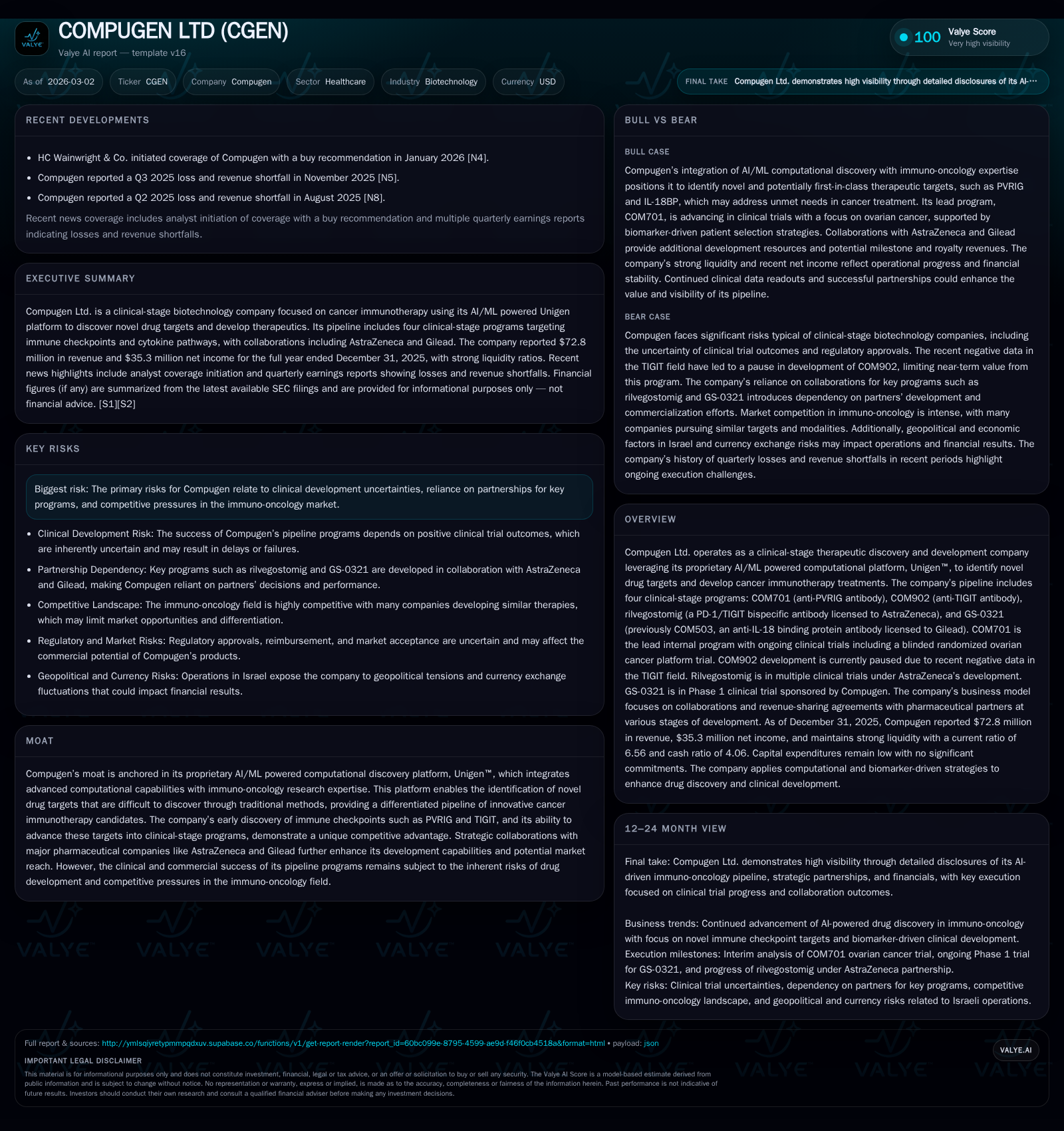

Compugen Ltd. Accelerates Growth Through AI-Driven Cancer Immunotherapy Innovations

A clinical-stage biotech company advances its AI-powered drug discovery platform fueling a dramatic financial turnaround and pipeline progress.

Compugen Ltd. delivered a remarkable financial recovery in FY2025, posting over 160% revenue growth coupled with operating profitability for the first time in several years. This turnaround was propelled by milestone licensing revenues from its proprietary immuno-oncology programs discovered via its AI/ML computational platform, Unigen™. Clinically, the lead internal asset COM701 advances through a blinded randomized ovarian cancer trial, while collaborations with AstraZeneca and Gilead underpin risk-sharing and validation of pipeline assets. Despite worsening operating cash flow compared to the prior year, Compugen maintains strong liquidity and is reinvesting capital internally without dividends or buybacks. Near-term catalysts include the expected interim analysis of COM701’s maintenance ovarian cancer study in early 2027.

Historic Financial Transformation Fueled by AI-Enhanced Pipeline Development

Compugen Ltd.’s financial trajectory through fiscal years 2022 to 2025 illustrates a striking operational pivot. After sustained periods of losses—net income was negative $33.7 million in 2022 before improving slightly but remaining negative in subsequent years—the company achieved net profitability of $35.3 million in 2025 [F1]. This dramatic shift accompanies a soaring revenue base which expanded from just $7.5 million in 2022 to $72.8 million in 2025, a staggering compound acceleration mainly attributed to licensing milestone revenues tied to the advancement of their oncology immunotherapy programs [F1][S1].

Operating income likewise flipped from a deficit of -$35.4 million in 2022 to a positive $31.3 million last year, underscoring improved cost management alongside maturation of intangible assets through monetization deals [F1]. In terms of operational cash flow, while CFO declined by approximately one-third compared to the year prior—from $49.6 million down to $31.6 million—it remains strong enough to fund near-zero capital expenditures ($0.3 million reported) while maintaining a robust liquidity position approaching $90.6 million in cash and equivalents at year end [F1]. The current ratio stands around an enviable 6.56x attesting to solvency strength [F1]. Equity grew significantly doubling from about $54.9 million in 2024 to over $102.7 million last year [F1], yielding an estimated return on equity near 34%.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 73 | 35 | 32 | 31 | +161.1% | +348.4% |

| 2024 | 28 | -14 | 50 | -15 | -16.7% | +24.1% |

| 2023 | 33 | -19 | -36 | -13 | +346.1% | +44.3% |

| 2022 | 8 | -34 | -35 | -35 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 31 | 34.4 |

| 2024 | 49 | -25.9 |

| 2023 | -36 | -28.6 |

| 2022 | -35 | -43.4 |

Source: SEC companyfacts cache [F1].

Table uses audited annual figures per fiscal year ending December.

Leveraging Unigen™: The Core Competitive Advantage in Cancer Immunotherapy Target Discovery

At the technical heart of Compugen’s transformation is Unigen™, an AI/ML powered computational platform combining machine learning with robust immuno-oncology datasets to identify novel immune checkpoints that have eluded more conventional drug discovery approaches [S1]. This platform propelled the early identification of candidates such as PVRIG and TIGIT — inhibitory receptors implicated in tumor immune evasion — enabling Compugen to pursue next-generation checkpoint blockade modalities including monoclonal and bispecific antibodies.

This biologics-driven modality aligns with broader industry trends emphasizing immune checkpoint blockade therapies augmented via multispecific formats such as bispecific antibodies shown by rilvegostomig’s design incorporating PD-1 and TIGIT binding domains [S1]. Unigen™’s capability to integrate complex genomic, proteomic, and cell signaling data confers a strong scientific moat that differentiates Compugen’s pipeline from numerous biotech peers struggling with target validation bottlenecks.

Clinical Progress and Pipeline Dynamics: COM701 Leads While COM902 Pauses

Compugen’s clinical-stage portfolio centers around four drugs progressing through varying stages:

COM701: A potential first-in-class anti-PVRIG monoclonal antibody being evaluated primarily as maintenance therapy in relapsed platinum-sensitive ovarian cancer via the ongoing MAIA-ovarian blinded randomized platform trial sponsored solely by Compugen [S1][N2]. This trial’s interim readout is slated for Q1 2027 — a pivotal near-term catalyst poised to validate both target utility and clinical efficacy.

COM902: An anti-TIGIT antibody candidate once considered best-in-class has had its development paused following unfavorable data emerging across the TIGIT therapeutic class — reaffirming inherent risks associated with emerging checkpoint targets [S1].

Rilvegostomig: A bispecific PD-1/TIGIT antibody derived from COM902 licensed exclusively to AstraZeneca underpins multiple Phase I/II/III trials conducted by AstraZeneca globally, extending Compugen's reach into late-stage trials funded externally [S1].

GS-0321 (formerly COM503): A high-affinity anti-IL-18 binding protein antibody licensed to Gilead Sciences; Compugen currently sponsors an early Phase 1 clinical trial assessing safety and preliminary efficacy parameters [S1].

Further early discovery research continues internally targeting additional immune mechanisms potentially augmenting antitumor responses.

Evolving Collaborations with AstraZeneca and Gilead Strengthen Development Prospects

The strategic licensing agreements underpinning rilvegostomig with AstraZeneca and GS-0321 with Gilead highlight key pillars of risk sharing and resource leverage crucial for an emerging biopharma like Compugen [S17][S23]. These alliances provide validation for Unigen™-derived targets reaching mid-to-late stage development allowing partners’ extensive global trial infrastructure and commercialization channels to be utilized.

Notably, Compugen amended its agreement with AstraZeneca in late 2025 selling part of its royalty stream for an upfront payment of $65 million—a material liquidity event reflecting confidence in rilvegostomig’s commercial potential against peak sales targets exceeding several billion dollars per analyst consensus within the sector [S23][F1]. Gilead's license includes upfront payments exceeding $50 million plus milestones tied closely to successful regulatory steps supporting GS-0321 progression.

Yet these collaborations entail dependencies on partner execution and regulatory strategies impacting asset timelines — introducing external risk on both clinical progression and revenue streams.

Capital Efficiency and Shareholder Returns amid Operating Cash Flow Headwinds

Despite stronger earnings metrics, operating cash flow fell roughly one-third from $49.6 million in FY2024 to $31.6 million in FY2025 largely due to timing differences between recognition of licensing payments versus cash receipts or expenditures linked to trial conduct phases [F1]. Capital expenditure remained deliberately minimal at approximately $0.3 million consistent with reliance on partners for late-stage development costs [F1][S11]. The company's sizable cash reserves ($90+ million) provide a substantial runway supporting continued R&D effort without immediate need for external financing [F1][S7].

Return on equity metrics approximate a healthy ~34% given net income growth versus shareholder equity buildup over recent years suggesting efficient capital deployment within clinical development operational constraints [F1]. Notably absent are any dividend distributions or share repurchase programs as stated consistently since listing; Compugen retains profits within business activities prioritizing pipeline capitalization over shareholder returns via yield strategies [S16][S24].

Risks in Drug Development and Geopolitical Factors Impacting Future Trajectory

Several risk domains weigh on Compugen’s outlook:

Clinical uncertainty: Negative data prompting pause on COM902 underscores the high attrition common in immune checkpoint therapies especially within contentious targets such as TIGIT where competitive landscape pressure is intense [S4][S19]. Regulatory hurdles remain ever-present risks influencing faster or slower timeline achievement.

Partnership dependency: Licensing relies heavily on AstraZeneca's and Gilead’s continued commitment; any shifts could affect milestone-triggered revenues or asset stewardship adversely impacting financials.

Geopolitical environment: Being Israel-based exposes Compugen to political volatility impacting both operational continuity and investor sentiment given ongoing regional instability compounded by global macroeconomic fluctuations may affect cost structures or access to international capital markets [S25][S4].

Exchange rate exposure: Significant expenses paid in NIS versus revenues realized predominantly in USD widen currency translation risk impacting reported results notably under volatile forex conditions [S7].

Furthermore, intensifying competition amid evolving biologics modalities elevates pressure on pipeline differentiation requiring ongoing innovation investment just to maintain relevance as platforms evolve rapidly sector-wide [S5].

Key Upcoming Catalysts: Clinical Data Readouts and Partnership Milestones to Watch

Attention should center on:

The interim efficacy analysis from the Phase II MAIA ovarian cancer maintenance trial for COM701 anticipated Q1 2027 — success here could catalyze valuation reassessment grounded on first-in-class checkpoint validation outside PD-1/PD-L1 inhibitors known today.

Milestone announcements from AstraZeneca concerning rilvegostomig regulatory progress encompassing BLA submissions or Phase III completions which drive tiered payouts per licensing contracts [S23].

Next phase transitions by Gilead surrounding GS-0321 beyond Phase I endpoints informing product candidate viability.

While no definitive guidance beyond these milestones is provided explicitly by management so far, monitoring shifts along these vectors will be paramount for assessing value creation trajectories or financing needs should operational costs accelerate unexpectedly amidst broader market volatility [N2][S1].

This analysis aims solely at summarizing recent company developments anchored exclusively on reported data without offering investment guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments