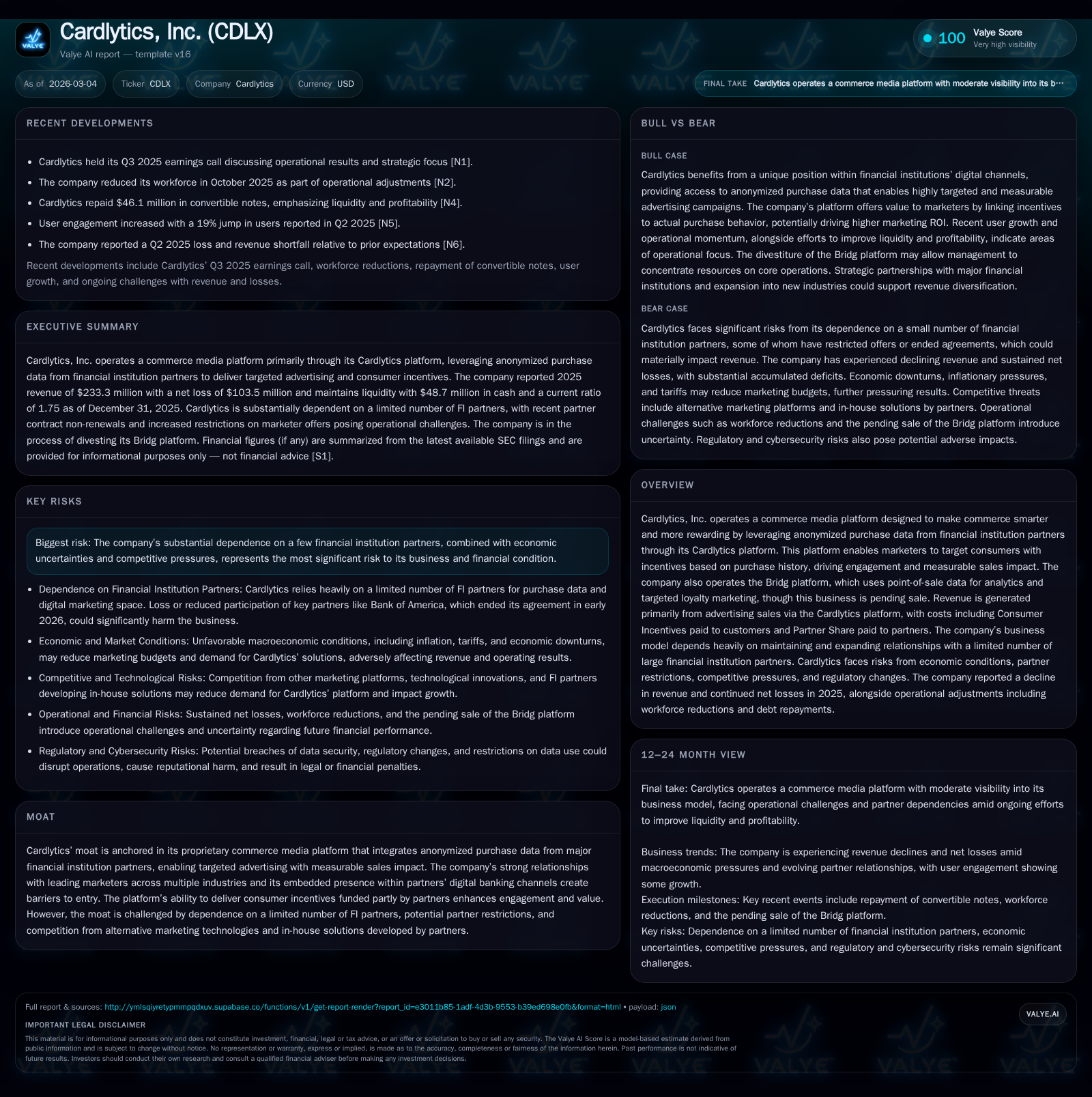

Cardlytics Faces Growth Challenges Amid Revenue Declines and Heavy FI Partner Dependence

The company's commerce media platform leverages anonymized financial data but grapples with narrowing revenue and ongoing losses.

Cardlytics operates a commerce media platform that uses anonymized purchase data from financial institution partners to drive targeted advertising through consumer incentives. Over the past several years, Cardlytics has experienced declining revenues, hitting $233 million in 2025, down 16% year over year from 2024, while continuing to report substantial net losses. The company’s growth prospects hinge on expanding partnerships and diversifying marketers but are constrained by macroeconomic uncertainties and dependence on a few large financial institution partners. Liquidity remains adequate following debt refinancing and capital raises, but operating cash flow improvements have yet to translate into profitability.

Company Overview

Cardlytics, Inc. operates a proprietary commerce media platform that integrates anonymized purchase data from leading financial institution (FI) partners with the intent of delivering targeted advertising campaigns based on consumers’ spending behavior. Central to its offering is the Cardlytics platform embedded within FI digital banking channels where consumers receive tailored incentives designed to promote engagement and measurable incremental sales for marketers.

A secondary offering, the Bridg platform—focused on leveraging point-of-sale (POS) data for merchant analytics and targeted loyalty marketing—is presently slated for sale, indicating strategic streamlining toward Cardlytics’ core FI partnerships [S1][S21].

Historical Performance and Key Financials

The company’s top line has been under persistent pressure through recent years. Revenue peaked near $309 million in 2023 before contraction began. In fiscal year 2025, total revenue dropped substantially to approximately $233 million, down about 16.2% year over year from $278 million in 2024 [F1]. This decline corresponds strongly with noted macroeconomic headwinds such as inflationary pressures and the introduction of new baseline tariffs on U.S. imports imposed in April 2025 [S1][S28]. These factors have notably dampened marketing budgets across Cardlytics’ core industries—restaurants, brick-and-mortar retail, telecommunications, among others—regions cumulatively representing the majority of its advertising sales.

Operating results have remained negative but showed improvement with operating losses narrowing from nearly $195.5 million in 2024 to about $101.8 million in 2025 (approximately a 48% improvement). Net income followed a similar trend with losses around $103.5 million in the latest reported year compared to nearly $189.3 million the prior year [F1].

Positive signs emerge from cash flow management: operating cash flow turned positive at roughly $9.3 million last year after several years of negative cash flow marked by operational investment and legacy costs [F1]. Capital expenditure intensity has been scaled back considerably since previous years; capex fell notably from $1.56 million in 2024 down to only $480,000 in 2025, reflecting more conservative investment during uncertain growth prospects [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 233 | -103 | 9 | -102 | -16.2% | +45.3% |

| 2024 | 278 | -189 | -9 | -195 | -10.0% | -40.5% |

| 2023 | 309 | -135 | 0 | -136 | +3.6% | +71.0% |

| 2022 | 299 | -465 | -54 | -458 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 9 | 1590.2 | |

| 2024 | 0 | -10 | -270.5 |

| 2023 | 0 | -1 | -99.9 |

| 2022 | 40 | -55 | -219.9 |

Source: SEC companyfacts cache [F1].

Note: Operating income (OpInc) and Net Income reflect losses.

Business Model Drivers and Moat

Cardlytics’ competitive advantage centers on its ability to harness anonymized purchase data accessed through exclusive or semi-exclusive partnerships with leading financial institutions [S21]. This fairly unique data asset fuels targeted marketing campaigns where firms offer direct consumer incentives for qualifying purchases—a mechanism that helps demonstrate attributable sales lift unlike many traditional digital ad efforts.

Their embedded presence within FI digital portals affords both scale and fidelity that constitute high barriers for competitors without similar direct bank access . Moreover, partner-funded consumer incentives partially subsidize promotional costs increasing effectiveness for advertisers while enhancing customer stickiness.

However, this moat is challenged by reliance on a concentrated number of FI data partners who retain leverage over access terms and conditions [S12]. Furthermore, competitive pressures arise from alternative digital marketing platforms including those deploying AI-driven targeting independently or marketers building custom internal solutions harnessing first-party data.

Risks and Constraints on Growth

Recent tariff increases—including a new universal baseline tariff of roughly 10% on all imported goods effective April 2025—coupled with inflation have pressured key sectors such as restaurants and retail that represent much of Cardlytics’ advertiser base [S1][S28]. These economic constraints lead marketers to reduce or delay advertising spends, directly impacting Cardlytics’ revenue growth.

Additionally, quarterly results remain volatile partly due to seasonality in marketing budgets which concentrate spending disproportionately around holidays creating uneven cash flow dynamics [S17]. The dependency on timely dealer payments and collection cycles further adds complexity to cash conversion efficiency.

Given significant accumulated net losses exceeding $1.4 billion since inception as of end-2025 and recurring operating deficits despite smaller magnitudes recently [F1], sustainable margin expansion will require successful scaling of revenues beyond existing core partnerships as well as diversification across more stable market segments.

Recent Capital Structure Updates & Liquidity Position

In early April 2024, Cardlytics issued approximately $172.5 million principal amount of Convertible Senior Notes due in 2029 bearing a coupon rate of approximately 4.25%. Proceeds primarily funded full repayment of its outstanding principal on the older higher-coupon convertible notes issued back in September 2020 at favorable terms resulting in a gain on extinction recognized during that period [$13 million gain] [S5][S7][S20].

The company maintains an asset-backed revolving credit facility (termed as the "2018 Loan Facility") which has undergone successive amendments increasing borrowing capacity incrementally up to potentially $75 million; the line's maturity was extended into April 15, 2028 [S6][S8][S16]. As of fiscal year-end December 31, 2025, net borrowings under this facility totaled approximately $40 million with unused credit availability around $8.5 million [F1][S11]. Interest rates are linked primarily to prime plus an adjustable spread ranging near ~0.125–0.25% post amendments.

Cash reserves stood at roughly $49 million as of December end-2025 held largely in liquid money market instruments and U.S Treasury bills yielding around mid-single digits (~4%) [S11][S18]. With positive working capital approximating $59 million (current ratio ~1.75x), liquidity appears sufficient for near-term obligations absent significant capital expenditures or acquisitions [F1][S11].

Equity stands slightly negative at approx -$6.5 million at year-end reflecting cumulative losses though recent quarters show some stabilization [F1]. There were no share buybacks conducted after historically modest repurchase activity ($40 million repurchased back in FY22 only) [F1][S24]. Instead equity financing through an at-the-market program raised roughly $48 million gross proceeds during early-to-mid-2024 providing additional balance sheet flexibility [S23][S29].

Future Growth Outlook – What To Watch For (Analysis)

Cardlytics’ trajectory hinges heavily on its ability to:

- Deepen relationships with existing FI partners while onboarding additional banks domestically or internationally.

- Expand marketer adoption across varied verticals beyond legacy strongholds like restaurants or cable providers.

- Successfully divest or otherwise optimize non-core operations like Bridg so it can sharpen focus on scalable commerce media solutions.

- Navigate macroeconomic headwinds including tariff impacts which may linger or evolve unpredictably impacting client marketing budget allocations.

- Leverage emerging technologies such as AI/ML within its analytics stack while managing attendant risks around privacy compliance and AI explainability [S25].

- Sustain operational efficiencies that progressively narrow losses while converting improving cash flow into positive free cash flow metrics more consistently.

Key milestones would include tangible signs of revenue stabilization or inflection upward following effective partner expansions; successful pact announcements; quarterly margin improvements; possible re-expansion of buybacks or dividend declarations once profitability stabilizes; plus handling regulatory or litigation risks effectively if they surface again given past stockholder activism episodes [S12][S21].

Capital Allocation Considerations

Operationally generated cash flow is still emerging: full-year operating cash flow swung positive reaching about $9 million last reported year mostly reflecting improved working capital cycles against notable prior period outflows [F1]. Capital expenditures remain modest (~$480k), consistent with a software platform company conserving resources amid uncertain top-line growth environment.

No dividends are declared nor buybacks conducted recently indicating capital retention prioritizes liquidity preservation amidst ongoing loss absorption [F1][S24]. Debt service obligations have been rationalized through refinancing moves reducing interest burden though leverage remains moderate given subpar earnings performance relative to scale.

Return metrics such as ROE are distorted by persistent net losses yielding an approximate negative ratio but improving trends highlight potential stemming from fixed-cost leverage benefits if revenue erosion slows or reverses soon enough [F1].

Summary Assessment

Cardlytics presents a compelling yet challenging case within commerce media leveraging anonymized banking transaction data powering targeted incentive-based marketing campaigns uniquely positioned within FI digital ecosystems. Its moat derives principally from exclusive partner integrations driving differentiated attribution capabilities not easily replicated by generalist ad tech providers. Yet the company faces meaningful top-line contraction pressures predominantly due to macroeconomic slowdowns across its primary marketer segments coupled with risks tied to concentrated partner dependency. Liquidity accessibility remains ample supported by recent convertible debt issuances refinanced at lower cost and augmented equity raises providing operational runway. Future growth dynamics will be tethered closely to successful partnership expansions alongside tighter margin control and adaptation amidst evolving regulatory landscapes especially around privacy and AI applications. Continuous monitoring of revenue trends relative to seasonalities plus evolving tariff impacts should be prioritized alongside scrutiny of debt covenant compliance given capital structure complexity. Ultimately, Cardlytics embodies the tension between proprietary data-powered innovation against execution risks elevated by external economic adversities challenging profitable scale-up prospects currently still unrealized fully.

This analysis synthesizes publicly available SEC filings through March 4, 2026 ([F1],) without speculative projections or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments