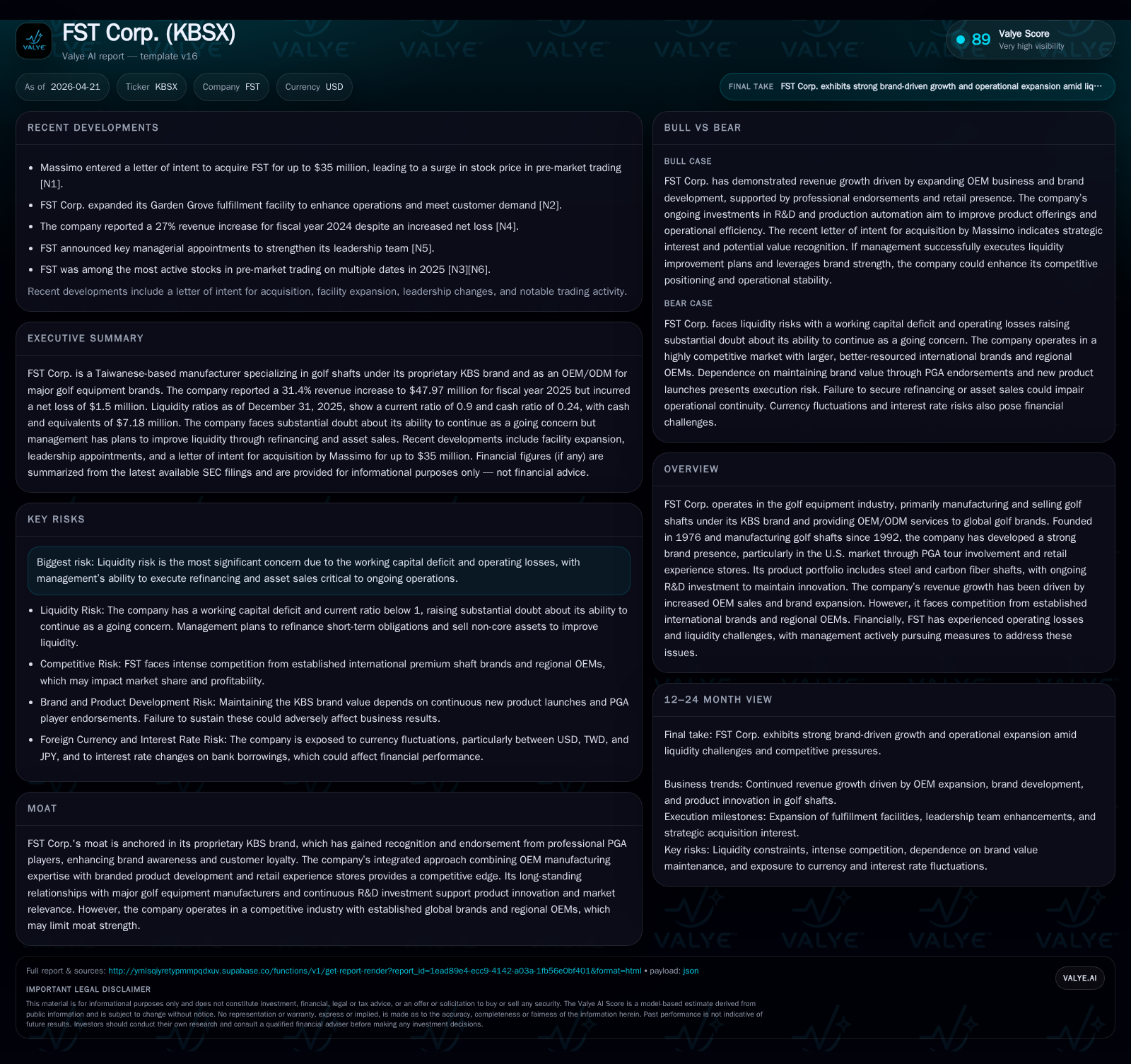

FST Corp. Capitals on KBS Brand to Boost Market Share Despite Persistent Losses

FST Corp. leverages its proprietary KBS brand and OEM expertise to grow revenue, despite sustained operating losses and liquidity concerns.

In its latest quarterly filing, FST Corp. reported a 31% increase in revenue driven by OEM sales and expanded brand presence but continues to generate operating losses with a working capital deficit raising liquidity risks. The company’s business model combines OEM manufacturing with proprietary KBS branded golf shafts endorsed by PGA players, fostering higher-margin opportunities while maintaining production scale. The industry’s competitive landscape poses pricing and innovation pressures, yet FST’s strategic retail stores and R&D driven by pro feedback underpin growth drivers. Ahead, monitoring refinancing success and operational execution will be key amid ongoing capital structure stress.

Latest Quarterly Operating Update Highlights Revenue Gains amid Operating Losses

FST Corp., reporting under its February 2026 6-K filing, revealed unaudited year-end financials for 2025 showcasing robust top-line growth counterbalanced by persistent losses and liquidity pressures [S2][F1]. Revenue advanced sharply by 31.4% to $47.97 million, reflecting higher OEM volumes and increased acceptance of its proprietary KBS brand globally. Despite this, the company recorded an operating loss of $2.33 million—down 36% from the prior year’s $3.64 million—and a net loss nearing $1.5 million, evidencing progress yet continued unprofitability [F1]. Operating cash outflows narrowed but remained negative at around $1 million amidst working capital challenges.

The working capital deficit stood at approximately $2.9 million as of year-end 2025, intensifying concerns over near-term liquidity [S3][F1]. Management has articulated plans to address these constraints through potential refinancing efforts aimed at extending debt maturities alongside contemplated non-core asset disposals to shore up cash reserves [S3][S4]. While improved cash collections signal healthier market demand and inventory normalization among customers, ongoing negative free cash flow sustains going concern doubts flagged explicitly in disclosures.

Evolution of FST Corp.’s Business Model: From OEM to Proprietary KBS Brand Leadership

Founded in Taiwan in 1976 with golf shaft manufacturing commencing in 1992, FST has traditionally operated as an OEM and ODM provider for major international golf equipment companies [S1]. However, since launching its own high-performance "KBS" brand in 2007—championed by designer Kim Braly—the firm has progressively shifted toward cultivating branded products offering higher margin potential [S1].

The strategic pivot centers on leveraging the KBS brand's growing reputation through extensive participation in the PGA Tour beginning in 2008 and direct shaft supply relationships with professional players since 2016 [S1]. This enables FST not only to command better pricing but also capture brand profits that OEM clients typically retain. The company benefits from a vertically integrated model pairing large-scale manufacturing capabilities with direct-to-consumer channels through KBS retail experience stores located in the U.S., Taiwan, and Japan.

This hybrid approach enhances bargaining power vis-à-vis other Taiwanese peers largely restricted to OEM roles and accelerates innovation responsiveness by internalizing customer feedback loops from professionals using its shafts competitively [S1]. The business model thus supports both volume-driven production economies and premium branded offerings differentiated by endorsement fatigue-resistant reputational capital.

Product Quality and Service Innovation: Crafting Golf Shafts Tailored to Pro Feedback

FST's portfolio spans steel shafts—such as the KBS Tour and C-Taper—and advanced carbon fiber lines including Hybrid, TGI graphite, and TD Driver shafts launched over recent years [S1][S19]. This breadth caters to growing consumer preference for one-stop shopping models addressing diverse playing styles across amateur and professional tiers.

Critical to product relevance is FST’s continuous R&D investment designed to compress product life cycles amidst industry pressure for frequent innovation [S1][S19]. Dedicated teams shadow PGA players during tournaments capturing detailed performance insights which inform iterative shaft design refinements. Additionally, innovations such as IoT-enabled production data collection have enhanced manufacturing efficiency minimizing labor costs while advancing quality consistency [S19].

Complementing product line diversification are experiential retail formats outfitted with state-of-the-art simulation tracking and swing analytics systems enabling precise customer fitting services—a compelling value-add even though custom build revenues remain immaterial so far [S1]. These elements collectively fortify FST's competitive product positioning based on superior customization calibrated against elite player data.

Competitive Industry Dynamics: Global Golf Shaft Players, Pricing, and Market Access

The golf shaft market is dominated by well-established global suppliers boasting robust brand equity alongside fragmented regional OEM manufacturers primarily serving local markets [S1]. In this context, FST seeks differentiation via its dual-brand/OEM hybrid model which helps sustain production scale benefits while extracting incremental margin from proprietary offerings.

Pricing power is constrained given close competition especially from entrenched multinational giants like True Temper or Fujikura who command significant distribution leverage across the golf equipment ecosystem . Nevertheless, FST's embeddedness as both an OEM partner producing shafts for major brands (e.g., TaylorMade, Callaway) and a direct-to-player supplier mitigates vulnerability by diversifying revenue sources and customer concentration risk [S21].

Supply chain robustness stems partly from legacy manufacturing proximity in Taiwan aligned with incremental automation investments reducing cycle times—a competitive edge amid industry demands for rapid product launches [S19]. However, cyclical downturns in leisure spending or disruption risks related to forex volatility between USD/TWD/JPY introduce ongoing headwinds requiring vigilant management.

Key Growth Drivers: PGA Tour Endorsements, Retail Experience Stores, and R&D Investment

FST's brand momentum is propelled significantly by endorsement adoption; as of late 2025, 69 professional golfers including PGA Tour players employed KBS shafts competitively—a powerful marketing engine enhancing visibility among serious amateurs seeking proven equipment [S1]. These endorsements deepen credibility beyond pure commercial messaging translating into durable brand loyalty.

Expansion of physical touchpoints through KBS Golf Experience stores in Carlsbad (California), Taipei, and Tokyo supports direct consumer engagement providing customized fitting influenced directly by player inputs leveraging cutting-edge simulation technologies [S1]. While revenues from custom club building remain nominal currently due to focus on shaft sales predominance, these outlets serve strategic functions fostering incremental attachment effects enhancing long-term retention.

From an investment perspective, R&D spend has risen notably (15% increase year-over-year ending 2025) reflecting management commitment to staying ahead technologically through material innovation and production process automation integrating IoT for data-driven efficiency gains [S19][S21]. Continuous iteration fuelled by pro user feedback closing design-to-market loops underpins FST’s claim to innovation leadership within niche shaft categories critical for sustaining relevance where launch cadence increasingly influences shelf space allocations.

Constraining Factors: Liquidity Risks, Working Capital Deficit, and Competitive Pressures

Despite operational improvements driving top-line expansion and gross profit enhancements maintaining margins near ~43%, FST faces acute liquidity pressures manifested in an approximate $2.94 million working capital deficit at the end of 2025 along with consistent negative operating cash flows totaling about $1 million during the year [F1][S3][S4]. These dynamics raise a substantial doubt regarding ongoing viability without successful remediation.

Refinancing efforts constitute a central pillar of management’s contingency planning aiming at rolling short-term debt exposures exceeding $18 million due within one year alongside target asset monetization through non-core land dispositions expected to generate sufficient proceeds for short-term obligations servicing [S3][S4]. Execution success here remains uncertain amidst volatile credit markets posing an existential risk if plans falter.

Compounding capital structure strain are persistent annual net losses ($1.5 million for FY 2025) offset partially by revenue growth but insufficient to restore positive free cash flow given reinvestment requirements highlighted by sustained capex levels albeit sharply down from prior year levels reflecting a temporary scaling back post extensive investments in prior periods [F1][S15]. Furthermore competitive intensity from multinational incumbents limits pricing elasticity while consumer discretionary spend sensitivity constrains demand scalability practically making margin expansion delicate over the medium term.

What Investors Should Track: Refinancing Outcomes, Operational Execution, and Market Expansion

Key near-term milestones revolve around management’s ability to secure favorable refinancing extending debt maturities mitigating liquidity crunch risk highlighted prominently within SEC disclosures [S3][S4]. Parallelly observing operational metrics such as sales order growth velocity across OEM channels combined with progressive traction for newly introduced shaft series shaped directly by pro feedback will offer signals regarding core business execution quality.

Further attention should be paid to expansion and monetization dynamics within KBS Golf Experience stores network—with specific emphasis on their contribution towards enhancing customer lifetime value beyond shaft unit sales—as well as effectiveness of R&D spend converting into commercially viable next-generation products accelerated along increasingly compressed development cycles mandated by evolving market expectations [S6][S21].

Currency fluctuations impacting Taiwanese operations versus dollar-based revenues represent another variable influencing cost structure unpredictability necessitating diligent hedging strategies or contingency provisions [S12]. Overall trajectory towards sustainable profitability hinges critically on these interconnected factors balancing organic expansion against financing discipline within a challenging competitive environment.

Supporting Financials: Revenue Growth, Profitability Trajectory, and Cash Flow Challenges

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 48 | -2 | -1000014 | -2 | +31.4% | +53.6% |

| 2024 | 36 | -3 | -1576129 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | -2 | -9.7 |

| 2024 | 3 | -6 | -14.2 |

Source: SEC companyfacts cache [F1].

Source: Company filings [F1]

FST achieved a compounded annual revenue growth rate exceeding 30% between FY24-25 while concurrently improving operating losses by approximately 36% signaling operational gearing benefits materializing alongside scale-up efforts. However net income remains negative reflecting continuing investment phase impacts including elevated selling expenses linked partly to expanding retail footprint plus functional increases associated with tooling capacity enhancements within U.S. operations [S15]. Operating cash flow trends mirror income statement losses with free cash flow estimated around -$1.6 million after capex absorption underscoring ongoing funding necessity absent immediate profit generation continuity.

These financial contours reinforce a narrative of emerging brand traction coupled with scaling production capabilities tempered fundamentally by pressing liquidity constraints demanding scrupulous financial management acumen moving forward.

Disclaimer: This analysis is for informational purposes only. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments