CEVA INC’s Revenue Growth Outpaces Rising Geopolitical and Trade Risks

CEVA INC demonstrates strong top-line expansion driven by licensing revenues while facing intensified challenges from geopolitical and trade uncertainties.

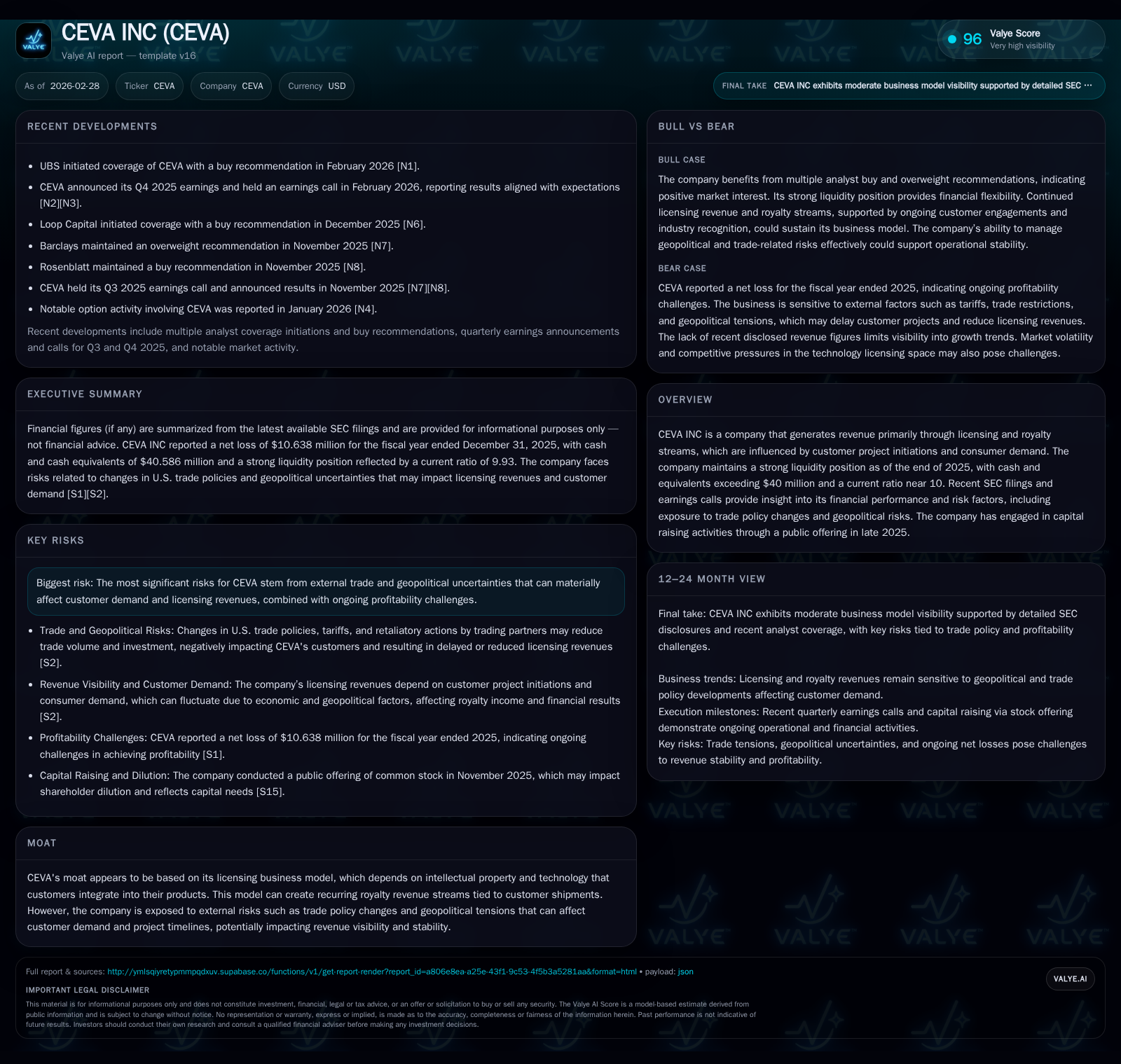

CEVA INC reported a 20.4% revenue increase in 2025, reflecting robust licensing income growth despite escalating operating losses. The company maintains a fortified liquidity position, with cash reserves above $40 million and a current ratio near 10, bolstered by a capital raise in late 2025. However, external headwinds from trade policy shifts and geopolitical tensions inject volatility into licensing revenues and customer project timing, complicating revenue visibility. Ongoing operating losses have led to negative returns on equity and free cash flow deficits, underscoring the strategic importance of prudent capital allocation going forward.

Revenue Trends and Profitability: Historical Performance Through 2025

CEVA INC’s financial trajectory through the latest fiscal year reveals a marked acceleration in revenue growth juxtaposed against amplified operating losses. In 2017, total revenue reached approximately $87.5 million, reflecting a hearty annual gain of 20.4% compared to the previous year [F1]. This gain primarily stems from the company's licensing model, where royalty income scales with customer product integrations and downstream consumer demand.

However, this top-line strength did not translate into profitability. Operating income declined sharply to -$11.3 million in the most recent fiscal year, a deterioration exceeding 50% from the prior year's operating loss of -$7.55 million [F1]. Net income mirrored this trend yet narrowed slightly relative to steep losses recorded in earlier years, registering a loss of approximately -$10.6 million [F1]. This pattern indicates continued pressure on margins despite healthier revenue flows.

The operating cash flow (CFO) profile remained challenged as well. CEVA registered negative CFO of -$3.36 million for the latest available fiscal year after generating positive cash flow in the prior year [F1]. Capital expenditures were steady at about $2.9 million, consistent with a controlled investment approach amid uncertain market conditions [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -11 | -3 | -11 | 3 | -21.1% |

| 2024 | -9 | 3 | -8 | 3 | +26.0% |

| 2023 | -12 | -6 | -13 | 3 | +48.8% |

| 2022 | -23 | 7 | -5 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 7 | -6 | -3.2 |

| 2024 | 8 | 1 | -3.3 |

| 2023 | 6 | -9 | -4.5 |

| 2022 | 7 | 3 | -9.0 |

Source: SEC companyfacts cache [F1].

Note: Some fiscal years exhibit incomplete data points due to source limitations; focus is placed on latest available annual figures [F1].

Licensing Model Dynamics and Key Growth Drivers

CEVA’s business hinges on technology intellectual property (IP) licensing enabling its customers to embed CEVA’s signal processing and AI-related algorithms into semiconductor chips and end-products [S5]. This licensing cadence generates upfront fees coupled with recurring royalty streams tied directly to customer shipment volumes — effectively allowing CEVA to monetize the IP integration lifecycle.

Customer project initiations serve as critical inflection points determining future royalty trajectories since projects funnel into production phases that trigger royalty payments [N1][N2]. The company benefits from a moat established through proprietary IP that competitors find challenging to replicate quickly but remains susceptible to royalty income volatility given reliance on external product demand cycles.

Industry practitioners recognize this model as sensitive to shifts in consumer electronics demand or chip order patterns — resulting in royalty income that can fluctuate materially quarter-to-quarter based on underlying shipment trends [S5]. This dynamic demands vigilant monitoring of project pipelines and client engagement durations which CEVA highlights as key drivers behind their guidance uncertainty.

Impact of Geopolitical and Trade Policy Changes on Business Stability

Trade policy flux poses one of the most salient risks for CEVA's licensing revenue stability, as documented repeatedly across quarterly filings spanning mid-2025 through early 2026 [S2][S6][S7][S8][S9]. The imposition of tariffs, evolving U.S.-China trade relations, retaliatory duties by global partners, and heightened political frictions collectively present 'trade compliance exposure' that influences customer behavior.

Such geopolitical tensions often prompt customers either to defer engaging new projects or re-evaluate existing supply chain commitments — leading to potential delays or cancellations impacting CEVA’s invoicing timelines [S2]. Furthermore, downstream market softness spurred by these dynamics may constrain end-user purchases, directly lowering units shipped and thereby diminishing CEVA’s royalty inflows.

This environment enforces considerable revenue visibility challenges for CEVA management who explicitly cite 'demand deferral' phenomena in their risk disclosures linked to shifting tariff regimes [S8]. The company's ongoing disclosures consistently stress this interplay as a key factor contributing to forecast volatility and budgeting complexity.

Capital Raising Efforts: Recent Public Offering and Liquidity Profile

Against a backdrop of widening recurring losses, CEVA has prudently bolstered its financial foundation via capital raising activities late in calendar year 2025 [S15][S16][N3]. On November 18, 2025, the company completed an underwritten public offering involving approximately three million shares priced at $19.50 per share with an option for an additional allotment exercisable within thirty days [S15].

This transaction refreshed CEVA’s liquidity position substantially; as of December 31, 2025, cash and equivalents stood robustly at $40.6 million — an important cushion given operational cash burn [F1]. Concurrently, the firm reported a current ratio approaching ten (9.93), signaling strong short-term asset coverage relative to liabilities which remain modest at around $28.7 million.

The capital structure enhancements grant flexibility amid ongoing margin pressures while equipping management with resources to selectively invest or navigate near-term uncertainty without excessive reliance on debt markets [S23][S24]. Such resilience is crucial for sustaining operations during periods marked by external shocks affecting customer conversion cycles.

Operating Cash Flow, Capital Expenditures, and Return Metrics

Despite improved revenue trends, CEVA posted negative operating cash flow of nearly $3.4 million in the latest fiscal year reflecting elevated working capital needs or timing differences inherent in royalty collections versus costs disbursed [F1]. When factoring capital expenditures—steady near $2.9 million annually—the resulting free cash flow remains negative at roughly -$6.28 million.

This persistent free cash outflow underscores the capital intensity associated with maintaining technology development platforms required for sustaining competitive moats in IP integration sectors.

Return metrics reflect these dynamics; using net loss against shareholder equity approximated at $336 million yields an estimated return on equity (ROE) around -3.2%, indicating that equity investments have yet to generate positive earnings despite growing asset bases [F1].

No dividends were declared per recent capital allocation disclosures while share buybacks continued at sustainable rates (~$7 million annually), suggesting selective shareholder value strategies amidst resource constraints [S18][S25].

Forecast Focus: Legal Proceedings, Customer Project Cycles, and Market Risks

Legal proceedings disclosed in latest filings introduce potential operational burdens though no material unexpected liabilities have emerged yet [S4]. Such legal risks add layers of uncertainty which affect long-range planning alongside more palpable business cycle factors.

The central forecasting challenge remains tied to unpredictable client project initiation timings—a core driver for both licensing fees and downstream royalties—as highlighted during earnings calls earlier this year [N1][S3]. This variability tempers management’s ability to provide definitive guidance beyond qualitative color on pipeline health.

Monitoring shifts in regulatory environments or potential changes in trade agreements will be vital given their outsized influence on demand patterns detailed previously.

What to Watch: Milestones and Company Signals in Upcoming Quarters

Market participants should track several key metrics that could illuminate CEVA’s trajectory moving forward:

- Royalty revenue progression aligned with consumer electronics demand shifts,

- Updates on client project launches or contract renewals signaling pipeline vitality,

- Announcements regarding additional licensing deals or IP portfolio expansions,

- Regulatory developments impacting trade policies influencing customer sourcing decisions,

- Analyst coverage such as UBS’ initiation adding external perspective on valuation and prospects [N3].

Evidence from recent analyst notes may help calibrate expectations on how well CEVA manages macro-driven headwinds while executing its growth plan.

This analysis integrates publicly filed data points and news releases up through February 28, 2026 without extrapolation beyond documented facts or issuer disclosures. It aims solely to provide a detailed operational and financial overview without advocating any investment action or opinion.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments