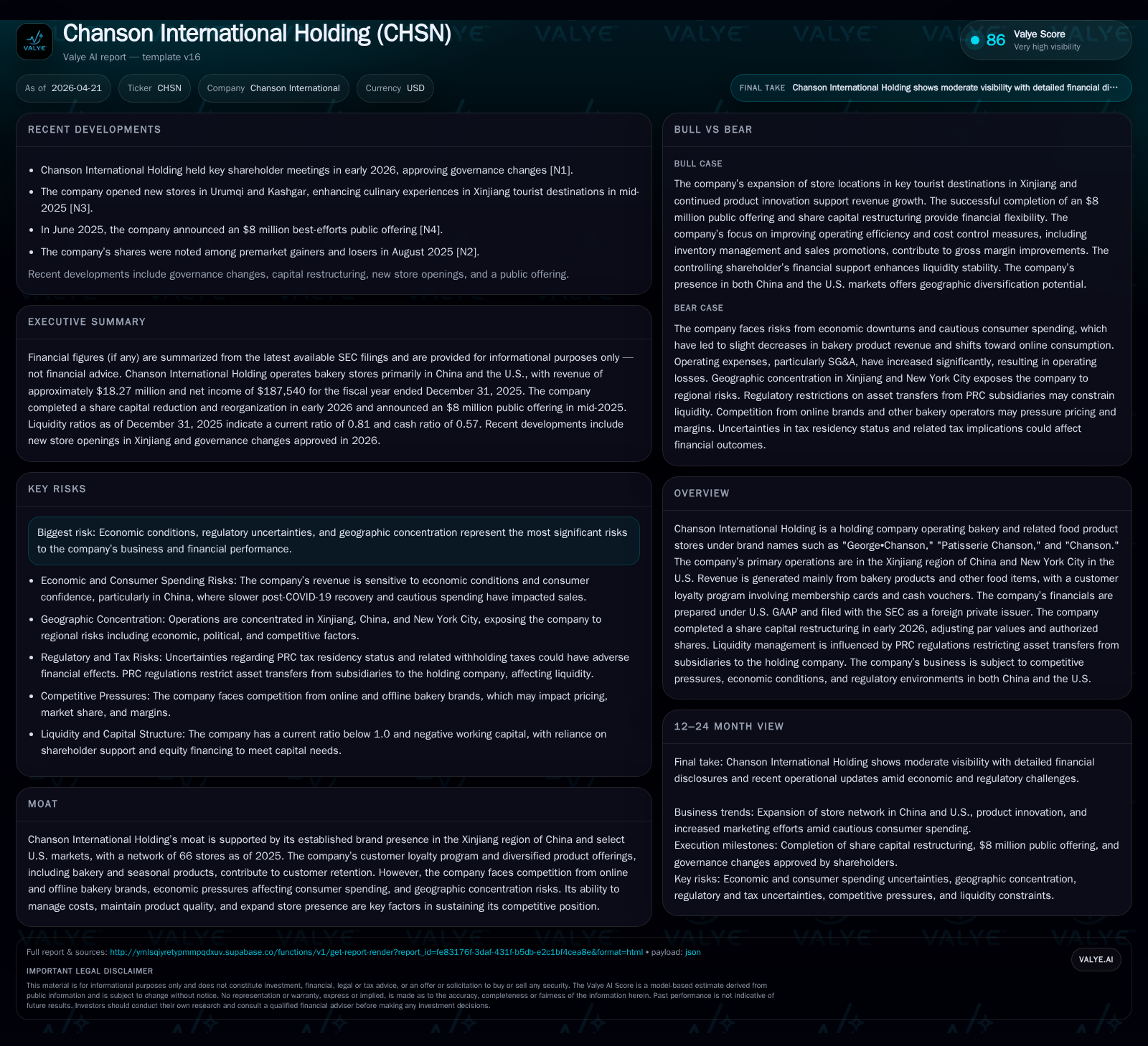

Chanson International’s Share Capital Reset and Growth Challenges in Bakery Markets

Chanson International recently completed a significant share capital restructuring amid slowing comparable store sales and competitive pressures in its bakery business.

In early 2026, Chanson International Holding executed a comprehensive share capital reduction and subdivision that reduced the par value of shares from $0.08 to $0.0001, increasing authorized shares but enhancing balance sheet flexibility. Despite expanding its store base to 66 locations by year-end 2025, the company faced notable declines in comparable store sales—down 17.2% in China and 29% in the U.S.—driven by sluggish consumer spending and intensified competition from online and offline bakery brands. Regulatory constraints on capital flows between China and the U.S., along with ongoing inflationary pressures, impose additional headwinds. Looking forward, store expansions and cost controls will be key execution areas, while financials indicate continued pressure on operating margins despite modest revenue growth.

Recent Quarterly Operating Update: Share Capital Reorganization and Implications

Chanson International Holding announced a significant capital restructuring finalized by March 13, 2026 as recorded in its Form 6-K filings dated February 26 [S3] and March 16 [S2], 2026. The company reduced the par value of each issued and outstanding Class A and Class B ordinary share from US$0.08 to US$0.0001 by canceling US$0.0799 of paid-up capital per share. This reduction was immediately followed by a subdivision multiplying each authorized but unissued share into 800 shares at the new par value, culminating in authorization for approximately 4.11 billion Class A shares and 15 million Class B shares with maintained voting rights.

This restructuring aims to provide enhanced balance sheet flexibility by converting previously rigid equity into distributable reserves that may absorb accumulated losses or support future corporate actions permitted under Cayman Islands law [S2]. While the nominal value reduction does not directly affect cash position, it supports better financial presentation of equity on the balance sheet and sets a platform for potential capital re-deployment or shareholder returns aligned with improving operational performance.

Business Model Overview: Brand Portfolio, Revenue Streams, and Loyalty Programs

Chanson International operates primarily through three bakery brand names: "George•Chanson," "Patisserie Chanson," and "Chanson." Its brick-and-mortar footprint comprises predominantly retail bakery stores located primarily in the Xinjiang region of China (63 stores) alongside three stores situated in New York City as of December 31, 2025 [S1]. Revenue is mainly generated from retail sales of bakery products supplemented by seasonal offerings such as beverages and desserts.

A critical feature supporting customer retention is their loyalty program involving membership cards and cash vouchers which incentivizes repeat purchases [N1]. This program functions as a retention mechanism amidst intensifying competition both from traditional local bakeries and rapidly growing online bakery brands increasingly favored by consumers. The diversified product mix facilitates revenue stability by balancing staple baked goods with seasonal novelties aimed at attracting varied customer segments.

Competitive Landscape and Industry Context: Market Segmentation and Consumer Trends

The company's core markets face considerable competitive pressures amid structural shifts in consumer behavior—particularly within China where online purchasing channels have significantly expanded consumer options [S1]. Inflationary dynamics alongside slower-than-anticipated post-pandemic economic recovery have suppressed discretionary spending impacting foot traffic at physical locations.

Moreover, legacy brick-and-mortar bakeries compete against digitally native competitors offering rapid home delivery services with often aggressive pricing tactics that erode traditional margin pools [S1]. Geographic concentration risks are pronounced given the heavy reliance on Xinjiang for PRC revenue generation, exposing the company to regional economic fluctuations and political complexities unique to that area.

Growth Drivers and Limitations: Store Expansion, Comparable Sales, and Economic Factors

Despite facing headwinds on revenue growth at existing locations reflected by comparable store sales declines—17.2% in PRC stores and an even steeper 29% drop at U.S. stores during fiscal year ended December 31, 2025—the company continued to expand its overall store count reaching a total of 66 stores [S1]. This expansion strategy underpins top-line growth potential but also introduces risk related to cannibalization or oversaturation within relatively localized markets.

The suspended bakery operations at the Chanson 23rd Street location contributed materially to U.S. comps weakness [S1]. Slower consumer confidence recovery coupled with intensified discounting strategies has pressured revenue mix quality despite promotional efforts designed to stimulate traffic.

Regulatory and Geopolitical Risks Impacting Capital Flows and Operations

Regulatory complexity significantly influences Chanson’s liquidity management due to Chinese government restrictions on transferring assets from subsidiaries within PRC jurisdictions back to the holding entity—headquartered in the Cayman Islands [S1]. This restricts reinvestment flexibility particularly under volatile foreign exchange regimes given RMB-to-USD conversion challenges highlighted by limited hedging options [S15].

Geopolitical uncertainties between operational regions—namely Xinjiang’s politically sensitive environment juxtaposed with U.S.-based operations—compound compliance burdens while elevating operational risk profiles requiring vigilant governance oversight [N1][S1]. These factors frame capital allocation decisions following the recent share reorganization emphasizing internal resource optimization over external funding reliance.

Key Execution Metrics to Monitor: Guidance, Store Performance, and Margin Levers

Critical performance indicators moving forward include:

- Recovery trajectory for comparable store sales post-2025 reflecting efficacy of marketing campaigns and product innovation.

- Success of promotions balancing traffic stimulation against margin erosion particularly within seasonal products which have shown declining gross margins due to discounts [S12].

- Cost containment effectiveness especially labor optimization, ingredient sourcing efficiencies amidst inflationary pressures noted more acutely in U.S. operations [S6][S20].

- Planned addition of approximately ten new stores during fiscal year 2026 with associated capex deployment targeting deepening penetration within core markets [S11].

- Handling regulatory compliance challenges influencing liquidity flows affecting working capital availability crucial for inventory management.

Financial Review: Revenue Growth, Margin Pressure, Cash Flow, and Capital Structure

Financial results through fiscal year ended December 31, 2025 illustrate operational strains across multiple dimensions:

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($mm) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 18 | 187540 | 3 | -1887125 | +0.2% | -75.2% |

| 2024 | 18 | 756285 | 4 | -529620 | +5.7% | +2151.7% |

| 2023 | 17 | 33588 | -3 | -610501 | +30.0% | +102.6% |

| 2022 | 13 | -1288205 | 1 | -1438025 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 0.3 |

| 2024 | 3 | 4.1 |

| 2023 | -4 | 0.3 |

| 2022 | 0 | -109.4 |

Source: SEC companyfacts cache [F1].

Revenue remained flat year-over-year reflecting levelling sales achieved via new stores offsetting declining comps [F1][S1]. Operating losses widened severely driven mostly by higher SG&A expenses associated with expansion investments plus rising ingredient costs partially offset by efficiency gains [F1][S8]. Net income declined substantially though marginally positive due largely to income tax effects.

Operating cash flow remains positive but has contracted compared to prior year reflecting increased working capital needs tied to expanded inventory requirements amid slower revenue turnover [F1]. Capex surged sharply echoing investments tied mainly to new unit openings planned for continued growth initiatives [F1][S11].

The March 2026 share capital reorganization enhanced equity robustness inflating reported equity from $18 million end-2024 to $56 million by end-2025 through transferred reserves despite ongoing operating losses underscoring balance sheet strength post-restructure [F1][S2].

Analysis based on current disclosures shows Chanson International navigating material near-term headwinds rooted in weakening comparable store sales amidst a transitioning competitive bakery market landscape compounded by complex cross-border operational constraints. Their brand loyalty programs coupled with ongoing geographic expansion articulate a deliberate yet cautious growth stance contingent upon execution discipline regarding cost controls and market positioning for recovery ahead.

Disclaimer: This report is an independent analyst commentary based solely on publicly available information as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments