Reading International’s Asset-Backed Model Confronts Persistent Industry Headwinds

Recent quarterly resilience in cinema and real estate segments contrasts with mounting liquidity pressures, underscoring risks to Reading International’s integrated business approach.

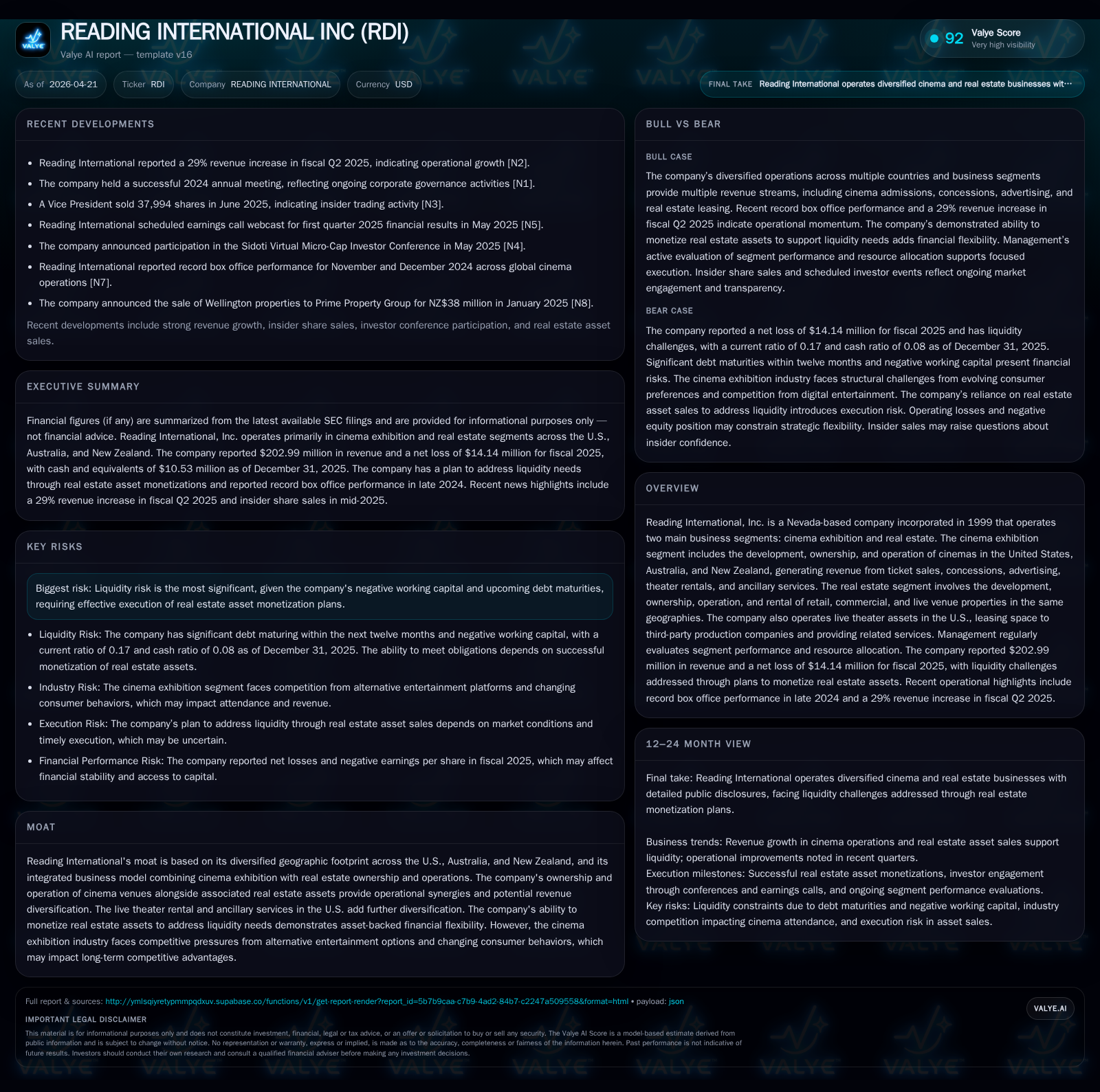

Reading International posted higher revenues and operating income at the asset group level through the first nine months of 2025 without recording impairments, indicating operational resilience amid challenging industry conditions. However, significant liquidity constraints persist due to burdensome near-term debt maturities and negative working capital, compelling management to rely on real estate asset monetization and refinancing as critical lifelines. The company's dual focus on cinema exhibition across three countries and associated real estate assets provides diversification, but secular headwinds from streaming and consumer shifts weigh on growth prospects. Watching progress on asset sales and refinancing will be key to assessing Reading's ability to sustain its recovery and manage financial risks going forward.

Latest Operating Update Highlights: Improved Performance Meets Liquidity Concerns

The latest quarterly report filed November 14, 2025 ([S2]) anchors Reading International's near-term operating narrative with signs of operational improvement at the asset group level. The company reported increased revenues and operating income for the first nine months of 2025 relative to the same period in 2024. Notably, management determined no impairment charges were needed for these periods despite ongoing uncertainties in cinema attendance trends. This operational uptick suggests underlying asset groups are generating stronger cash flows than in prior years.

However, this positive operating momentum contrasts sharply against continuing liquidity constraints. As of September 30, 2025, Reading faced negative working capital estimated at $92.7 million ([S21]), with $16.5 million in debt due within twelve months ([S6]). Cash on hand stood at approximately $10.5 million ([F1]), insufficient to cover short-term liabilities without additional funding sources. To address this tight liquidity position, Reading’s management is pursuing a strategy centered on monetizing select real estate assets—the company emphasizes confidence in its portfolio's marketability supported by prior sales totaling $201.5 million since 2021 ([S10], [S24]). These factors underscore a delicate balance: operational resilience suffused with considerable financial vulnerability.

Continuous evaluation of the ASC 205-40 going concern assertion remains fundamental, driving management’s focus on refinancings and asset sales as primary mitigants against potential solvency doubts.

Business Model and Segment Overview: Integrated Cinema Exhibition and Real Estate

Reading International operates through two principal segments: cinema exhibition and real estate development/ownership ([S1], [S2]). The cinema exhibition footprint spans the United States, Australia, and New Zealand, generating revenue principally from ticket sales, concessions, advertising placements within theaters, theater rentals for third parties, and various ancillary services such as live theater operations in the U.S. These cinemas operate both as consumer-facing entertainment venues and tenants within properties owned or controlled by the company's real estate segment.

The real estate division manages a portfolio comprising retail locations, commercial offices, and live entertainment venues—with activities ranging from direct operation to leasing space to third-party tenants including production companies in live theater contexts ([S18]). This complementary structure creates operational synergies; for example, owning venue properties facilitates capturing rental income while supporting cinema operations that drive foot traffic and concessions revenue.

Geographically diversified across three mature markets—each with distinct entertainment consumption patterns—this multidimensional business model aims to soften sector-specific shocks. Nonetheless, the core economics of the cinema exhibition remain challenged by industry maturity effects exacerbated by digital substitutes affecting attendance patterns.

Competitive Environment: Market Pressures and Diversification Advantages

The competitive landscape for Reading’s cinema segment is marked by increasing competition from digital streaming services that disintermediate traditional moviegoing experiences ([S1]). Such substitution erodes box office attendance volumes limiting pricing power even amid rising input costs (e.g., film rental fees). Consumer switching costs remain low; patrons can relatively easily transition between streaming platforms or alternate leisure activities.

In this context, Reading’s integrated ownership of real estate assets generates important offsets to pure exhibition risks. Rental income streams from retail or live venue tenants provide revenue diversification less directly impacted by content consumption trends. Furthermore, tenant relationships tend to offer more contractual stability than episodic cinematic attendance patterns.

Nonetheless, even ancillary services such as live theater leasing face demand cyclicality tied to discretionary spending propensities among audiences—a factor that does not fully insulate operations from economic downturns or shifts in consumer preferences.

Regional segmentation nuances also provide varying degrees of insulation; for example, Australian or New Zealand markets display different competitive dynamics relative to large U.S. urban centers ([N1]). This geographic breadth represents a moat component but is not wholly immune to broader entertainment ecosystem disruptions.

Growth Drivers: Geographic Reach, Ancillary Services, and Real Estate Monetization

Operational improvements indicated in recent quarterly disclosures ([S2]) highlight potential leverage points for margin expansion—particularly via growing concession sales mixes combined with targeted advertising initiatives inside theaters. These ancillary offerings contribute disproportionately higher margin contributions compared to ticketing alone.

Real estate monetization stands out as a pivotal growth enabler—not through accelerating property sales in volume but rather strategic disposals designed to inject liquidity critical for funding expansions or managing existing debt profiles ([S4], [S10]). Given historical success selling nine properties for over $201 million since 2021 without disrupting core operations ([S24]), management possesses demonstrated capability in selectively unlocking asset value while sustaining theater network integrity.

Live theater ancillary services provide niche opportunity capture although represent a limited piece relative to overall scale.

Finally, evolving film release calendars post-pandemic may help boost attendance if marquee titles draw patrons back consistently—yet this remains subject to unpredictability around consumer tastes.

Constraints on Growth: Industry Shifts, Consumer Trends, and Financial Risks

Despite isolated operational gains, Reading faces structural headwinds deeply embedded in industry secular trends ([S1], [F1]). Streaming platforms enjoy robust adoption growth that reshapes content delivery paradigms fundamentally disadvantaging traditional exhibitors. Pricing power is constrained as consumers substitute readily among entertainment formats.

Fixed cost burdens in theater operations—ranging from lease obligations (even when self-owned) to ongoing maintenance requirements—limit margin scalability especially when attendance plateaus or declines episodically.

Financially, the company grapples with significant current liabilities overshadowing all forms of liquid assets as evident by a current ratio below 0.2 ([F1]). Negative working capital fundamentally restricts operational flexibility curtailing discretionary investments critical for competitive positioning.

Ongoing reliance on refinancing maneuvers heightens execution risk should capital markets conditions deteriorate or asset sales fail to materialize timely at favorable valuations ([S21]). Economic cycles influencing leisure spending add further unpredictability.

These constraints collectively temper growth visibility signaling that any sustained resurgence depends heavily on managing both macro-entertainment trends alongside micro financial/operational execution risks tightly.

Upcoming Catalysts and Execution Milestones to Watch

Critical near-term events revolve around refinancing scheduled debt maturities extending terms into late 2026—specifically loans extended per November 2025 filings including bank facility extensions ([S21], [S10]). Progress here reduces default risk alleviating immediate liquidity stress.

Further real estate asset monetizations approved by management hold key potential impact; timing and value realization metrics will be crucial markers indicating ability to fund upcoming obligations without additional distress issuance or dilution.

Subsequent quarterly earnings releases will reveal whether top-line improvements translate into sustainable net income trajectories devoid of impairments per ASC 360 tests.

Monitoring any strategic efforts pivoting towards digital integration or expansion into adjacent entertainment verticals also bears attention given industry disruption pressure points identified.

Shareholder communications such as annual meeting outcomes in early April 2026 affirm ongoing corporate governance stability but do not yet indicate major business model shifts ([N1]).

Financial Profile Summary: Revenue Trends, Profitability, and Balance Sheet Stress

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 203 | -14 | -2 | -5 | -3.6% | +59.9% |

| 2024 | 211 | -35 | -4 | -14 | -5.5% | -15.1% |

| 2023 | 223 | -31 | -10 | -12 | +9.7% | +15.2% |

| 2022 | 203 | -36 | -26 | -28 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | 77.5 |

| 2024 | -9 | 808.9 |

| 2023 | -14 | -92.7 |

| 2022 | -36 | -57.6 |

Source: SEC companyfacts cache [F1]. (USD millions except FY) [F1]

Revenue declined modestly by 3.6% year-over-year into FY25 reflecting mixed demand recovery dynamics post-pandemic compounded by competition effects. Operating losses narrowed substantially (62%) evidencing better cost control or revenue mix shifts; yet losses remain material with net income still negative at $14 million reflective of interest load and depreciation impacts.

Cash balances hover around $10-12 million while current liabilities clustered above $120 million generate acute liquidity pressure indicated by very low current ratios (~0.17). Negative equity deepened significantly owing primarily to accumulated losses eroding shareholder base—a red flag for solvency absent effective capital interventions.

Operating cash flow remained slightly negative (~$1.6 million), though improved markedly versus prior years suggesting incremental stabilization but continued capex spending ($1.3 million) limits free cash flow generation capacity—imposing reliance on external financing sources or asset sales.

In sum, financial profile underscores persistent stress despite incremental operational progress requiring close attention on refinancing success and monetization strategies execution going forward.

This analysis is based exclusively on publicly filed SEC documents including Reading International’s latest Form 10-Q (November 14, 2025), Form 8-K event updates (March 31, 2026), amended annual Form 10-K/A (April 20, 2026), supplemented by periodic news disclosures [N1]. No forward-looking statements are made beyond information explicitly presented in these filings or publicly available facts about the industry environment noted herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments