Danaher Corporation Elevates 2026 Outlook on Biotechnology and Life Sciences Momentum

Strong early 2026 core sales growth in biotechnology and life sciences segments drive Danaher's raised earnings guidance amid mixed diagnostics demand.

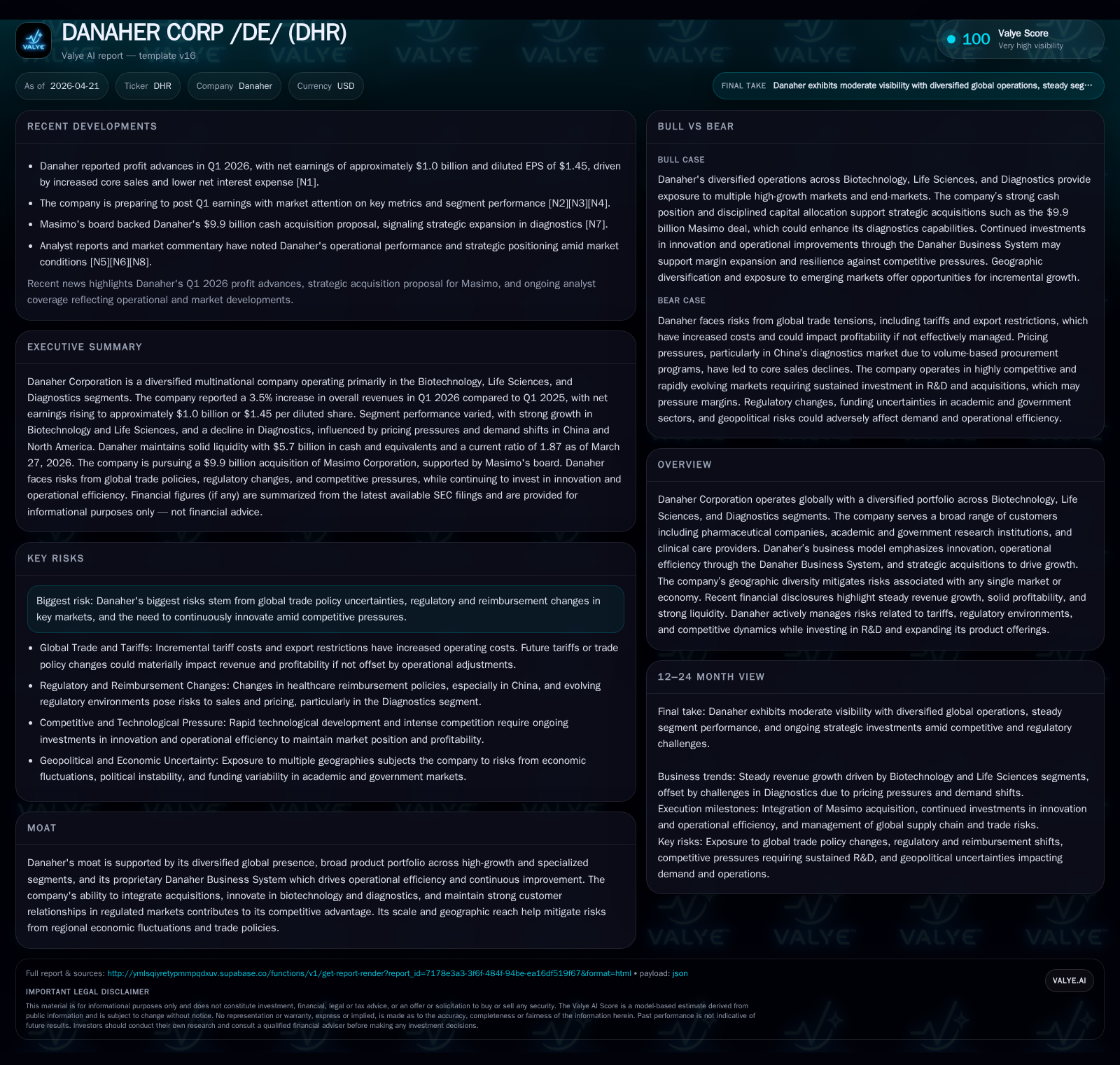

Danaher's Q1 2026 results showcase modest overall core sales growth of 0.5%, led by gains in Biotechnology and Life Sciences segments, offset by softness in Diagnostics. Foreign currency tailwinds notably boosted reported revenue by 3%. The company increased its full-year adjusted earnings guidance, reflecting confidence in innovation-led growth and operational efficiencies despite ongoing trade and regulatory challenges. Danaher's diversified portfolio across high-growth life sciences markets, combined with its proprietary operational system and strategic acquisitions, underpin its resilient competitive position. Near-term risks include tariff uncertainties and fluctuating end-market demand, particularly in diagnostics.

Q1 2026 Operating Update: Growth Drivers and Raised Guidance

Danaher's first quarter of 2026 revealed a nuanced growth landscape anchored by strong momentum within its Biotechnology and Life Sciences segments. The company's overall core sales — which exclude the effects of acquisitions, divestitures, and currency fluctuations — rose modestly by 0.5% year-over-year [S2]. This slight uptick masks divergent performance across segments: Biotechnology's core sales surged due to heightened demand for biotherapeutic development tools and consumables, while Life Sciences saw gains driven primarily by consumables related to plasmids products. However, these positive drivers were offset partially by softness in the Diagnostics segment, which experienced declining core demand amid changing reimbursement dynamics and decreased respiratory testing volumes.

Reported revenue growth was more pronounced at +3.5%, largely fueled by a favorable foreign currency translation impact (+3%) tied to U.S. dollar weakness against major currencies like the euro [S2], [S21]. Notably, pricing changes did not materially influence sales during this quarter; price effects were neutral within core sales measures, indicating stable pricing power but limited ability or willingness to hike prices amid cautious end-market conditions.

Operating profit margins improved by approximately 40 basis points year-over-year in Q1 2026 [S9], supported by higher core sales volumes, the company's operational leverage via the Danaher Business System (DBS), as well as currency benefits net of product mix shifts. Despite increased transaction costs relating to the pending Masimo acquisition within Diagnostics (~25 basis points margin drag) [S9], management's outlook remained confident enough to raise full-year adjusted earnings guidance post-quarter [N2]. This elevation reflects expectations that incremental R&D investments combined with productivity initiatives will sustain margin expansion despite macroeconomic pressures.

Danaher’s Business Model: Innovation, Acquisition, and Operational Excellence

Danaher's diversified portfolio spans three key segments: Biotechnology, Life Sciences, and Diagnostics [S1]. The company generates revenues mainly through innovative instruments, consumables, software solutions, and associated services tailored for pharmaceutical companies advancing biologics development, academic/government research laboratories probing disease mechanisms, and clinical entities relying on precise diagnostic tools.

Innovation is a cornerstone of Danaher's offering strategy. The firm consistently invests in R&D (approximately mid-single digits percentage of sales annually [S20]) to advance proprietary product platforms that characterize differentiated technology positioning—such as monoclonal antibody manufacturing aids in Biotechnology or gene editing consumables in Life Sciences. This innovation focus enables premium pricing where defensible.

Complementing organic innovation is Danaher's disciplined acquisition strategy aimed at broadening technology scope or accessing growth niches—illustrated recently by its pending Masimo acquisition intended to enhance diagnostics capabilities [S3]. The Danaher Business System underpins operations as a proprietary lean management methodology driving continuous improvement in cost efficiencies, quality control, cycle-time reduction, and scaling effects across global manufacturing footprints . This operational DNA facilitates effective integration of acquisitions for rapid synergy capture.

Customer relationships are diversified across geographies (59% ex-U.S. sales) with multi-channel distribution models catering to large pharma conglomerates investing heavily in biologic therapies alongside smaller academic research centers with variable funding cycles [S1], . Such breadth reduces dependency on any one customer or market sector.

Competitive Positioning within Biotechnology, Life Sciences, and Diagnostics

Within highly specialized markets characterized by increasing consolidation among suppliers and customers alike, Danaher's scale confers multiple competitive advantages. Its global reach spans developed (Europe/North America) and high-growth emerging markets (notably China) which represented about 27% of total sales in Q1 2026 [S12], allowing risk mitigation from regional headwinds such as regulatory stringency or reimbursement policy shifts.

Competitive moats arise not only from technology leadership but also from robust regulatory compliance expertise essential for medical devices and diagnostic products navigating global approvals. While pricing power is moderated by intense competition—especially in diagnostics where commoditization poses pressure—Danaher's persistent emphasis on R&D investment sustains product differentiation enabling above-average margins relative to peers .

Industry consolidation trends favor established players capable of rolling up smaller innovators or securing exclusive partnerships with major pharmaceutical clients for critical supply components. Danaher's demonstrated ability to integrate acquisitions efficiently supports this advantage.

Industry Dynamics: Trade, Regulation, and Technology Trends Shaping Demand

Externally sourced risk factors significantly influence operational outcomes at Danaher. U.S. tariffs on imported components remain a notable concern following the February 2026 Supreme Court ruling limiting prior tariff authorities; the administration's plan to impose new tariffs under alternative legal frameworks could elevate input costs unpredictably over coming quarters [S1]. Such tariff-related cost increases typically necessitate surcharges or price adjustments but entail potential demand elasticity backlash from cost-sensitive customers leading to volume pressures.

Regulatory frameworks around diagnostics have tightened globally with increased scrutiny on reimbursement rates affecting test volumes; China’s volume-based procurement system especially burdens market access there [S14]. Meanwhile technological accelerants such as AI-driven automation of laboratory workflows present both an opportunity for new product innovation—and a source of ongoing capital allocation decisions for the firm.

Geopolitical risks linked to Middle East conflicts or Russia/Ukraine remain minimal in direct exposure (<1% revenue), but broader macroeconomic instability stemming from such conflicts amplifies commodity price volatility impacting manufacturing costs indirectly [S1].

Growth Catalysts and Potential Constraints Ahead

Key growth vectors are rooted structurally rather than cyclically: accelerating global biotherapeutics development data underpins sustained demand for Biotechnology consumables; likewise increasing adoption of gene therapy tools fuels Life Sciences consumable consumption. Emerging market penetration—particularly China’s upward trend—is a focal area where tailored solutions can gain traction amidst expanding healthcare infrastructure budgets [S21].

In contrast, Diagnostics growth remains constrained due primarily to reimbursement pressures reducing disposable volume demand. Innovation efforts seek offsetting alternatives through software-enabled diagnostics solutions accompanying core instrumentation.

Acquisition integration (e.g., Masimo) represents a critical near-term catalyst contingent on successful harmonization of operations without excessive dilution of margins due to transaction expenses observed recently [S9]. Furthermore, continued tariff impacts require agility in pricing strategy balancing input cost recovery against customer retention.

Upcoming Milestones and Indicators to Monitor

Monitoring the evolution of segmental revenue trajectories post-Q1 will be instructive—particularly whether Diagnostics volume declines stabilize or revert amid innovation launches or regulatory easing. Execution updates regarding Masimo acquisition progress are anticipated within management commentary at forthcoming quarterly calls; these provide insight into expected synergy realization timelines [N1].

Margin progression remains an operational barometer reflecting effectiveness of ongoing DBS-driven productivity improvements vis-à-vis inflationary pressures from tariffs or wage inflation.

Currency fluctuations will persist as a double-edged sword impacting reported earnings; hence forex hedging strategies disclosures merit attention alongside capital allocation signals indicative of sustaining innovation investments versus shareholder returns.

Supporting Financial Performance with Liquidity and Capital Structure

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 3.6 | 6.4 | 4.7 | 1156 | -7.3% |

| 2024 | 3.9 | 6.7 | 4.9 | 1392 | -18.2% |

| 2023 | 4.8 | 7.2 | 1.3 | 1383 | -33.9% |

| 2022 | 7.2 | 8.5 | 8.7 | 1152 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 878 | 3.1 | 5.3 |

| 2024 | 768 | 6.0 | 5.3 |

| 2023 | 821 | 5.8 | |

| 2022 | 818 | 7.4 |

Source: SEC companyfacts cache [F1].

Financial disclosures underscore a solid liquidity position with a current ratio near 1.87 as of Q1 2026 end reflecting prudent working capital management [F1]. Operating income edged down slightly (-3.6% YoY FY2025 vs FY2024), reflective partly of investment activities and marginal margin pressures; net income similarly contracted moderately (-7.3%) amid elevated non-operational charges [F1]. However, operating cash flow remained robust at over $6.4 billion FY2025 supporting capital expenditures around $1.15 billion—allocated mainly toward capacity expansions for manufacturing instruments integral to OTL arrangements servicing client labs globally [F1], [S20].

Debt maturity profiles detailed April 2026 show staggered senior notes extending beyond 2040 providing manageable refinancing risks while preserving flexibility for strategic acquisitions like Masimo or share repurchases executed prudently ($3 billion repurchased FY2025 vs $6 billion prior year) balanced against steadily increasing dividends ($878 million paid FY2025) [F1], [S3]. This conservative capital structure posture aligns with sustaining long-term innovation-led growth priorities plus responsiveness amid trade/regulatory environments.

This analysis is intended solely for informational purposes reflecting Danaher Corporation's latest filings as of April 21, 2026 including SEC 10-Q/Q-K disclosures; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments