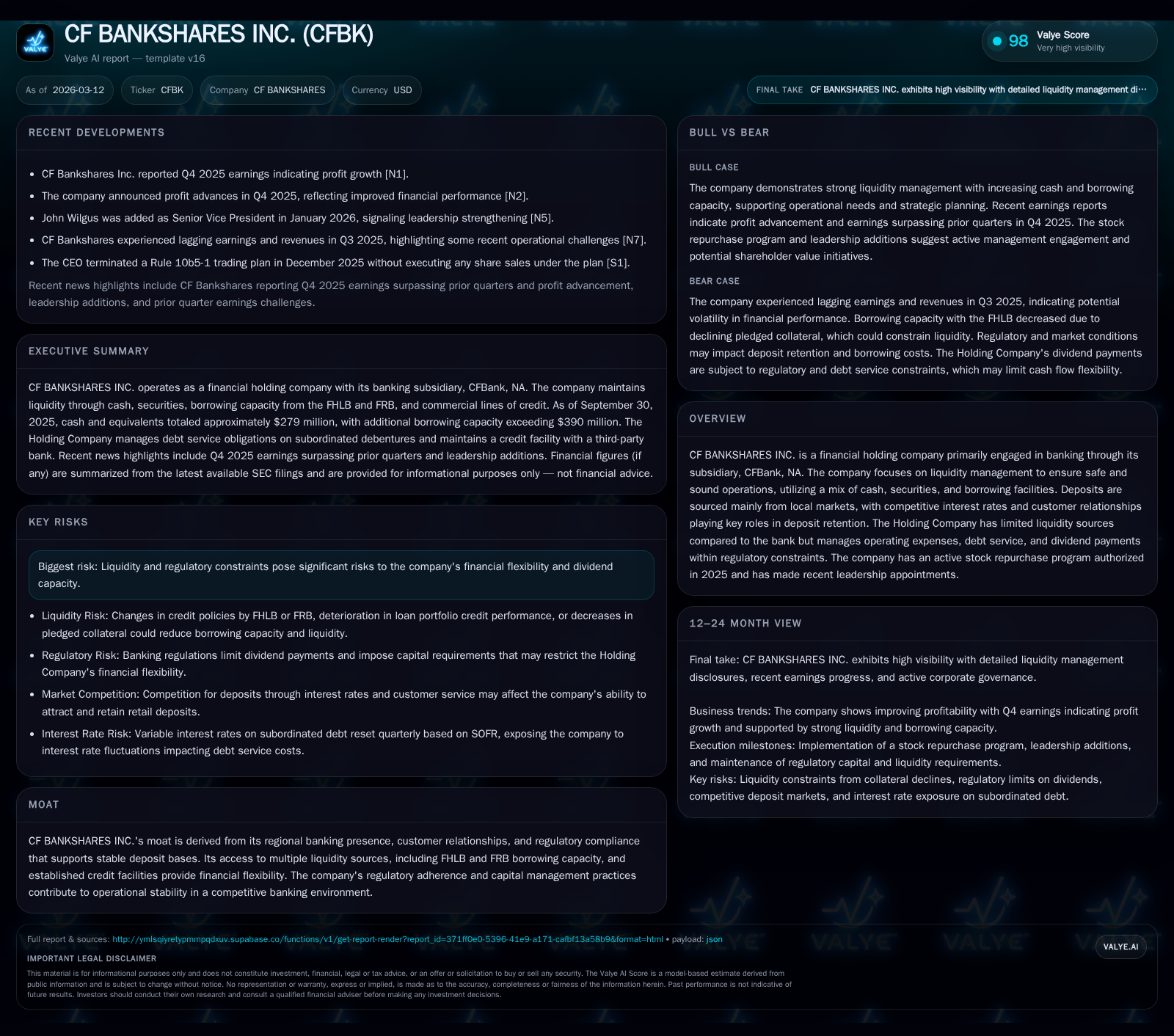

CF Bankshares Inc.: Earnings Momentum and Strategic Capital Management in 2025

CF Bankshares reports significant net income growth bolstered by disciplined liquidity and proactive capital deployment amid regulatory liquidity constraints.

In 2025, CF Bankshares Inc. demonstrated robust earnings momentum with a 31% increase in net income, driven by improved asset yields and deposit franchise strength. The company’s layered liquidity approach, incorporating cash reserves, securities, and borrowing capacity from FHLB and FRB, supports its operational resilience despite regulatory limits on the Holding Company’s flexibility. Capital allocation remains prudent through dividends and an active stock repurchase program authorized in 2025, funded by consistent free cash flow. Going forward, regulatory dividend caps and collateral quality for borrowing will be critical factors to monitor.

Record Earnings Performance and Historical Drivers

CF Bankshares Inc. recorded a notable rebound in earnings for fiscal year 2025 with net income reaching approximately $17.54 million, reflecting a 31% increase over the prior year’s $13.39 million [F1]. This surge marks recovery from the net income dip witnessed in 2024 following a relatively stronger year in 2023 ($16.94 million) and 2022 ($18.16 million), illustrating earnings momentum amid evolving interest rate dynamics.

The underlying drivers extend to solid asset yield trends within its banking subsidiary CFBank NA supported by a resilient retail deposit franchise focused mainly on local markets [N1], aided by competitive interest rates that help retain deposit balances in a competitive environment [S2]. Operating cash flow showed commensurate strength with a surge of nearly 32% to $18.69 million in FY2025 from $14.19 million in FY2024 despite capex maintaining tight discipline at $487 thousand (up modestly from $266 thousand) — favoring incremental investment without undermining free cash generation capabilities (see table below) [F1]. This careful control of operating expenses alongside steady deposit inflows underscores effective asset/liability management.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 18 | 19 | 487000 | +31.0% |

| 2024 | 13 | 14 | 266000 | -21.0% |

| 2023 | 17 | 18 | 661000 | -6.8% |

| 2022 | 18 | 40 | 905000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1948000 | 18 | 9.5 |

| 2024 | 1614000 | 14 | 7.9 |

| 2023 | 1476000 | 17 | 10.9 |

| 2022 | 1153000 | 39 | 13.0 |

Source: SEC companyfacts cache [F1].

The table reflects the volatile yet improving profitability landscape while equity growth signals balance sheet strengthening underpinning shareholder value creation.

Liquidity Framework and Regulatory Impact on Financial Flexibility

CFBank’s liquidity architecture is anchored by a multilayered framework blending readily liquid assets and credit resources essential to sustaining safe operations under stringent regulations [S2]. At September end of fiscal year ‘25, unpledged cash and securities rose significantly by about $40.9 million (+17%) year-over-year to reach $278.8 million — providing a robust liquidity buffer accessible without collateral restrictions [S4,S6,S2].

Complementing this are borrowing facilities including Federal Home Loan Bank (FHLB) advances with capacity around $181.6 million (down slightly due to lower pledged collateral chiefly residential loans), Federal Reserve Bank (FRB) primary credit borrowing increasing to approximately $145.7 million (+14%) driven by enhanced collateral pledges, plus two committed commercial lines adding another unused $65 million capacity unchanged since year-end '24 [S4,S6,S7].

These tiers are crucial for asset/liability management programs balancing expected loan demand fluctuations against deposit flows under competitive pressures and market conditions [S2]. However, the Holding Company operates with markedly less liquidity—primarily reliant on dividend inflows from CFBank plus possible debt/equity funding avenues constrained by regulatory approvals limiting dividends payable without prior consent as per current earnings coverage rules [S5,S7]. This bifurcation exposes capital allocation decisions at the Holding Company level to regulatory scrutiny restricting free cash movement.

Growth Outlook: Balancing Loan Demand and Deposit Retention

Management commentary indicates cautious optimism regarding loan book expansion predicated on stable but competitive local market activity where relationship banking provides meaningful sticky deposits critical to funding loans cost-effectively [N1,S3,S2]. Predominantly retail-focused deposits hinge on market-competitive interest offerings alongside excellent customer service – necessary levers given aggressive competition noted within CFBank's core geographies.

Interest rate environments have challenged net interest margin compressions industry-wide; however CF Bankshares benefits from strategic positioning along the yield curve ensuring nimble repricing aligned with deposit beta sensitivity [S3,N1]. The tuning of asset durations seeks to mitigate margin erosions while fostering moderate loan growth.

Nonetheless headwinds remain from heightened local competition for deposits driving marginal increases in funding costs potentially capping short-term asset yield expansions—an issue common among regional banks striving for efficient loan-to-deposit spreads.

Capital Allocation Strategy: Dividends, Buybacks, and Debt Service

Free cash flow enabled healthy returns to shareholders via gradual dividend increases—from roughly $1.15 million paid in FY2022 growing steadily to $1.95 million projected for FY2025—sustained under current earnings trends [F1]. Furthermore CF Bankshares actively pursues stock repurchases authorized initially early January ‘25 permitting buybacks totaling up to approximately five percent of outstanding shares (~325k shares). As of Q3 report date September '25 roughly fifty-four thousand shares had been repurchased with nearly two hundred eighty-nine thousand shares still available under this program emphasizing disciplined capital return focus manifested through tactical buybacks rather than aggressive leverage increases or large dividends expansions [S9,S11,S26].

The company’s subordinated debt obligations also shape capital deployment strategies: SOFR-linked trust preferred debentures incur annual debt service near $370k resetting quarterly at SOFR +3.112%, coupled with fixed-to-floating subordinated notes totaling $10 million yielding initial fixed coupons now converted to floating SOFR +4.402%, generating approximately $840k annual servicing costs as well—all manageable within current cash flows but considerable when sizing dividend or buyback decisions [S5,S7].

Additional credit facilities expanded CFBank’s Tier One capital base with an incremental revolving line infusion enhancing strategic flexibility but accentuating the need for cautious leverage management amidst evolving rates and regulatory oversight.

Key Milestones to Watch in 2026

Investors should closely watch quarterly earnings cadence for consistency in sustaining double-digit net income growth evident through FY25 results ([N1],[S3]). Regulatory developments impacting dividend caps or Holding Company liquidity could redefine shareholder return frameworks; any shifts there warrant attention.

Loan portfolio composition adjustments or concentration risks should continue being monitored given their potential effect on collateral valuations influencing FHLB/FRB borrowing quantities—a critical factor given past quarter fluctuations observed due to pledged collateral changes reported end-2024 vs mid-2025 [S4,S6,S27].

Finally execution velocity under ongoing repurchase authorization plans will signal confidence levels among management regarding valuation assessments and available capital buffers within regulatory guidelines.

Risk Profile: Regulatory and Liquidity Challenges

Primary risks stem from the tension between limited Holding Company liquidity sources vis-à-vis reliance upon regulated dividend flows from CFBank alongside scheduled subordinated debt obligations constraining financial elasticity [S8,S12]. Regulatory restrictions tether maximum allowable dividends to current plus prior two-year earnings reinforcing dependence on stable profit generation.

Potential tightening of credit policies by FRB or FHLB institutions could reduce permissible borrowing against pledged collateral if loan performance deteriorates or macroeconomic stress intensifies—an inherent systemic vulnerability common across banks leveraging these financing avenues [S8,S12]. Therefore operational vigilance regarding credit concentrations and compliance remains fundamental.

Operational Efficiency in Managing Asset/Liability Mix

Management continues optimizing investment distribution among highly liquid assets — cash equivalents expanded prominently in FY25 while balancing short-term securities purchases aligned with yield opportunities under secondary market conditions ([S2],[S6],[S10]).

This agility supports steady loan growth targeted at core markets while managing deposit cost pressures amidst competitive interest rate environments signaling proactive duration matching efforts enhancing overall net interest margin resilience despite pressure points common among thrift bank peers today.

Overall, CFBK manages its funding structure with prudent safeguards including liquidity buffers well above minimal requirements – key considerations underpinning safe operations even within evolving economic conditions prone to volatility impacting local market lending dynamics.[S2]

Disclaimer: This analysis is based exclusively on publicly available documents filed by CF Bankshares Inc., including SEC filings dated through March 12, 2026 ([F1]-[S29]) and referenced news reports ([N1]-[N3]). It does not constitute investment advice or recommendations but aims to provide an integrated view grounded in disclosed data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments