C & F Financial Corp’s Balancing Act: Growth Drivers, Regulatory Challenges, and Returns

Loan growth and margin expansion powered C & F Financial Corp’s 2025 earnings surge despite regulatory and operational headwinds.

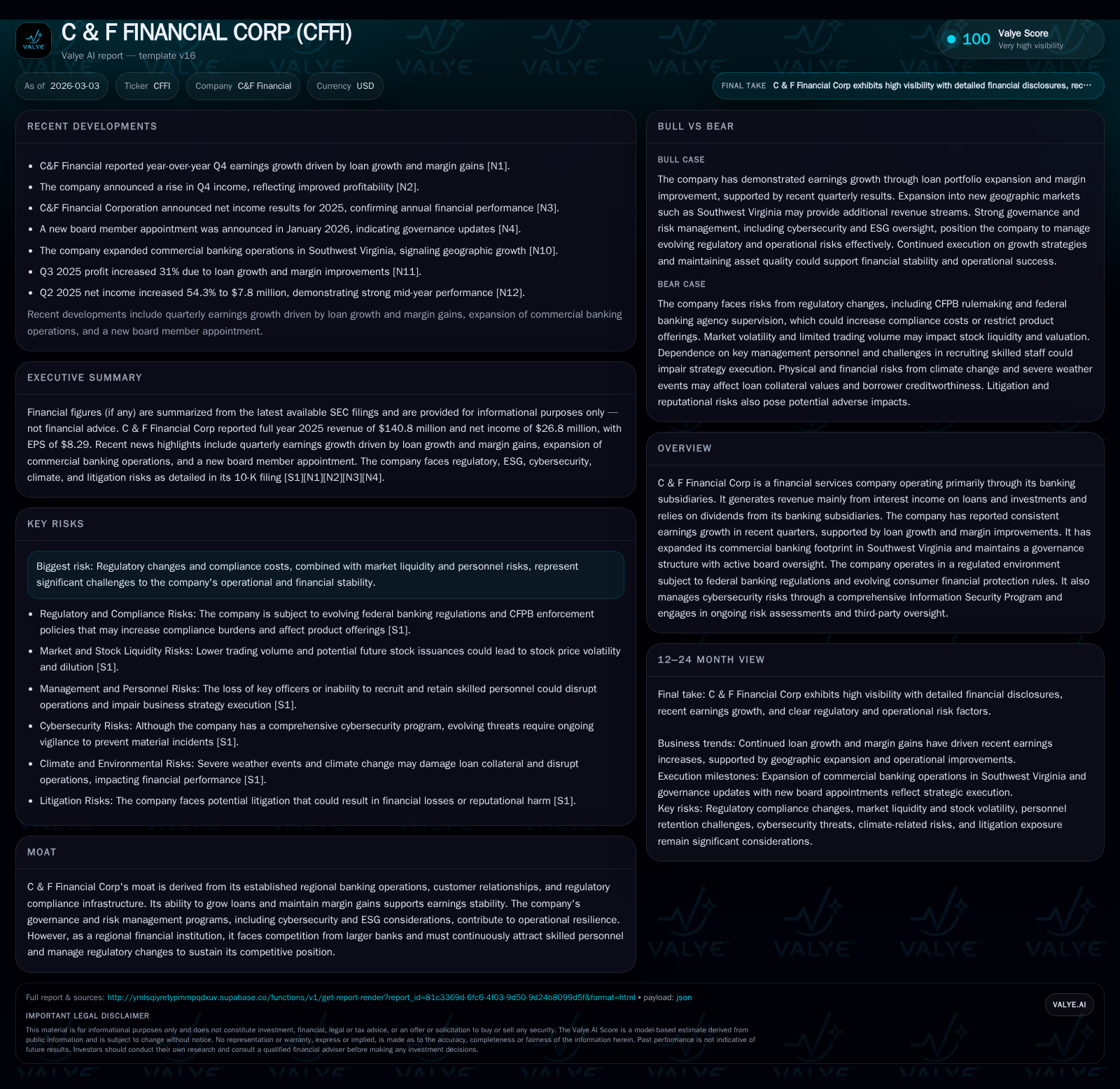

C & F Financial Corp exhibited notable financial progress in 2025, with revenue increasing by 10.6% year-over-year and net income advancing 35.3%, underpinned by strong commercial loan growth in Southwest Virginia and improved net interest margins. However, operating cash flow decreased by over a third, reflecting fluctuations in core cash generation. The evolving federal regulatory environment, including heightened ESG scrutiny and consumer finance oversight, presents ongoing challenges. Capital allocation remained disciplined, with steady dividends and significantly curtailed share repurchases. The company’s moat relies on established regional relationships and regulatory adeptness, but must navigate personnel, litigation, and climate risks carefully to sustain momentum.

Performance Trajectory: Analysis of Recent Financial Growth and Its Catalysts

C & F Financial Corp's fiscal year 2025 marked a clear inflection point in the trajectory of its earnings cycle after relatively flat revenue in FY2024. Annual revenue reached $140.8 million, representing a solid 10.6% year-over-year increase from $127.3 million in FY2024 as reported in their latest filings [F1]. This surge was fueled principally by expanding loan balances coupled with margin improvement strategies.

Net income accelerated even more markedly—rising 35.3% from $19.8 million to $26.8 million—signaling effective leverage of earned interest against operating expenses and credit costs under tight control [F1], corroborated by Q4 earnings releases highlighting these drivers [N1],[N2],[N3]. Meanwhile, operating cash flow declined by about one-third relative to the prior year ($24.5 million versus $38.5 million), illustrating volatility in working capital components or changes in deposit dynamics that influence cash conversion cycles typical for regionally focused banking firms [F1]. Capital expenditures also trended lower by approximately 33%, supporting prudent spending priorities aligned with infrastructure needs rather than aggressive expansion or digital transformation accelerations seen elsewhere.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 141 | 27 | 24 | 2 | +10.6% | +35.3% |

| 2024 | 127 | 20 | 38 | 3 | -0.0% | -16.0% |

| 2023 | 127 | 24 | 39 | 1 | +4.4% | -19.1% |

| 2022 | 122 | 29 | 91 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 1 | 22 |

| 2024 | 6 | 9 | 35 |

| 2023 | 6 | 8 | 37 |

| 2022 | 6 | 5 | 87 |

Source: SEC companyfacts cache [F1].

The figures above illuminate a pattern where earnings are benefiting from strategic lending growth combined with margin optimization yet cash flows remain sensitive to balance sheet dynamics consistent with regional banks focusing on efficient asset-liability management.

Loan Portfolio Dynamics: Growth Drivers and Margin Evolution

A central pillar of C & F Financial’s recent earnings momentum resides in its expanded commercial loan portfolio predominantly concentrated in Southwest Virginia markets—a region where it maintains entrenched customer relationships buttressed by localized knowledge and regulatory compliance frameworks favorable for sustained growth [N1], [S16]. Customer intimacy allows selective origination activity at attractive spreads despite sector-wide asset yield compression risks.

The bank's reported rise in net interest margin acts as an important propellant behind income gains amid an environment challenging for yield enhancement across many regional lenders [N1]. This suggests judicious balance sheet positioning paired with active credit quality monitoring protocols to mitigate downside risk while capturing spread widening opportunities where possible without compromising asset quality metrics.

Additionally noteworthy is C & F Financial’s reliance on dividends remitted from its banking subsidiaries constituting a vital cash flow source enabling parent-level operational funding without resorting extensively to external capital markets—typical of mid-size financial holding companies seeking internal capital efficiency within regulatory constraints imposed on subsidiary dividend distributions [S9].

This dual reliance—loan book robustness combined with regulated dividend streams—forms the core moat elements sustaining earnings stability amid fierce competition from larger regional banks expanding aggressively via technology investments.

Regulatory Environment and Compliance Complexity in 2026

The regulatory landscape confronting C & F Financial has become increasingly intricate due to political shifts changing leadership within federal banking agencies that oversee rulemaking regimes and supervisory doctrines affecting regional institutions broadly and C & F specifically [S1],[S8]. The current presidential administration's agenda marks departure from predecessors', reshaping enforcement priorities with potential interpretative shifts demanding agile compliance adaptation.

Furthermore, the company acknowledges intensifying scrutiny over environmental social governance (ESG) matters levied by stakeholders ranging from customers through regulators to investors; these initiatives introduce incremental cost burdens alongside potential reputational risk if compliance missteps occur or conflicting jurisdictional regulations emerge across diverse state frameworks [S7]. Such ESG considerations also interlace with consumer finance product oversight led increasingly by the Consumer Financial Protection Bureau (CFPB), whose evolving rulemaking could materially affect the design and offering of products critical for community bank competitiveness amidst tightening supervision regimes that extend indirectly via Federal Reserve or FDIC adoption.

These regulatory headwinds necessitate robust governance systems complemented by vigilant legal counsel engagement lest unanticipated consequences erode operational flexibility or impose costly remediation requirements.

Governance Enhancements and Board-Level Oversight Update

Reflecting responsiveness to mounting regulatory complexity is C & F Financial’s strategic reinforcement of its board composition through appointment of Dr. David H. Downs as a new director effective February 24, 2026—a move signaling intent to elevate governance quality during an era where regulators emphasize board accountability over risk management programs including cybersecurity defenses and compliance monitoring frameworks [N5],[S1],[S15].

The board’s enhanced oversight capacity underpins corporate resilience efforts ensuring rigorous review cycles for policy updates around information security standards aligned with FFIEC guidelines as well as periodic assessments of third-party service provider risk controls pivotal given today’s cyber-threat landscape—all critical factors validating operational continuity assurances valued highly within banking supervision assessments.

Such governance evolutions align with best practices prioritizing transparency alongside agility essential for navigating fluid regulatory environments effectively.

Capital Allocation Review: Dividends, Share Repurchases, and Cash Flow Trends

Financial stewardship at C & F Financial during FY2025 exhibits discipline balanced against growth needs amid external uncertainty. While dividends paid slightly increased to approximately $5.9 million maintaining shareholder income streams comparably stable against prior years ($5.75M–$6M range) [F1], share repurchases contracted sharply to under $1 million following earlier double-digit million-dollar levels consistent with retaining capital buffers responsive to regulatory prudence around subsidiary dividend restrictions potentially limiting upstream flows critical for parent liquidity management tasks [F1],[S9],[S10],[S23].

Return on equity estimated near 10.3% reflects moderate efficiency gains driven by improved net profitability relative to equity base reaching $261.8 million as of FY2025 year-end—a healthy sign aligning with sustainable bank holding company performance thresholds favored by prudent investors seeking balance between yield generation and risk calibration within community banking segments [F1].

Free cash flow remains positive at approximately $22.2 million (operating cash flow minus capex), endorsing internal funding capability supporting organic initiatives without excessive reliance on debt issuance or equity dilution notwithstanding market volatility concerns noted around common stock trading patterns affecting liquidity provisions for potential future issuances impacting shareholder value perceptions [F1],[S9],[S10].

Risk Landscape: Personnel Challenges, Litigation Exposure, and Climate Implications

On the operational risk front,[S6] highlights escalating compensation pressures reflective of competitive landscape dynamics for talented executives crucial for client acquisition strategies leveraging local ties alongside product innovation capacities—factors that could edge upward expense ratios if not managed prudently.

Legal proceedings exist as inherent banking industry features introducing contingent liabilities subject to insurance coverage limits potentially exposing net income fluctuations if adverse judgments exceed protections or impair reputational standing adversely affecting business development prospects [S5],[S14].

Climate-related risks also receive explicit acknowledgment encompassing prevalent physical threats like hurricanes or flooding within their geographic footprint which pose collateral value diminution risks translating directly into credit quality degradation possibilities mandating stress-testing incorporation into underwriting frameworks ensuring readiness for episodic environmental shocks increasingly materializing under shifting weather patterns emblematic of broader climate change effects impacting real estate-dependent portfolios critically important in retail/commercial mortgage sectors served by the bank [S5],[S12].

Cybersecurity diligence conducted through comprehensive programs led by seasoned professionals adherent to FFIEC benchmarks reduce exposure likelihood though residual operational risks persist requiring continued investment attention given growing attack sophistication trends documented nationally among smaller institutions lacking scale economies of technology deployment validations featured prominently across federal examination guidebooks emphasizing continual audit committee engagement suited for this purpose supporting enterprise-wide defense postures robustly maintained presently without any material incident reported historically demonstrating management effectiveness thus far.[S15]

Outlook and Monitoring: What to Watch as Regional Banking Evolves

Looking forward involves close observation of several pivotal vectors shaping future performance trajectories at C & F Financial including congressional legislative developments influencing CFPB mandates possibly reshaping consumer product offerings critical to diversifying retail revenues away from primary commercial loan concentrations currently safeguarding income stream durability.[N1],[N3],[S1]

Margin sustainability amid potential shifts in interest rate regimes constitutes another focus area particularly as macroeconomic oscillations affect deposit pricing strategies alongside pressure points intrinsic to asset yield compression realities prevalent nationwide among mid-tier banks competing on both price and service differentiation parameters.[N2]

Continued retention success for skilled workforce segments essential given noted scarcity fuelled compensation escalation forecasts affecting cost management capabilities also remains key.[S6]

Board-level communication hints at maintaining conservative dividend policies balanced against capital adequacy signaling no radical payout expansions planned short term providing comfortable buffers assuming no disruptive external shocks.[N3],[S23]

Lastly evolving ESG norms will impose strategic priority adjustments requiring ongoing adaptation balancing stakeholder demands versus operational pragmatism preserving franchise value within community sensitive contexts characteristic of their regional moats ultimately determining competitive positioning vis-à-vis larger players exploiting scale advantages but often lacking comparable local embeddedness.[S7]

This analysis leverages publicly available financial data and company disclosures without offering investment advice or price predictions. Readers should consider company filings directly alongside broader industry developments before formulating views related to C & F Financial Corporation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments