Credo Technology’s Turnaround: From Operating Losses to Positive Cash Flow in FY2025

In FY2025, Credo Technology reversed multi-year operating losses to generate significant cash flow and profitability, supported by strategic AI hardware partnerships and solid capital structure.

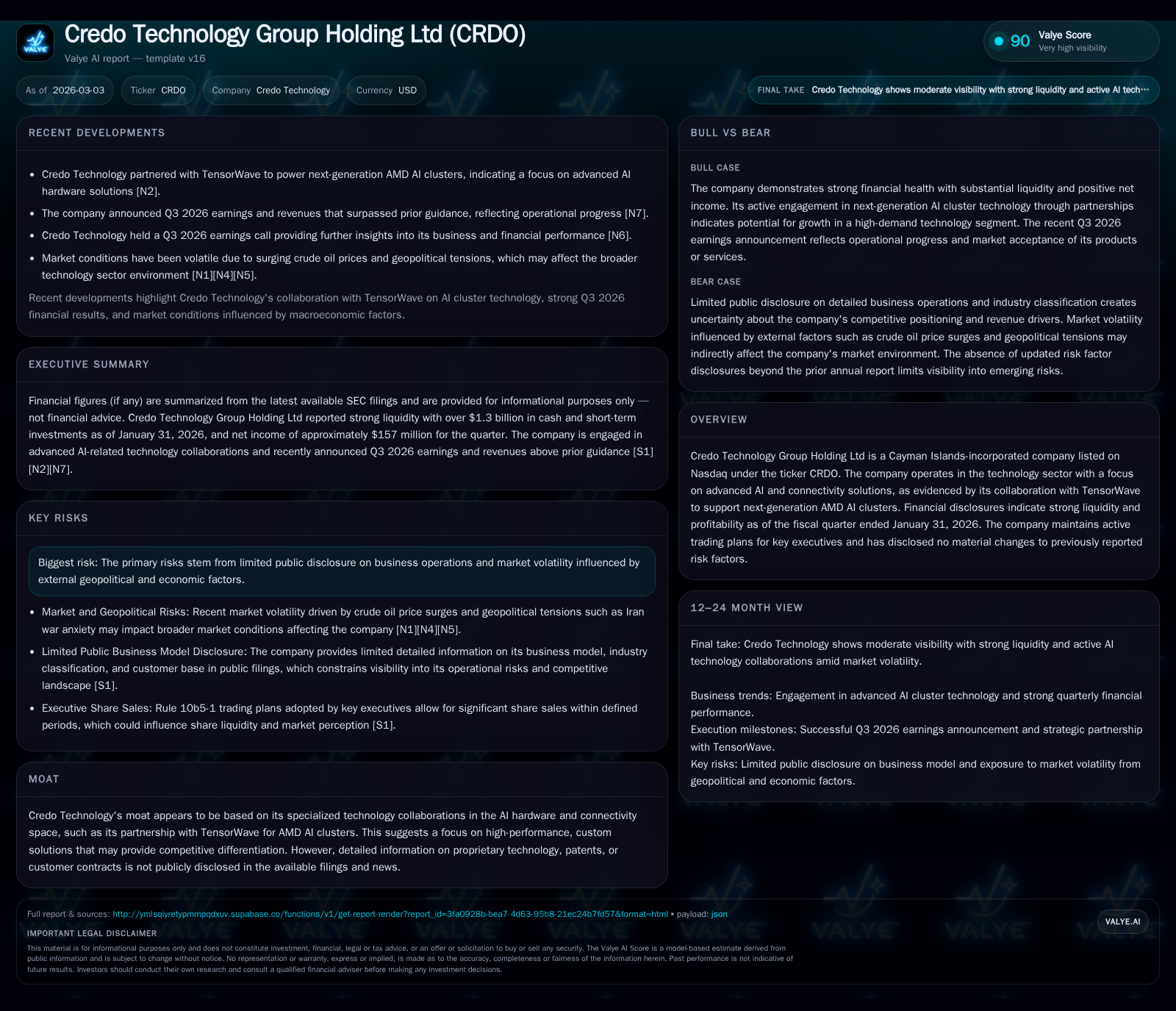

Credo Technology Group Holding Ltd posted a $37.1 million operating income and $52.2 million net income in FY2025, marking a sharp turnaround from prior losses. The company’s partnership with TensorWave to support next-generation AMD AI clusters underpins new revenue opportunities. As of January 31, 2026, Credo held $1.22 billion in cash and equivalents with a current ratio exceeding 10x, positioning it well for continued investment. Capital expenditures rose sharply reflecting growth investments. While growth prospects appear favorable amid AI hardware demand, risks include geopolitical uncertainty and limited public disclosure on technology specifics.

Evolution from Loss to Profit: FY2022–FY2025 Performance Overview

Credo Technology’s financial performance over the past four fiscal years shows a notable turnaround. From operating losses of approximately $22 million in FY2022 worsening to around $37 million in FY2024, the company shifted to operating profitability of $37.1 million in FY2025, representing a 200% year-over-year improvement [F1]. Net income similarly swung from a loss of $28.4 million in FY2024 to a gain of $52.2 million in FY2025, up nearly 284% YoY [F1].

Operating cash flow followed this positive trend, nearly doubling from about $32.7 million to over $65 million year-over-year, underscoring stronger core business cash generation [F1]. Capital expenditures rose sharply by more than 130% to $36.1 million in FY2025, indicating substantial reinvestment into product development or capacity expansion [F1]. Equity also expanded from approximately $540 million to over $681 million during this period.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 52 | 65 | 37 | 36 | +283.9% |

| 2024 | -28 | 33 | -37 | 16 | -71.4% |

| 2023 | -17 | -25 | -21 | 22 | +25.4% |

| 2022 | -22 | -31 | -22 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 29 | 7.7 | |

| 2024 | 17 | -5.3 | |

| 2023 | 0 | -46 | -4.8 |

| 2022 | 0 | -48 | -6.6 |

Source: SEC companyfacts cache [F1].

This rapid improvement aligns with sector dynamics favoring firms specializing in custom AI hardware solutions where operational leverage can improve swiftly once scale is reached.

Strategic Collaborations Powering New Revenue Streams

A key driver supporting Credo’s recent performance is its partnership with TensorWave focused on next-generation AMD AI clusters [N9]. This collaboration places Credo at the forefront of developing specialized connectivity architectures tailored for high-performance AI computing environments.

Addressing power efficiency bottlenecks remains critical in this space as highlighted by industry observers [N10]. Credo's involvement likely centers on advanced interconnect chips or modules that optimize latency and power consumption while maximizing throughput—essential for feeding complex AI models efficiently.

While detailed disclosures on proprietary technology remain limited publicly [S2][S5], this partnership suggests an emerging technical moat based on deep expertise and close OEM engagement rather than commoditized components.

Current Financial Strength: Cash Position and Liquidity

At the quarter ending January 31, 2026, Credo held approximately $1.22 billion in cash and equivalents alongside total current assets near $1.79 billion against current liabilities of approximately $165 million [F1][S4][S7]. This yields a robust current ratio above 10x—a strong indicator of liquidity and short-term financial stability.

The balance sheet shows no significant debt burdens or restrictive covenants disclosed [S4][S7], providing flexibility to fund ongoing R&D and scaling initiatives without near-term refinancing concerns.

Growth Outlook: Opportunities Amid Challenges

Growth prospects are anchored by ongoing integration projects stemming from the TensorWave partnership and broader trends favoring specialized connectivity solutions for AMD-powered AI cluster deployments [N9]. The technical complexity involved may foster sticky customer relationships.

However risks persist including geopolitical uncertainties flagged in recent risk disclosures without material changes [S2][S5], and macroeconomic factors such as supply chain disruptions or market volatility linked to geopolitical events .

Growth visibility is constrained by limited granular guidance; stakeholders should monitor order backlogs and collaboration updates alongside sector data center spending trends for early signals.

Capital Allocation: Investment Focus and Returns

Capital allocation reflects maturation with capex rising over 130%, likely targeting design or manufacturing capability expansion aligned with demand growth [F1]. Operating cash flow near $65 million generated estimated free cash flow around $29 million after capex deductions [F1].

Return metrics show improving efficiency with an approximate ROE of 7.7%, calculated as net income divided by equity at fiscal year end FY2025—a reasonable baseline as business economics improve beyond break-even stages [F1].

The company has not conducted share repurchases nor declared dividends since at least FY2022 indicating a focus on reinvestment rather than shareholder distributions currently [F1][S14][S19][S20].

Insider Trading Plans and Market Sentiment

Insider Rule 10b5-1 trading plans were adopted by COO Yat Tung Lam and CFO Daniel Fleming covering periods extending into fiscal year 2027 [S2][S5]. These planned sales typically represent orderly liquidity management or diversification rather than negative sentiment.

Market reaction included oversold technical conditions following Q3 earnings beats but underlying fundamentals remain constructive given reported milestones [N14][N3].

Risks and Transparency Considerations

Despite positive trends notable risks include limited public transparency regarding proprietary technologies or binding customer agreements complicating moat assessment beyond known partnerships [S2][S5].

Geopolitical tensions coupled with commodity price volatility pose external headwinds potentially disrupting operations or investor confidence as reflected in recent market reactions tied to crude oil surges and regional conflicts .

Mitigating these risks will require enhanced disclosure alongside managing competitive pressures prevalent within advanced semiconductor components serving hyperscale AI architectures.

Disclaimer: This report is based exclusively on publicly available documents dated through March 3rd , 2026 . It aims to provide detailed factual analysis without offering investment advice or forecast guarantees.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments