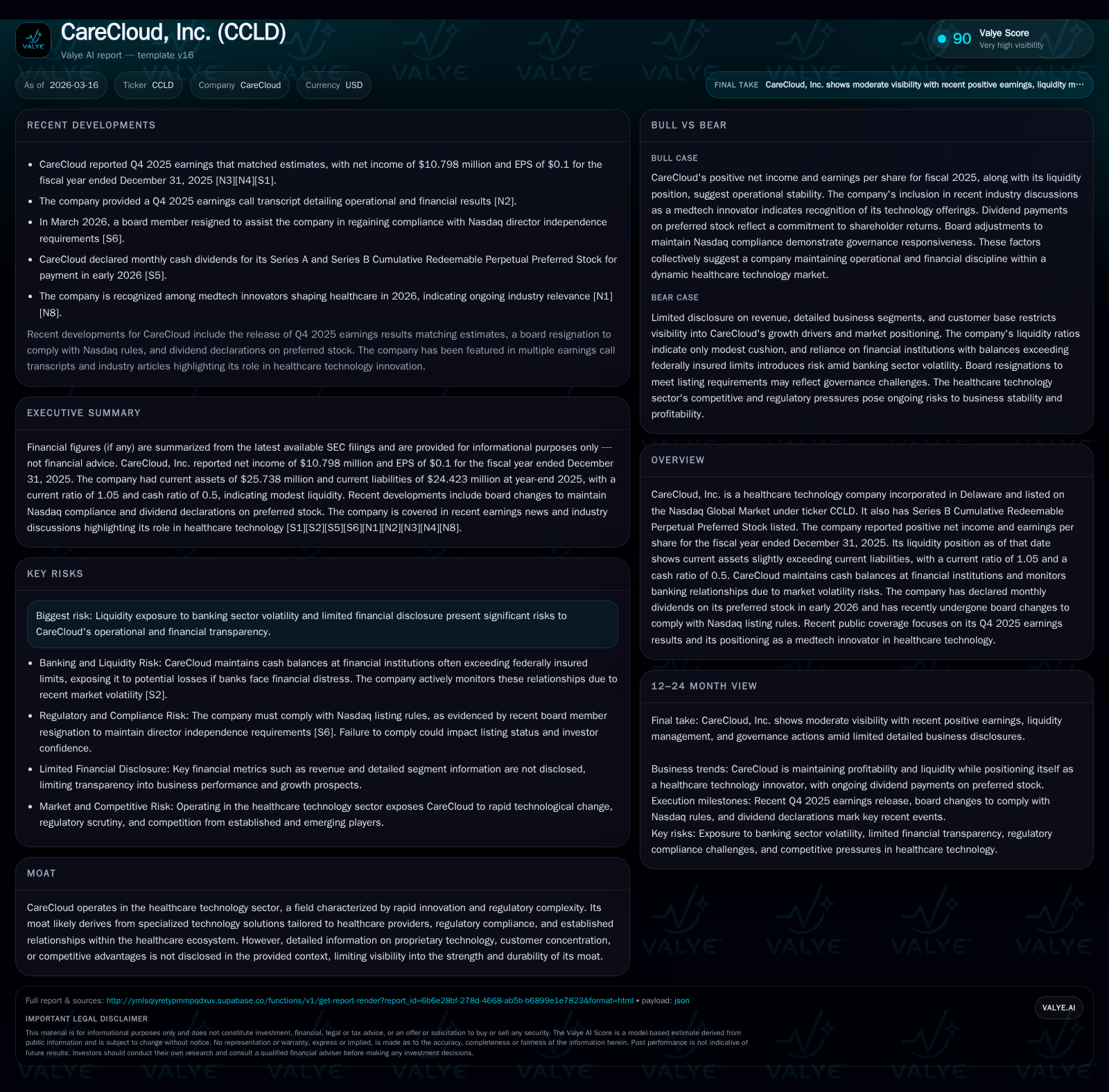

CareCloud, Inc. reported positive net and operating income for fiscal 2025, marking a significant turnaround from prior years. The company’s growth has been propelled by expansion in technology-enabled revenue cycle management and cloud-based healthcare software, aided by AI-driven solutions. However, its reliance on offshore operations in Pakistan and Sri Lanka introduces geopolitical and regulatory risks that could disrupt performance. CareCloud maintains modest liquidity with current assets just exceeding liabilities and continues dividend payments on its preferred stock while evolving board composition to meet Nasdaq compliance requirements.

Executive Summary

CareCloud, Inc., listed on Nasdaq as CCLD, is a healthcare technology company specializing in technology-enabled revenue cycle management (RCM) services augmented by proprietary cloud-based software solutions. After enduring sizable losses in fiscal year 2023, CareCloud achieved positive operating income ($11.3 million) and net income ($10.8 million) in fiscal year 2025, according to their latest SEC filings [F1]. This financial recovery reflects the company's continuing strategy of pairing AI-driven applications with outsourced medical billing, coding, credentialing, and claims clearinghouse services to optimize provider revenue cycles within complex regulatory environments [S1].

Past Growth and Historical Performance

CareCloud’s business model hinges on leveraging a lower-cost offshore workforce—approximately 3,300 employees primarily located in Pakistan’s offices—to deliver scalable RCM services alongside cloud-based software products including electronic health records (EHR) and practice management systems [S1]. Historically, the company faced significant financial headwinds culminating in a net loss near $48.7 million in FY2023 [F1]. This loss was attributed partly to investments in platform development and integration.

However, FY2024 initiated a turnaround with net income returning to $7.9 million and operating income rising accordingly [F1]. By FY2025 these gains consolidated into steady profitability:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 11 | 29 | 11 | 5 | +37.5% |

| 2024 | 8 | 21 | 9 | 2 | +116.1% |

| 2023 | -49 | 15 | -47 | 3 | -996.1% |

| 2022 | 5 | 21 | 7 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 24 | 18.1 |

| 2024 | 19 | 15.8 |

| 2023 | 12 | -116.7 |

| 2022 | 19 | 5.3 |

Source: SEC companyfacts cache [F1].

Notably, operating cash flow increased by nearly 38% between FY2024 and FY2025 offsetting substantially higher capital expenditures aimed at expanding product capabilities, reflecting focused reinvestment in technology platforms [F1]. The company’s equity base expanded modestly following previous contractions tied to losses.

Business Model and Industry Positioning

CareCloud operates at the intersection of healthcare IT SaaS solutions and managed service provision—two segments experiencing secular growth due to increasing complexity in medical billing protocols, regulatory compliance demands (e.g., HIPAA), reimbursement structures under value-based care models, and provider burnout exacerbating staffing shortages . Its suite includes cloud-based EHRs designed for ease of use that integrate directly or complement outsourced billing workflows; this combination aims not only to improve collection rates but also enhance clinical workflows for clients ranging from small practices to large health systems across the U.S.[S1]

CareCloud’s moat appears grounded in its specialized AI-enabled automation applications coupled with the cost advantage derived from offshore operations in Pakistan—a significant differentiator relative to competitors relying on higher-cost domestic resources or less integrated solutions [S1]. However, this same offshore dependency exposes CareCloud to geopolitical risks including political unrest, sanctions adjustments, data transfer regulations abroad, currency fluctuations, infrastructure reliability concerns (e.g., power grid stability), as well as evolving client preferences potentially favoring onshore providers [S1]. These factors present ongoing operational leverage points balancing cost competitiveness against risk exposure.

Future Growth Prospects

Growth prospects hinge on several vectors:

- Expansion of AI-Driven Revenue Cycle Tools: Continued refinement of robotic process automation (RPA) within RCM promises incremental margin expansion by reducing manual coding errors and speeding claims processing.

- Scaling Cloud-Based Software Adoption: Increasing penetration with EHR/PM solutions among mid-sized practices transitioning from legacy systems creates upsell opportunities tethered to bundled service offerings.

- Healthcare IT Professional Services & Staffing: Addressing physician burnout through flexible staffing/professional services represents an adjunct growth area aligned with broader industry workforce constraints.

- Regulatory Tailwinds: Stimulus initiatives or incentive programs encouraging healthcare digitization may further boost adoption rates. However, sustaining momentum requires navigating persistent risks around offshore operations resilience—the company emphasizes its dependence on Pakistan offices for roughly estimated labor cost savings of approximately five-sixth versus comparable U.S.-based roles—and sensitivity to international trade constraints or direct government interventions targeting cross-border data flows or payments compliance like FCPA enforcement nuances [S1].

Forecasts / Milestones / Expectations

While explicit forward guidance was not detailed in disclosed documents or recent earnings materials [N1][S3], milestones to watch include:

- Progress on regaining full Nasdaq compliance as board reshuffling unfolds following recent director resignations/deaths affecting independence criteria [S16][S19][N1].

- Further margin improvement driven by optimized mix toward higher-margin SaaS products versus lower-margin outsourcing services.

- Enhanced automation deployments expected to reduce cost structures over subsequent fiscal periods.

- Maintenance or incremental expansion of monthly preferred stock dividends declared for early-to-mid-2026 evidences free cash flow availability for capital return policies albeit modestly sized given ongoing reinvestments [S13][S23].

Returns / Capital Allocation

CareCloud achieved an approximate return on equity (ROE) of around 18% based on the ratio of trailing fiscal year net income ($10.8 million) over average equity ($59.5 million) indicating improved profitability returns after years of losses [F1]. Operating cash flow generation remains robust at $28.6 million FY2025 with capital expenditures rising sharply signaling strategic investments — resulting in free cash flow around $23.8 million [F1].

Capital allocation highlights include monthly dividend declarations on cumulative redeemable perpetual preferred stock through at least April 2026 [S5][S13] indicating shareholder distributions prioritized alongside balance sheet health considerations amid currently tight liquidity metrics: the current ratio stands barely above parity at roughly 1.05 while the cash ratio measures approximately .50 reflecting moderate unencumbered liquid assets versus short-term obligations at year-end [F1][S2]. There have been no recent common stock buybacks documented since FY2017 suggesting a conservative stance possibly driven by capital preservation objectives.

Risks

Material risks relate predominantly to business continuity surrounding offshore operations which account for the majority of headcount performing development, customer support, coding/billing activities primarily from offices in Pakistan (98%) plus Sri Lanka [S1]. Political instability or regulatory shifts—including export controls or changes linked to U.S./foreign sanctions regimes—could impose disruptions with material impact given labor cost advantages underpinning competitive pricing materialize only if current offshore delivery models persist unhindered.

Other challenges include foreign currency volatility impacting operational costs or repatriation flows; potential client migration preferences favoring domestic providers; cybersecurity or data privacy breaches leading to reputation damage; and legal exposures referenced through settled contractual disputes noted historically but without immediate ongoing litigation threat disclosed at present [S1][S12]. Financially the company holds balances exceeding federally insured bank limits thereby exposing it indirectly to banking sector turbulence emerging across regional banks amid persistent market volatilities necessitating proactive liquidity monitoring efforts reported during late-2025 filings [S2].

Corporate Governance Update

The company proactively addressed board governance gaps triggered by the passing of an independent director late November 2025 as well as by voluntary resignation effective March 2026 aiming compliance restoration under Nasdaq Listing Rule requirements for board independence majorities and audit committee composition prior to November annual shareholder meeting deadlines slated within next year’s timeframe [S16][S17][S19][N1]. Leadership transitions implemented effective January included executive adjustments enhancing strategic focus around CEO responsibilities while retaining key executives under updated employment terms with severance protections acknowledging competitive talent retention imperatives amid sector labor tightness [S24][N2].

Conclusion

CareCloud’s recent return to profitability marks a pivotal stage supported by balanced execution across AI-enabled SaaS offerings combined with specialized outsourcing services tailored for healthcare providers’ revenue cycle complexities facing digital transformation pressures industry-wide. While appreciating inherent dependency risks related to offshore operations residing amid geopolitical flux—especially concentrated employee bases subject to localized socio-political disturbances—the firm’s ability to generate robust operating cash flow fosters sufficient runway for both growth reinvestment and preferred dividend commitments.

Monitoring developments around regulatory landscapes affecting export controls or data transfers alongside corporate governance adherence will remain key focal points going forward. Investors seeking insights should also observe product adoption trends that validate upgrade trajectories from legacy systems toward next-generation cloud deployments augmented by automation advancements crucial for competing effectively within the evolving medtech ecosystem.

This analysis is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments